1-888-601-9980

1-888-601-9980Mortgage Insurance Vs Life Insurance

Mortgage insurance pays off a mortgage debt in the event the borrower passes away while the principal loan is still outstanding. However, a better alternative is mortgage protection through a term life insurance policy; it can offer more flexible protection than mortgage insurance and cost considerably less.

Have you recently purchased a home or refinanced your mortgage? If so, you have probably opened your mailbox or email inbox to find several offers for mortgage insurance. Many people confuse mortgage insurance with other products, like mortgage default insurance. Before you make a choice, look at mortgage insurance vs life insurance for your protection needs.

There are a lot of good reasons to purchase life insurance in the first place, as anyone with young children or other dependents knows. Life insurance protects your family and loved ones if anything unexpected happens to you. But it’s not the first thing on new homeowners’ minds when thinking about protecting their new purchase.

What is mortgage default insurance?

Mortgage default insurance is a mandatory insurance policy required when the down payment for your newly purchased home is above 5% but less than 20% of the value of your home. This insurance is offered to protect the lender or financial institution, in case you as the borrower are unable to make the mortgage payments for any reason. In Canada, mortgage default insurance is currently offered by two entities: Genworth and Canada Mortgage and Housing Corporation (CMHC).

On the other hand, mortgage insurance is a product that you elect to purchase for a very specific reason. What is that you ask?

Need insurance answers now?

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

What is mortgage insurance?

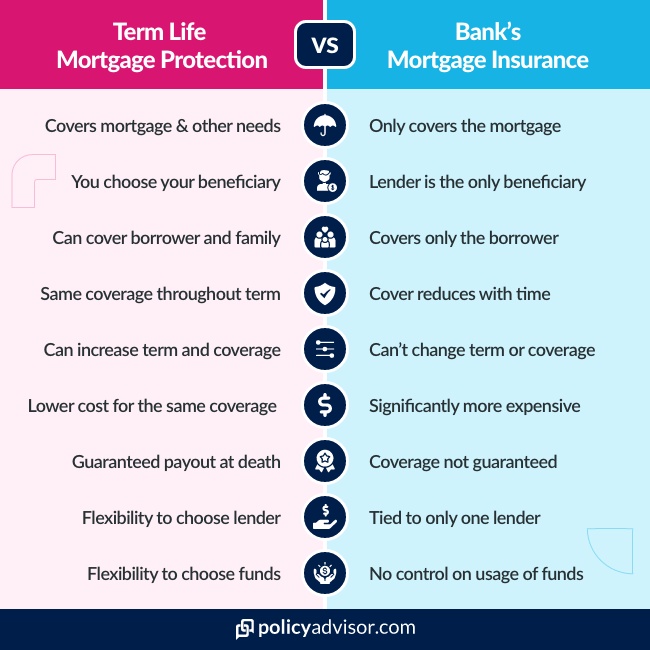

Mortgage insurance is an insurance policy, generally offered by your lender, that pays off the mortgage should the borrower die, while the principal on the loan is still outstanding. A mortgage insurance policy (sometimes referred to as a mortgage life insurance policy) requires a fixed cost premium payment by the borrower to cover a reducing mortgage debt for the benefit of your lender until the mortgage balance is paid. With mortgage insurance, the lender is covered. However, it doesn’t fully protect you or your needs. Our experience as insurance professionals shows there are other products that do a much better job of protecting your mortgage.

Read our full review of the Best Mortgage Insurance Companies in Canada.

Are there alternatives to mortgage insurance?

YES! As mentioned, mortgage life insurance entails a fixed cost payment that covers a diminishing mortgage debt for your financial institution until the mortgage is paid. The alternative to mortgage life insurance is mortgage protection through term life insurance. It can better protect your investment and the life you’re building for your loved ones.

What is mortgage protection insurance?

Mortgage protection insurance is an insurance policy offered by insurance companies that protects the borrower through a term life insurance product. It offers a lot more flexibility than traditional mortgage insurance. Term life insurance can be tailored in a way to make certain that families can pay off the mortgage balance and also provide coverage for many other needs, in case an income earner passes away. Typically, you can choose between a range of terms such as 10-, 15-, 20-, or 30-year term to closely match the length of time you have left to pay off the mortgage.

How much mortgage protection do I need?

You would generally buy at least enough mortgage protection coverage to pay the balance of your mortgage, which may be at least $160,000 (StatsCan) Mortgage protection through life insurance can make sure that a surviving spouse and children will be able to keep the family home, even if the homeowner dies unexpectedly.

Through term life insurance you have the option to consider a policy with a death benefit larger than your mortgage to cover other such obligations as your child’s education, other debts, and living expenses for survivors. Our insurance calculator can help you determine the amount of life insurance you need.

Choosing Mortgage Insurance Vs Life Insurance

Sure – there are some small advantages to mortgage insurance; we would be remiss if we didn’t mention them. As it is offered by your lender, you pay for it when you make your monthly mortgage payments – no need to worry about missing it. That said, is this small convenience worth thousands of dollars? Because that’s what you’ll be overpaying for the same amount of coverage over the life of your mortgage.

Another supposed advantage of your bank-offered mortgage life insurance – there is no underwriting when you purchase. You qualify instantly without a medical exam. The caveat here is that the mortgage insurance is not a guaranteed coverage and is only underwritten at the time of filing of a claim, so your estate might find out after your death that you weren’t covered as well as you thought or maybe not covered at all. Besides the unfortunate circumstances around an early death, having to deal with the duress of further investigation into that death is stress your loved ones do not need at that time.

Read our full review of the Best Life Insurance Companies in Canada.

6 Reasons Why Term Life Insurance is Better for Mortgage Protection

Want to learn even more about mortgage insurance vs life insurance? Read our Honest Guide To Mortgage Insurance or schedule a call with one of our licensed brokers to discuss your specific protection needs. Even better: get a free instant quote for mortgage protection with our online tool – you only have to answer a few basic questions to get a clear picture of how much it may cost to protect your mortgage.

- Mortgage insurance pays off one’s mortgage in the event the borrower dies, but other products can do a better job at protecting a mortgage debt.

- A term life insurance policy can offer you better mortgage protection in a number of ways

- The policyholder chooses the beneficiary, and in turn the beneficiary can choose exactly how the benefit is used (paying off the mortgage, servicing other debts, handling final expenses, etc)