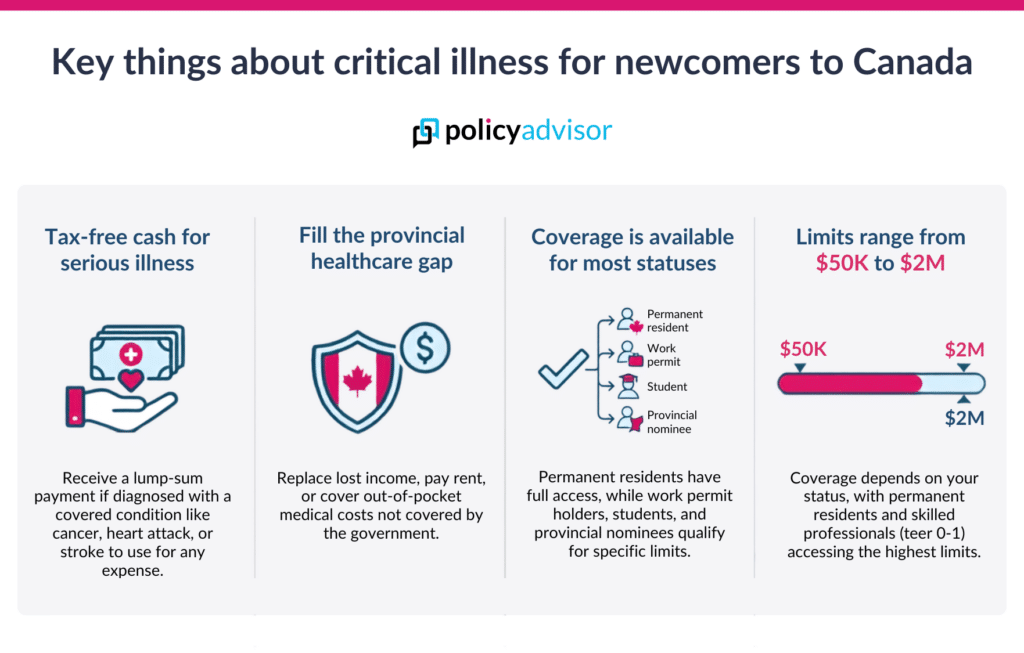

Critical illness insurance for newcomers to Canada provides a tax-free lump-sum payment if you are diagnosed with a covered serious illness such as cancer, heart attack, or stroke. Permanent residents, work permit holders, foreign-trained physicians, and other eligible newcomers may qualify for coverage. This benefit can help replace lost income, cover recovery expenses, and protect your financial stability while you are recovering.

Can newcomers get critical illness insurance in Canada?

Yes, newcomers can get critical illness insurance in Canada, but eligibility, coverage amounts, and policy options depend on their immigration status. Newcomers generally fall into two categories: permanent residents and temporary residents. Permanent residents have the widest access to coverage, while temporary residents may face certain limits and documentation requirements.

Who qualifies for critical illness coverage:

- Permanent residents

- Work permit holders

- Post-graduate work permit holders (PGWP)

- Caregivers/nannies

- International students (only a select few insurers offer)

- Provincial nominees

- Convention refugee / protected person

- Spouse or dependent of an eligible resident

- Foreign-trained physicians

Why do newcomers need critical illness insurance?

Critical illness insurance protects newcomers from the financial impact of a serious illness. While provincial health care covers many treatment costs, it does not replace lost income or pay for many everyday expenses during recovery. Here’s why critical illness insurance can be especially beneficial for newcomers:

- Income replacement: Whether your loved ones live in Canada or abroad, a serious illness can make it difficult to meet ongoing financial commitments. A lump-sum payment helps ensure your family’s finances stay on track if you are unable to work during recovery

- Lack of employee benefits: Many newcomers, such as work permit holders, don’t have employer-sponsored critical illness coverage upon arrival. Even if you do, workplace benefits may be limited or end when you change jobs

- Ensures peace of mind during recovery: Serious illnesses such as cancer, stroke, or heart attack can require extended time away from work. Critical illness insurance provides financial flexibility while you focus on recovery instead of worrying about bills.

