If someone depends on your income, term life insurance is one of the most affordable solutions to protect their financial future. It offers coverage for a specific period (such as 10, 20, or 30 years), and if you pass away during the policy term, your beneficiaries receive a tax-free, lump-sum payment known as a death benefit.

Unlike permanent life insurance, term life insurance does not build cash value or include an investment component. Instead, it focuses on providing high-value financial protection at significantly lower premiums, making it one of the most popular types of life insurance for Canadian families.

Need insurance answers now?

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

What is term life insurance in Canada?

Term life insurance is a type of life insurance that provides financial protection for a set number of years. If the insured dies during that coverage period, the insurer pays a tax-free lump sum to their chosen beneficiaries. Since term life insurance does not have a savings or investment component, it typically costs much less than permanent life insurance. This is great for applicants seeking higher coverage amounts for lower premiums.

For example, a healthy 35-year-old parent may be able to purchase $500,000 in coverage for somewhere between $25 and $40 per month. The same amount of coverage for whole life insurance could cost around $250 to $400 per month. This makes whole life roughly ten times more expensive than a term life policy.

Term life insurance in Canada: At a glance

| Feature | Details |

| How it works | Pay premiums for a fixed term. If you die during the term, your beneficiaries receive a tax-free payout |

| Coverage period | Typically 10, 15, 20, 25, or 30 years |

| Who is it best for | Families, homeowners, parents, young professionals, and business owners |

| Cost | Can cost up to 90% less than permanent life insurance since coverage lasts for a fixed period. |

| Cash value | None. Term life insurance is designed solely to provide financial protection |

| Death benefit | Tax-free payout to your beneficiaries |

| Renewal | Most policies are renewable, but premiums typically increase |

| Can I convert it? | Most policies can be converted to permanent life insurance without a medical exam before a specified age or conversion deadline |

| Common coverage amounts | Typically $100,000 to $5 million or more |

Types of term life insurance in Canada

Although term life insurance provides temporary coverage, insurers offer it in several structures to suit different needs. The most common options are Term 10, Term 20, and Term 30 policies, while some insurers also provide level term, annual renewable term (ART), and return of premium (ROP) term policies.

Here’s a quick overview of the different types of term life insurance in Canada:

| Type of term life insurance | How it works | Best for |

| Level term life insurance | Premiums and death benefit remain the same throughout the policy term | Most Canadians seeking predictable costs |

| Annual renewable term (ART) | Coverage renews every year, with premiums increasing annually based on your age | Short-term coverage needs or temporary financial obligations |

| Return of premium (ROP) term | Returns some or all eligible premiums if you outlive the policy term, depending on the insurer and policy | People who want the possibility of getting premiums back |

| Term 10 (T10) | Provides level coverage for 10 years | Short-term financial obligations, such as personal loans or smaller mortgages |

| Term 20 (T20) | Provides level coverage for 20 years | Families, homeowners, and parents |

| Term 30 (T30) | Provides level coverage for 30 years | Long-term financial protections, such as raising children or paying off a long-term mortgage |

Pros and cons of term life insurance

How does term life insurance work in Canada?

Term life insurance has one of the most straightforward processes among insurance policies. You choose how much coverage you need and how long you want it to last. In exchange for regular premium payments, your insurer agrees to pay your beneficiaries a tax-free death benefit if you pass away during the policy term.

Here’s how a term life insurance policy usually works:

Step 1: Choosing the right coverage amount

Choose a coverage amount that would secure the financial future of your family and protect your loved ones from outstanding debts or other costs. As a general rule of thumb, many applicants choose coverage anywhere between 7 and 15 times their annual income.

Step 2: Choose your policy term

Once you have selected the coverage amount, you need to choose how long your coverage should remain in place. Most Canadian insurers offer the following periods:

| Policy type | Coverage period |

| Term 10 | 10 years |

| Term 20 | 20 years |

| Term 25 | 25 years |

| Term 30 | 30 years |

Step 3: Complete your application and pay your premiums

Once you have chosen your coverage amount and period, you will need to complete your application and name the beneficiary. Most applicants choose their close relatives, such as their spouse, children, or parents, as the beneficiary.

Once the application is completed, you will need to pay your premiums. You can make premium payments monthly or annually. Some insurers offer lower overall costs if you choose to pay annually instead of monthly.

Step 4: Your beneficiaries receive the death benefit

If you pass away while your policy is active, your beneficiaries submit a claim to the insurance company. Once the claim is approved, the insurer pays the death benefit as a tax-free lump sum.

Unlike investment or estate assets, term life insurance proceeds are typically paid directly to named beneficiaries, helping them access funds more quickly during a difficult time.

