Best life insurance in British Columbia

Get an instant quote in minutes, compare top insurers, and choose coverage that fits your family and budget.

How life insurance works in British Columbia

Life insurance in British Columbia (BC) is an agreement between you and an insurance provider that guarantees a tax-free lump sum payment to your beneficiaries if you pass away while the policy is active. The payout is designed to protect your family from financial strain by covering expenses such as mortgage payments, outstanding debts, daily living costs, or future education needs.

Most BC residents choose between term life insurance, which provides coverage for a fixed period (such as 10, 20, or 30 years), and whole life insurance, which offers lifelong protection. Your premium is determined by factors such as age, health, smoking status, coverage amount, and policy type.

Once approved, you pay a monthly or annual premium to keep the policy active. If a claim is made, the insurer pays the agreed benefit directly to your named beneficiaries. At PolicyAdvisor, we help you compare policies from multiple insurers in BC so you can choose coverage that aligns with your financial goals and budget.

Types of life insurance in British Columbia

Term life insurance

Coverage for a fixed period (10, 20, or 30 years). Often used for mortgages, income replacement, and family expenses.

- Lower monthly premiums

- Strong short- to mid-term protection

- Common for young families

Whole life insurance

Lifelong coverage with cash value. Often used for estate planning and long-term wealth transfer.

- Permanent protection

- Cash value component

- Predictable long-term structure

How much life insurance cost in British Columbia

Life insurance premiums in BC are priced based on individual risk, but term coverage remains comparatively affordable for most healthy applicants.

Below are estimated monthly premiums for healthy non-smokers in British Columbia:

| Age | Male | Female |

|---|---|---|

| 25 | $31 | $22 |

| 35 | $33 | $26 |

| 45 | $75 | $54 |

| 55 | $223 | $155 |

| 65 | $716 | $487 |

Term life insurance premiums, $500,000 death benefit, non-smoking, 20-year term

What determines your premium in British Columbia?

Life insurance premiums in British Columbia are calculated through a process called underwriting. Insurers assess your overall risk profile to determine how likely you are to make a claim during the policy term.

Since insurers in BC use different underwriting models, the same applicant can receive different quotes across providers. PolicyAdvisor allows you to instantly compare rates from the biggest Canadian insurers, helping you identify competitive pricing based on your unique profile.

Need insurance answers now?

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them.

Why choose PolicyAdvisor for life insurance in British Columbia?

Buying life insurance in British Columbia doesn’t mean choosing the first insurer you find. Comparing multiple providers helps ensure you secure competitive quotes and the right policy structure for your needs. With PolicyAdvisor, you can:

No waiting for callbacks. No hidden pricing. Compare personalized insurance quotes upfront.

View multiple options side-by-side and find the best, most affordable option for your financial safety.

Your premiums stay fair and clear.

Explore your options without any pressure to buy.

Start your quote online in minutes and complete your application seamlessly.

Have questions? Speak to a licensed advisor for guidance anytime you need it.

How much life insurance coverage do you need in British Columbia?

The right coverage amount depends on your financial obligations and long-term responsibilities. A common rule is to get coverage equal to 7 to 10 times your annual income, but individual needs vary. When calculating your coverage needs, consider:

Because every household situation is different, using a life insurance calculator can help estimate a more precise coverage amount.

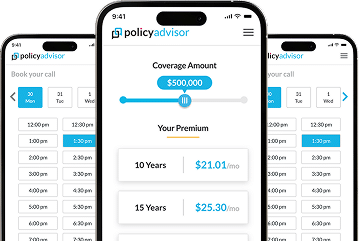

Get a personalized quote in seconds

Get instant quotes from Canada's top life insurance providers and find the perfect coverage for your family.

Powered by

![]()

Life insurance in major British Columbia cities

Life insurance needs can vary across British Columbia’s major cities due to differences in housing markets, average mortgage balances, and household income levels. In cities where property prices and living costs are higher, residents often structure coverage to protect larger mortgage obligations and ensure long-term income replacement for their families.

Get life insurance quotes in different cities

- Vancouver

- Surrey

- Burnaby

- Richmond

- Abbotsford

- Coquitlam

How to apply for life insurance in British Columbia

Applying for life insurance in British Columbia usually starts with choosing your coverage amount and policy type, followed by a health questionnaire or medical exam. Once underwriting is complete, the insurer reviews your application and determines your final premium.

Comparing multiple insurers before applying helps ensure you receive the best possible pricing and policy structure based on your profile. With PolicyAdvisor, the process is streamlined:

-

Save time

Get instant quotes from BC’s top life insurance companies

-

Save money

Compare multiple quotes to find the best price

-

Shop anywhere

Use online tools from your phone or computer

-

Personalized service

Receive expert advice from a dedicated insurance advisor

Common mistakes to avoid when buying life insurance in British Columbia

-

Relying only on employer-provided coverage

Group insurance is often limited to one or two times your annual salary. This may not be enough to cover mortgage debt, long-term income replacement, or future education costs.

-

Underestimating how much coverage you need

Choosing a lower coverage amount to save on premiums can leave your family financially exposed.

-

Waiting too long to apply

Premiums increase with age, and health changes over time. Delaying coverage can result in higher costs or limited eligibility.

-

Not comparing multiple insurers

Life insurance quotes and underwriting standards vary between companies. Applying with only one insurer may mean paying more than necessary.

-

Choosing mortgage insurance instead of individual coverage

Mortgage insurance typically names the lender as beneficiary and coverage decreases over time. Individual life insurance provides more flexibility and control.

Frequently Asked Questions

Is life insurance mandatory in British Columbia?

No, life insurance is not legally required in British Columbia. However, it is strongly recommended if you have dependents, a mortgage, or outstanding debts. It ensures your family is financially protected and not burdened with repayments or daily expenses in your absence.

Can I get life insurance in British Columbia without a medical exam?

Yes, many insurers offer no-medical or simplified issue life insurance in British Columbia. These plans are ideal if you want faster approval or prefer to avoid medical tests. While premiums may be slightly higher, they provide a convenient option for many applicants.

Are life insurance premiums higher in British Columbia?

Life insurance premiums are not directly based on your province but on personal factors such as age, health, smoking status, and coverage amount. However, people in British Columbia may choose higher coverage due to larger mortgages or higher living costs.

What types of life insurance are popular in British Columbia?

Term life insurance and whole life insurance are the most common choices in British Columbia. Term plans are popular for covering temporary needs like mortgages and income replacement, while whole life insurance is used for long-term financial planning and estate transfer.

Can I get life insurance if I have a mortgage in British Columbia?

Yes, life insurance is often used to protect mortgage obligations in British Columbia. Instead of relying solely on mortgage insurance from a lender, many homeowners prefer individual life insurance policies because they offer fixed coverage, flexible beneficiaries, and better long-term value.