- Health care expenses can still add up. Even with provincial health coverage, serious illnesses such as cancer, heart attack, or stroke can create high out-of-pocket costs. Prescription drugs, rehabilitation, home care, medical equipment, travel for treatment, and alternative therapies may not be fully covered

How does critical illness insurance work in Canada?

The following example illustrates how a critical illness insurance policy pays benefits after a covered diagnosis.

Suppose Raj, a 35-year-old newcomer to Canada, purchases a critical illness insurance policy with a $100,000 benefit. Two years later, he is diagnosed with cancer, a condition covered under his policy. After meeting the policy’s survival period requirement (mostly 30 days) and completing the claims process, Raj receives a tax-free lump-sum payment of $100,000.

He can use this lump-sum amount for the following or any other financial needs:

- Replacing income while taking time off work for treatment and recovery

- Covering prescription drug and rehabilitation costs not fully paid by provincial health care

- Paying a mortgage or rent and household bills

- Hiring child care or in-home care services

- Supporting family members in Canada or abroad

The benefit is paid regardless of his actual medical expenses, and Raj does not need to submit receipts or explain how the money is spent.

What illnesses are covered by critical illness insurance?

Most critical illness insurance policies in Canada cover major medical conditions that can have a significant impact on your health, income, and quality of life. The exact list of what is covered under critical illness varies by insurer and policy, but coverage includes:

- Cancer (life-threatening)

- Heart attack

- Stroke

- Coronary artery bypass surgery

- Kidney failure

- Major organ transplant

- Multiple sclerosis

- Parkinson’s disease

- Alzheimer’s disease

- Blindness

- Deafness

- Paralysis

- Loss of speech

- Severe burns

How much critical illness insurance can a newcomer get in Canada?

Critical illness insurance availability for newcomers depends on their immigration status, employment situation, and the insurer’s underwriting rules. While permanent residents generally have access to the highest coverage amounts, work permit holders may face lower limits and fewer insurer options.

Coverage limits by immigration status:

| Immigration status | Maximum critical illness coverage |

| Permanent resident | No fixed cap, all insurers offer maximum coverage (subject to product maximums and underwriting) |

| Skilled work permit (TEER 0-1) | $250K-$2M |

| Skilled work permit (TEER 2-3) | $250K-$1M |

| Lower-skilled work permit (TEER 4-5) | $50K-$500K |

| Post-Graduate Work Permit (PGWP) | $100K-$250K |

| Caregiver/nanny | $50K-$500K |

| Study permit | Available with only a few insurers for coverage up to $100K |

| Provincial nominee / CSQ | $250K-$2M |

| Convention refugee / protected person | Available with only a few insurers for coverage up to $100K |

| Spouse / dependent of an eligible resident | Typically, up to 50% of the primary insured’s coverage |

| Foreign-trained physicians / skilled professionals | $500K-$2M |

| Visitor/tourist/Super Visa | Not eligible |

Note: The range above reflects the limit across the broad panel of insurance companies. Your individual limit will depend on your specific immigration status, occupation, health profile, income, and the insurer’s underwriting requirements.

Critical illness insurance in Canada by immigration status

Depending on the immigration status, the coverage will vary. Here’s a detailed breakdown of critical illness insurance in Canada by immigration status:

1. Critical illness insurance for permanent residents

Permanent residents (PR) have the broadest access to critical illness insurance in Canada. Permanent residents are treated the same as Canadian citizens and have the same coverage and eligibility requirements.