How to choose the right term life insurance coverage amount?

Choosing the right amount of term life insurance is one of the most important decisions you will make when buying a policy. The coverage amount should be enough to help your loved ones maintain financial stability by replacing the lost income and support you provide if you were to pass away unexpectedly.

When deciding the coverage amount, you should keep in mind factors such as:

- Outstanding mortgage balance

- Personal loans or other debts

- Daily living expenses

- Future childcare costs and education expenses

- Funeral and final expenses

- Income replacement for several years

For many families, a common rule of thumb suggests choosing coverage between 7 and 15 times their annual income. This offers a sizable amount that can cover most future expenses with ease.

Using the DIME method to calculate term life insurance

Another method of calculating how much coverage you need is to use the debt, income, mortgage, and education (DIME) method. It is a simple way to estimate how much term life insurance you may need by considering four major financial obligations your family may need to cover if you pass away.

Let’s assume Sarah is 35 years old, married, has one young child, and is the primary income earner for her family.

Here’s an estimate of her term life insurance needs using the DIME method:

| DIME factor | Amount |

| Debt (credit card balance and car loan) | $25,000 |

| Income replacement (10 years of annual income at $100,000) | $1,000,000 |

| Mortgage (remaining mortgage balance) | $500,000 |

| Education (future education costs for one child) | $150,000 |

| Total estimated life insurance needed | $1,675,000 |

Based on the DIME method, Sarah may consider approximately $1.7 million to 2 million in term life insurance coverage. This amount could help her family pay off outstanding debts and offer financial security for the foreseeable future. While it is a handy index, your ideal coverage amount may differ based on factors such as savings, investments, and long-term financial goals.

Do you need a medical exam for term life insurance?

Not always. Many Canadians can qualify for term life insurance without a medical exam. However, this depends on your age, health, lifestyle, and the amount of coverage you apply for. Many insurers now offer accelerated underwriting and simplified issue options, which allow eligible applicants to qualify without a medical exam. Some insurers also offer no-medical life insurance, although these policies may have lower coverage limits and higher premiums.

However, you may still need a medical exam if:

- You are applying for a high coverage amount

- You are older or have certain pre-existing medical conditions

- The insurer requires additional health information based on your application

Most term life insurance policies in Canada may require you to submit a health questionnaire and furnish information about your height, weight, blood pressure, and medical history. If you are a smoker, you may be subject to additional blood, urine, or cotinine tests. Some applicants may also be required to undergo an electrocardiogram (ECG).

How much does term life insurance cost in Canada?

The cost of a term life insurance policy ranges between $21.60 and $741.60 per month. Your premiums depend on the coverage amount and personal factors, such as gender, age, smoking status, and health.

Here is a sample term life insurance rate for $500,000 coverage:

| Age | 10-Year Term | 20-Year Term | 30-Year Term | Term 100 |

| 25 | $21.60 | $27.90 | $36.90 | $196.58 |

| 35 | $22.04 | $30.15 | $53.55 | $292.50 |

| 45 | $39.15 | $66.60 | $134.10 | $470.25 |

| 55 | $96.75 | $198.90 | $357.30 | $741.60 |

| 65 | $324.45 | $610.65 | na | na |

*Monthly premiums for non-smoking male

Some insurers also offer lower overall premiums if you choose to pay annually instead of monthly. Speak with your advisor to compare the payment options and determine which offers the best value for your policy.

How are term life insurance premiums calculated?

Life insurance companies calculate your premium by assessing the likelihood of paying a claim during the policy term. This is primarily based on your age, health status, smoking status, coverage amount, and other related features.

Here’s a brief overview of the factors that may affect term life insurance premiums in Canada:

| Factor | How it affects your premium |

| Age | Younger applicants typically pay lower premiums |

| Health | Good overall health can help you qualify for lower rates |

| Smoking status | Smokers and tobacco users generally pay significantly more |

| Coverage amount | Higher coverage amounts result in higher premiums. |

| Policy term | Longer terms, such as 30 years, usually cost more than shorter terms like 10 or 20 years |

| Gender | Women often pay slightly lower premiums than men because they generally have longer life expectancies |

| Family medical history | A family history of serious illnesses may affect your premium, depending on the insurer |

| Occupation | High-risk jobs, such as mining or commercial aviation, can lead to higher premiums |

| Hobbies and lifestyle | Activities like skydiving, scuba diving, or motor racing may increase your rates |

| Policy riders | Optional add-ons, such as critical illness or child riders, increase the cost of your policy |

| Payment frequency | Paying annually instead of monthly may qualify you for savings with some insurers. |

When should you purchase term life insurance?