- Insurers offering critical illness coverage: Most major insurers, including Assumption Life, Beneva, RBC Insurance, Sun Life, Manulife, and others, offer permanent residents the same critical illness plans, riders, and optional benefits available to Canadian citizens

- Coverage amount available: The maximum coverage amount available for critical illness coverage is the same as that of permanent residents. Permanent residents in excellent health may be eligible for preferred underwriting classes and lower premiums, just as Canadian citizens are. For instance, Empire Life offers preferred rates

- Eligibility requirements: Most insurers do not require a minimum period of residence in Canada before a permanent resident can apply for critical illness insurance. They will simply verify your PR status during underwriting. However, Beneva and Canada Life require a hepatitis report for adults who have lived less than one year in Canada

2. Critical illness insurance for work permit holders and foreign workers

Work permit holders in Canada can qualify for critical illness insurance, but eligibility and coverage limits depend heavily on their occupation and skill level. Insurers generally group work permit holders into different categories based on Training, Education, Experience, and Responsibilities (TEER):

- Skilled work permit (TEER 0-1): Management and professional occupations that typically require a university degree, such as physicians, engineers, accountants, lawyers, and software developers.

- Skilled work permit (TEER 2-3): Technical, skilled trade, and college diploma occupations, such as electricians, plumbers, dental assistants, technicians, and administrative professionals.

- Lower-skilled work permit (TEER 4-5): Occupations that generally require a high school diploma or short-term job-specific training, such as labourers, food service workers, retail staff, and certain caregiving roles

Based on these categories, the coverage for critical illness insurance will vary:

TEER 0-1

- Insurers offering critical illness coverage: All top insurers, including Assumption Life, BMO Insurance, Canada Life, Manulife, Empire Life, and others

- Coverage amount available: Sun Life and Manulife offer the highest coverage, up to $2M. While other top insurers like Beneva and Empire Life offer up to $500K in coverage, others, including Equitable Life and iA Financial, offer only up to $ 100K

- Eligibility requirements: The coverage for critical illness is eligible as soon as the work permit holders arrive in Canada, and if they have a valid work permit with at least three months remaining. Some insurers may require higher limits. For instance, Assumption Life offers critical illness coverage if the work permit is valid for at least one year and does not expire within the first three months

TEER 2-3

- Insurers offering critical illness coverage: Assumption Life, Beneva, BMO Insurance, Canada Life, Desjardins, Empire Life, Equitable Life, iA Financial, Manulife, RBC Insurance, and Sun Life

- Coverage amount available: For TEER 2–3 skilled workers, the coverage amounts are generally lower than those available to highly skilled professionals in TEER 0-1 occupations. Sun Life critical illness insurance plan provides the highest available coverage, with limits of up to $2M for eligible applicants. Canada Life follows with coverage of up to $1M, while insurers such as Desjardins, Manulife, and Empire Life offer up to $500K

- Eligibility requirements: In terms of eligibility, Canada Life requires proof of employment and evidence that the applicant is actively working in their field, while Manulife generally requires participation in a provincial nomination program and prefers applicants who have lived in Canada for at least six months. Otherwise, all other insurers require the same work-permit rules as TEER 0/1

TEER 4-5

- Insurers offering critical illness coverage: All top insurers, excluding Manulife, offer critical illness coverage

- Coverage amount available: For TEER 4-5 workers, critical illness insurance coverage options are more limited. Sun Life offers the highest coverage in this category, too, with limits ranging from $250K to $500K. BMO Insurance follows with coverage of up to $250K, while insurers such as Beneva, Empire Life, Equitable Life, iA Financial, and Desjardins generally offer up to $100K in coverage

- Eligibility requirements: The same work-permit rules apply as for other teers. However, there are exceptions, for example, Empire Life requires applicants to have been in Canada for at least three months and provide a letter confirming their intent to remain in Canada. Meanwhile, Desjardins offers higher coverage limits to applicants who have filed or received a permanent residence application

3. Critical illness insurance for Post-Graduate Work Permit (PGWP)

A Post-Graduation Work Permit (PGWP) allows eligible international students who have graduated from a designated Canadian post-secondary institution to live and work in Canada temporarily.

- Insurers offering critical illness coverage: Assumption Life, Beneva, BMO Insurance, Canada Life, Desjardins, Empire Life, Equitable Life, iA Financial, Manulife, RBC Insurance, and Sun Life

- Coverage amount available: Most insurers offer coverage ranging from $100K to $250K. BMO Insurance, Desjardins, Equitable Life, Manulife, and Sun Life offer up to $250K in critical illness coverage, while Canada Life, Empire Life, Beneva, and iA Financial generally provide up to $100K

- Eligibility requirements: The eligibility requirements will vary; however, most insurers will require a work permit. Equitable Life require the PGWP to remain valid for at least three months beyond the application date, while Canada Life may request a WP-EXT for PGWP letter (IMM 0127E) or study permit details if the work permit has not yet been issued

4. Critical illness insurance for caregiver/nanny

Caregivers and nannies working in Canada on a valid work permit may qualify for critical illness insurance, although coverage limits are generally lower than those available to skilled workers and permanent residents.

- Insurers offering critical illness coverage: Assumption Life, Beneva, BMO Insurance, Canada Life, Desjardins, Empire Life, Equitable Life, iA Financial, Manulife, RBC Insurance, and Sun Life

- Coverage amount available: Sun Life offers the highest standard coverage limit of up to $500K, while insurers such as Empire Life, iA Financial, Manulife, and Beneva offer up to $100K. Canada Life and BMO Insurance provide up to $50K in critical illness coverage. Coverage limits may increase if you have applied for permanent residence. For example, Sun Life offers coverage ranging from $100K to $500K, with higher limits available to caregivers who have filed a permanent residence application and have lived in Canada for at least three months

- Eligibility requirements: Needs a valid work permit and 3+ months in Canada. Manulife critical illness insurance plan requires 6+ months of residence in Canada

5. Critical illness insurance for international students

International students studying in Canada may qualify for critical illness insurance, but insurer options are limited, and coverage amounts are generally lower than those available to permanent residents and work permit holders.

- Insurers offering critical illness coverage: Assumption Life, Canada Life, Desjardins, iA Financial, and RBC Insurance offer critical illness coverage under their student category

- Coverage amount available: Assumption Life offers the broadest access, while Canada Life, Desjardins, and iA Financial offer up to $100K in critical illness coverage

- Eligibility requirements: Most insurers require proof of full-time enrolment at a Canadian school, college, or university, along with evidence of the student’s intention to remain in Canada

6. Critical illness insurance for provincial nominee / CSQ

Provincial Nominee Program (PNP) candidates and Quebec Selection Certificate (CSQ) holders generally have access to some of the highest critical illness insurance limits available to newcomers. Because these applicants have already been selected by a province or territory for permanent residence, insurers often view them as lower-risk long-term residents and provide broader coverage options.

- Insurers offering critical illness coverage: Assumption Life, Beneva, BMO Insurance, Canada Life, Desjardins, Empire Life, Equitable Life, iA Financial, Manulife, RBC Insurance, and Sun Life

- Coverage amount available: Sun Life and Manulife offer the highest critical illness coverage limits of up to $2M, while Canada Life provides up to $1M. Beneva and BMO Insurance offer up to $250K, while Empire Life and Desjardins provide up to $500K

- Eligibility requirements: Most insurers require a copy of the nomination certificate, approval letter, or Quebec Selection Certificate before approving coverage. Some insurers offer coverage immediately after nomination. For example, Beneva makes critical illness insurance available as soon as the applicant arrives in Canada, provided they can show proof of nomination. BMO, on the other hand, requires a 6+ month stay in Canada

7. Critical illness insurance for convention refugee / protected person

Convention refugees and protected persons can qualify for critical illness insurance in Canada, but insurer options are significantly more limited than those available to permanent residents, work permit holders, or provincial nominees.

- Insurers offering critical illness coverage: Beneva, Canada Life, iA Financial, RBC Insurance, Sun Life

- Coverage amount available: Beneva, iA Financial, and Sun Life offer up to $100K in critical illness coverage, while Canada Life provides up to $50K

- Eligibility requirements: Requires at least six months of residence in Canada, full-time employment, an IRB Notice of Decision, and proof of a permanent residence application. The eligibility varies; for instance, iA Financial generally makes critical illness insurance available only after the applicant has lived in Canada for at least one year, while Sun Life requires at least three months of residency in Canada and the intent to stay

8. Critical illness insurance for the spouse / dependent of an eligible resident

Spouses and dependents of newcomers may qualify for critical illness insurance in Canada. Many insurers assess spouses and dependents based on the same underwriting category as the principal insured person.