The best time to purchase term life insurance is while you are still young and healthy, before taking on major financial responsibilities. Buying a policy earlier can help you lock in lower premiums, as life insurance generally becomes more expensive with age and as health changes.

In terms of financial responsibilities, you can consider purchasing term life insurance before major milestones such as starting a family, buying a house, or taking on significant debts or loans. The death benefit can help protect your beneficiaries from financial hardships should you pass away unexpectedly.

Learn which is the best time to buy life insurance in Canada

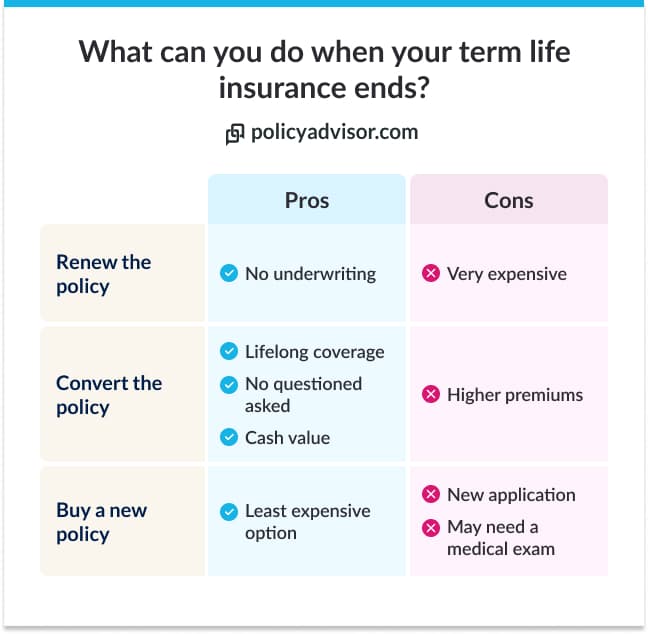

What happens when your term life insurance expires?

Once your policy expires, it does not pay out automatically. Instead, you have several options, depending on your insurer and personal circumstances.

Here is an overview of the choices you can make once your term life insurance policy expires:

| Option | What it means | Typical age limit |

| Renew your policy | Continue your coverage, but at a higher premium | Up to age 75–85, depending on the insurer and policy |

| Convert to permanent life insurance | Switch to a permanent policy without additional medical underwriting if you are eligible | Usually available until age 65–71 or before the policy’s conversion deadline |

| Buy a new policy | Apply for a brand-new term policy based on your current age and health | Most insurers accept new applications up to age 75–80, depending on policy and term |

| Let the policy expire | Coverage ends, and no further premiums are required | No age limit. Coverage ends after the term is over |

If you renew your policy, you will have to pay an increased premium based on your age and other factors at the time of renewal. Renewing can be a good option if you still have financial responsibilities and wish to remain covered for an extended period.

On the other hand, many applicants also convert their term life insurance into a permanent life insurance policy before a specified age or deadline. It is great for those who want lifelong coverage or are interested in estate planning.

However, you can choose to purchase a new policy with different coverage amounts or policy terms to align with your changing needs or financial planning. Alternatively, you can also choose to let the policy expire if your financial needs are met or you have enough savings to offset future costs.

Can you cancel your term life insurance policy?

Yes, most term life policies can be cancelled at any time. If you no longer need coverage, you can cancel your policy by notifying your insurer or advisor. Once cancelled, your coverage ends, and your beneficiaries will no longer be eligible to receive a death benefit. In most cases, you will not receive a refund on the premiums you have already paid.

Additionally, most Canadian insurers are required to provide a free look or cooling-off period after you receive your policy contract. During this time, you can review the policy terms and cancel the policy for a full refund of any premiums you have paid (provided you have not raised any claims during this time). While the industry standard is ten days, some insurers may offer up to 30 days.

Are there any exclusions to term life insurance?

While term life insurance generally covers natural and accidental death, there are certain exclusions where a claim may be reduced or denied. These exclusions vary by insurer and policy, so it’s important to review your policy contract carefully.

Here’s an overview of common exclusions to term life insurance:

| Exclusion | What you need to know |

| Death by suicide | Most policies have a two-year suicide exclusion as part of the contestability period. If death occurs during this time, the death benefit is usually not paid, though premiums may be refunded. |

| Death due to risky activities | Deaths resulting from high-risk activities (such as skydiving, racing, or private aviation) may be excluded unless you have additional coverage or a rider |

| Homicide involving the beneficiary | If the beneficiary is involved in the policyholder’s death, they cannot receive the payout under Canada’s “Slayer Rule” |

| Drug- and alcohol-related deaths | Claims may be denied if drug or alcohol use directly contributed to the insured’s death, based on the insurer’s investigation and exclusion policy |

| Criminal acts and illegal activities | Deaths that occur while committing a crime or engaging in illegal activities are generally not covered |

| Fraud or misrepresentation | Providing false or incomplete information on your application can result in policy cancellation or claim denial |

| War and terrorism | Some policies exclude deaths caused by war, armed conflict, or terrorism |

| Death in high-risk countries | Coverage may be limited or excluded if death occurs in countries affected by war, civil unrest, or political instability |

| Undisclosed pre-existing medical conditions | Failing to disclose a medical condition can void your policy or lead to a denied claim, even if the condition contributed to your death |

| Self-inflicted injuries | Deliberate self-harm, dangerous stunts, or certain situations may not be covered |

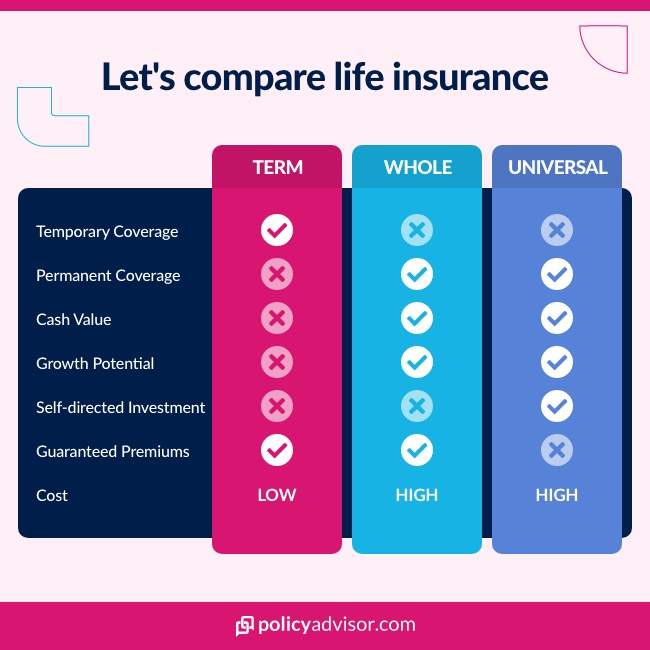

How does term life compare to other life insurance policies available in Canada?

Aside from term, you can get permanent life insurance. Unlike a fixed term for 10 or 20 years, these policies cover you for the rest of your life and may have an investment component.

Some of the most common types of permanent life insurance are:

- Whole

- Universal

- Term-to-100

Here’s a quick overview of how term life insurance compares to other popular options:

| Feature | Term life insurance | Term to 100 insurance | Whole life insurance | Universal life insurance |

| Coverage duration | Fixed term (e.g., 10, 20, or 30 years) | Lifetime (coverage to age 100) | Lifetime | Lifetime |

| Premiums | Lowest and fixed during the term | Fixed until age 100 (or for life, depending on the policy) | Higher but generally fixed for life | Flexible within policy limits |

| Cash value | No | No | Yes (guaranteed growth) | Yes (investment-linked) |

| Medical exam required | Often required, but non-medical options are available | Usually required | Usually required | Usually required |

| Investment component | None | None | Guaranteed cash value accumulation | Flexible investment options |

| Death benefit | Guaranteed if premiums are paid during the term | Guaranteed for life if premiums are maintained | Guaranteed for life | Can be adjusted within policy rules |

| Policy flexibility | Limited (renew or convert before expiry) | Low | High (cash value options with fixed coverage) | High (flexible premiums, investments, and death benefit) |

| Best for | Income replacement, mortgage protection, raising a family, and temporary financial obligations | Lifelong coverage without paying for cash value or investment features | Estate planning, lifelong financial protection, and leaving an inheritance | High-income earners seeking lifelong coverage with investment flexibility |

| Typical cost | Lowest | Lower than whole life but higher than term life | Highest | Higher than term; varies based on investment choices |

For a detailed comparison of the plans, check out the different types of life insurance in Canada

Is term life insurance worth it in Canada?

Yes, term life insurance is worth it for most Canadians who are seeking affordable financial protection for a specific period. The policy offers high coverage at relatively low premiums, making it a good choice for individuals with debts, mortgages, and high financial liabilities.