- Insurers offering critical illness coverage: Assumption Life, Beneva, BMO Insurance, Canada Life, Desjardins, Empire Life, Equitable Life, iA Financial, Manulife, RBC Insurance, and Sun Life

- Coverage amount available: Beneva offers some of the strongest spouse coverage options. Eligible spouses can receive critical illness coverage of up to 100% of the primary insured’s coverage amount, subject to a maximum benefit of $100K. Most insurers limit coverage to a percentage of the primary applicant’s coverage amount. For example, Empire Life, Manulife, and Sun Life offer critical illness coverage of up to 50% of the spouse’s or parent’s coverage amount

- Eligibility requirements: Dependants are generally required to live in Canada, but eligibility varies by insurer. While most insurers may follow the primary policyholder’s eligibility, insurers such as Manulife and Desjardins may impose additional requirements based on marital status, immigration status, or the applicant’s relationship to the primary insured

9. Critical illness insurance for foreign-trained physician / skilled professional

Foreign-trained physicians and other highly skilled professionals generally qualify for higher coverage amounts for critical illness. Because these applicants typically fall within TEER 0-1 occupations and have strong earning potential, many insurers offer higher coverage limits and broader product access.

- Insurers offering critical illness coverage: Assumption Life, Beneva, BMO Insurance, Canada Life, Desjardins, Empire Life, Equitable Life, iA Financial, Manulife, RBC Insurance, and Sun Life

- Coverage amount available: Coverage amounts are among the highest available to newcomers. Sun Life, Canada Life, and Manulife offer up to $2M in critical illness coverage, while insurers such as Beneva, Empire Life, and Equitable Life provide up to $500K. Empire Life may offer preferred health rates to eligible professionals with strong health profiles, resulting in lower premiums

- Eligibility requirements: Typically requires an employment contract, a PR application, a valid work permit, and 3+ months in Canada. Desjardins and Empire Life may require participation in a provincial nominee program or proof of a valid work permit

Who is not eligible for critical illness insurance in Canada?

If you fall into any of these categories, you might not be eligible to get critical illness insurance in Canada:

- Visitors, tourists, and business (short-stay) visa holders

- Asylum claimants who are still awaiting an IRB decision

- Non-conventional refugees and seasonal workers

- Super Visa holders

How much does critical illness insurance cost for newcomers?

The cost of critical illness insurance for newcomers increases with age. For a $100,000 policy, monthly premiums typically range from $19.62 to $617.49 for males and $22.41 to $458.91 for females, depending on age and underwriting factors. However, the exact cost of critical illness insurance for newcomers is based on many of the same factors as it is for Canadian citizens, including your age, sex, smoking status, coverage amount, policy type, and overall health.

Cost of critical illness insurance for newcomers

| Age (in years) | Male (monthly premium) | Female (monthly premium) |

| 25 | $19.62 | $22.41 |

| 35 | $32.85 | $37.26 |

| 45 | $70.65 | $68.67 |

| 55 | $185.31 | $137.52 |

| 65 | $617.49 | $458.91 |

Disclaimer: Illustrated monthly premiums are based on $100,000 of critical illness coverage, a 20-year term, non-smoking status, and no optional riders. Actual rates may vary based on underwriting.

How much does Critical Illness Insurance cost?

Get instant quotes from Canada's top critical illness insurance providers and find the perfect coverage for your family.