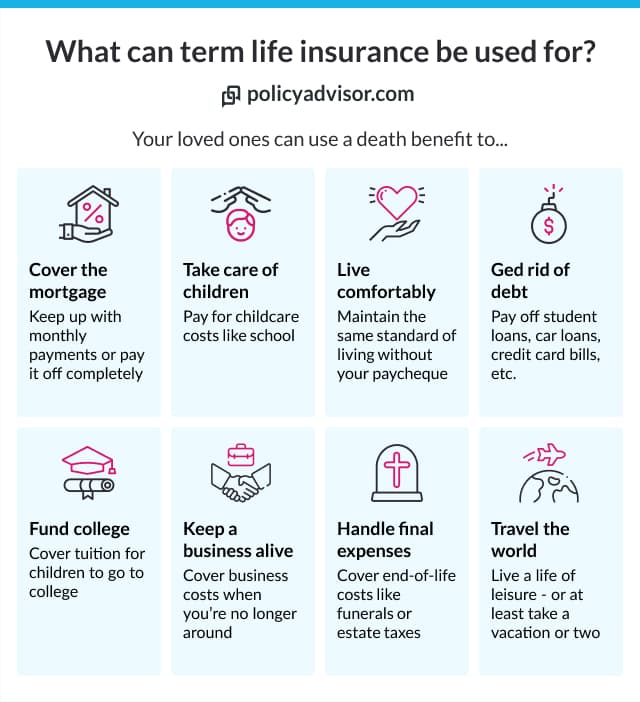

A term life insurance policy helps your loved ones replace lost income and pay off major outstanding debt, ensuring the burden does not rest upon them. It is one of the most cost-effective options for safeguarding your family from financial responsibilities should you pass away.

However, if you need lifelong coverage or are seeking to build cash value and estate planning, a permanent life insurance policy may be more suitable. While the premiums are significantly higher than term life, it provides more financial protection and rewards you with cash value and lifelong protection.

If your goal is to protect your family’s finances and cover immediate debts without paying the higher cost of permanent life insurance, term life insurance offers excellent value and coverage.

Our advisor’s take on term life insurance

At PolicyAdvisor, we recently helped a 35-year-old parent secure affordable term life insurance to protect their family’s financial future. They were seeking enough coverage to replace their income, pay off their newly acquired mortgage, and support their children’s future while keeping monthly premiums affordable.

Client profile

- Age: 35

- Family: Married with two young children

- Primary concern: Income replacement and mortgage protection

- Coverage goal: $1 million in affordable life insurance

Why we recommended term life insurance

- Affordable premiums for a high coverage amount during their peak earning years

- Coverage aligned with their mortgage term to help pay off outstanding debt

- Flexibility to extend the term if financial protection is still required

- The option to convert to permanent life insurance when financial needs change

How to purchase term life insurance in Canada?

PolicyAdvisor’s licensed life insurance advisors can help you compare term life insurance quotes from Canada’s leading insurers based on your age, budget, health, coverage needs, and financial goals.

Whether you are looking to protect your family, cover your mortgage, or secure affordable coverage for a specific period, our advisors at PolicyAdvisor can help you choose the right term length, coverage amount, and optional riders to fit your needs.

Connect with an advisor

Looking for the best term life insurance quotes in Canada? PolicyAdvisor makes it easy to compare quotes from Canada’s leading life insurance companies.

Our advice is 100% free, with no obligation to buy. Whether you are comparing insurers, choosing a policy term, or deciding how much coverage you need, we are here to guide you every step of the way.

Frequently asked questions

Is the term life insurance death benefit taxable in Canada?

No. Life insurance death benefit is generally tax-free in Canada. The amount is paid tax-free to the named beneficiaries if the policyholder passes away during the term.

Can I have more than one term life insurance policy?

Yes, many Canadians own multiple life insurance policies to cover different financial needs or life stages. Additionally, you can combine term and permanent policies to satisfy different financial goals.

Can I convert my term life insurance into permanent life insurance?

Yes, many Canadian insurers allow you to convert your policy before a specified age or conversion deadline without additional medical underwriting. Check your policy or consult with your advisor for eligibility requirements.

What happens if I miss a premium payment?

Most insurers provide a grace period (usually 30 or 31 days) during which you can make the missed payment and keep your coverage active. If the premium remains unpaid beyond this grace period, your policy may lapse.

Can I renew my term life insurance policy after it expires?

Yes, in many cases. Many term life insurance policies in Canada are renewable within a specified period or until a specified age. If you choose to renew, your premiums will typically increase based on your age at the time of renewal.

Does term life insurance cover accidental death?

Yes, most term life insurance policies cover accidental death, alongside death due to illness or natural causes, provided the policy is in force and no exclusions apply.