Powered by

![]()

Common mistakes newcomers make when buying critical illness insurance

Many newcomers focus on getting coverage quickly but overlook important details that can affect their future claims. Listed below are the common mistakes that newcomers should avoid when buying critical illness coverage:

- Waiting too long to buy coverage: Many newcomers postpone buying critical illness insurance until they are fully settled in Canada. However, premiums increase with age, and developing a health condition later could make coverage more expensive or difficult to obtain

- Choosing the lowest premium instead of the right coverage: A cheaper policy may cover fewer illnesses or offer a lower benefit amount. It is important to compare what is covered, not just the monthly cost

- Underestimating how much coverage you need: Many newcomers only consider medical expenses when choosing a coverage amount. But, critical illness insurance is used to replace lost income, cover mortgage payments, pay for child care, or fund recovery-related expenses, and hence choosing the right coverage is important

- Not checking eligibility requirements: Coverage rules vary by immigration status and insurer. Some policies require a valid work permit, proof of permanent residence application, or a minimum period of residency in Canada. Failing to meet these requirements can lead to delays or a declined application

- Overlooking policy exclusions and definitions: Each insurer has specific definitions and survival period requirements for covered illnesses. Understanding these details before purchasing a policy can help prevent surprises at claim time

- Not disclosing medical information accurately: Providing incomplete or inaccurate information on your application can result in a denied claim or policy cancellation. Always answer health and lifestyle questions honestly and completely

- Assuming all insurers treat newcomers the same way: Coverage limits, underwriting requirements, and eligible immigration categories differ significantly between insurers. Comparing multiple providers can help you find more favourable coverage and pricing

How do I apply for critical illness insurance as a newcomer?

Here are the steps you need to follow to apply for critical illness insurance as a newcomer with PolicyAdvisor:

- Consult our advisors: Speak with our licensed advisors to assess how much coverage you need based on your income, financial obligations, family responsibilities, and recovery-related expenses

- Compare plans from multiple insurers: Our advisors will help you compare critical illness insurance quotes and coverage options from Canada’s leading insurance companies, including plans available to permanent residents, work permit holders, students, and other newcomer categories

- Review your eligibility: Our experts will explain insurer-specific requirements, coverage limits, residency rules, and underwriting conditions that may apply to your immigration status

- Complete your application: Submit the required documents, such as your work permit and any medical information requested by the insurer. Our advisors will guide you through each step of the application process

- Review your coverage: Once your application is approved, review your policy details, covered illnesses, exclusions, waiting periods, and optional benefits before activating your coverage.

Our advisors will help you finalize the paperwork and ensure your policy is set up correctly. So, schedule a call now!

Frequently asked questions

Can newcomers buy critical illness insurance in Canada?

Yes, newcomers can buy critical illness insurance in Canada, but eligibility depends on their immigration status. Permanent residents typically have the widest access to coverage, while work permit holders, international students, caregivers, and other temporary residents may face coverage limits or additional underwriting requirements.

What illnesses are covered by critical illness insurance?

Most policies cover major conditions such as cancer, heart attack, stroke, coronary artery bypass surgery, kidney failure, major organ transplant, and multiple sclerosis. The exact list of covered illnesses varies by insurer and policy.

Is critical illness insurance worth it for newcomers to Canada?

Critical illness insurance can provide valuable financial protection if you are diagnosed with a serious illness. The tax-free lump-sum benefit can help replace lost income, mortgage payments, child care costs, travel for treatment, and other expenses that may not be covered by provincial health insurance.

Can work permit holders qualify for the same critical illness coverage as permanent residents?

No, work permit holders may not qualify for the same critical illness coverage as permanent residents. While some highly skilled workers (TEER 0-1) can access coverage of up to $2 million, many work permit holders face lower coverage limits and additional eligibility requirements. Insurers consider your occupation, permit validity, Canadian residency history, and permanent residence application when determining eligibility.

Can my spouse or dependents get critical illness insurance if I am a newcomer?

Yes, many insurers allow spouses and dependents of eligible newcomers to apply for critical illness insurance. Coverage is mainly linked to the primary applicant’s immigration status and coverage amount, with some insurers offering benefits equal to 50% to 100% of the primary insured’s coverage.

Can convention refugees and protected persons get critical illness insurance in Canada?

Yes, but options are limited when it comes to critical illness insurance for convention refugees and protected persons. Only a few insurers, including Beneva, iA Financial, and Sun Life, offer critical illness insurance to convention refugees and protected persons, and coverage amounts are typically capped at $50K to $100K, depending on the insurer.