A single emergency room visit or hospitalization in Canada can cost thousands of dollars. MSH visitors to Canada Insurance helps cover those unexpected costs with up to $1,000,000 in emergency medical benefits for trips up to 365 days, plus 24/7 multilingual assistance.

Quick review: MSH Discover Canada visitors to Canada Insurance

| PolicyAdvisor Rating | 4/5 |

| Best for | Visitors seeking comprehensive medical coverage with high policy limits |

| Skip if | You are above 80 with pre-existing conditions |

What is MSH Discover Canada visitors to Canada Insurance?

MSH visitors to Canada Insurance is a comprehensive travel insurance plan with coverage of up to $1,000,000 that includes support for stable pre-existing conditions, along with 24/7 emergency assistance and maternity coverage.

Key features of the MSH Discover Canada visitors to Canada insurance plan

| Feature | Details |

| Plan options | One core plan with multiple coverage amounts and a deductible option |

| Age eligibility | 15 days to 89 years |

| Maximum coverage amount | Up to $1,000,000 |

| Deductible options | $0, $100, $250, $500, $1,000, $3,000, $5,000, $10,000, $25,000 |

| Waiting period | If you purchase your policy after you arrive in Canada:

|

| Maximum policy duration | 365 days |

| Monthly payment option | Not available |

| Pre-existing conditions | Yes, if the condition (or related symptoms) has been stable for:

|

Need insurance answers now?

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

What does MSH visitors to Canada Insurance cover?

MSH Discover Canada visitors to Canada insurance offers a comprehensive range of emergency medical benefits, with up to $1,000,000 in coverage. It includes benefits such as hospitalization, physician services, ambulance service, diagnostic tests, and maternity care.

Here’s a rundown of the MSH Discover Canada visitor to Canada insurance plan:

| Benefit | Details |

| Emergency hospitalization | Up to $1,000,000 or the selected policy limit |

| Services of a physician, surgeon, and in-hospital nurse | Up to the policy limit |

| Maternity benefits | Up to $5,000 |

| Diagnostic services | The plan covers laboratory tests and X-rays ordered by an attending physician. You must obtain advance approval from Intrepid 24/7 for MRI, CAT scans, cardiac catheterization, sonograms, ultrasounds, and biopsies. |

| Prescription drugs | Up to $2,000 (maximum 30-day supply) |

| Additional wellness benefits (not subject to deductible) | Includes the following services every 12 months, after continuous coverage of 6 to 9 months:

Great for Super Visa applicants |

| Health practitioners | Up to $500 per profession |

| Transportation to the bedside | Economy airfare plus accommodations and meals up to $5,000 |

| Emergency dental | Coverage up to $4,000 for any injury and up to $500 for pain relief |

| Follow-up visits | The plan covers follow-up visits when a physician prescribes them as part of a covered emergency during the policy period |

| Repatriation | Up to $10,000 |

| Accidental Death and Dismemberment | $50,000 |

| Emergency return home | When approved and arranged in advance by Intrepid 24/7 |

| Out-of-pocket expenses | Up to $150 per day (maximum $3,000) for accommodations, meals, and other eligible costs due to a covered medical emergency |

| Flight accident benefit | $50,000 |

| Return of baggage | Up to $500 |

| Side-trip coverage | Included for eligible trips outside Canada, as long as most insured days (at least 51%) are spent in Canada |

Advisor insight: MSH Discover Canada stands out because it combines one of the highest coverage limits available for visitors to Canada with benefits that many competing plans do not include, such as maternity coverage and psychiatric care. However, travellers with complex health conditions should pay close attention to the policy’s stability requirements and exclusions before purchasing coverage.

Pros and cons of MSH Visitors to Canada Insurance

Who is eligible for MSH visitors to Canada insurance?

Any non-resident of Canada between 15 days and 89 years old who meets MSH’s definitions and medical eligibility criteria and is not covered by a provincial health care plan can apply for the visitor to Canada plan.

This includes tourists visiting Canada, new immigrants, Super Visa holders, work permit holders, and returning Canadians who are not currently covered by a provincial government health insurance plan (GHIP).

Who is not eligible for MSH Discover Canada visitor insurance?

You are not eligible for MSH travel insurance if you:

- Are 90 years of age or older on the policy effective date

- Are travelling against the advice of a physician

- Have been diagnosed with a terminal illness

- Have congestive heart failure

- Have new or undiagnosed symptoms requiring medical investigation

- Require assistance with activities of daily living (eating, bathing, dressing, functional mobility, and using the toilet) due to a medical condition or overall state of health

Does MSH Discover Canada visitor health insurance cover pre-existing conditions?

Yes, MSH Visitors to Canada Insurance offers coverage for pre-existing medical conditions that have been stable for 90 or 180 days, depending on age. Policyholders aged 70 and under have coverage for pre-existing conditions if they have been stable for at least 90 days, while those aged 71 to 80 require 180 days. Applicants above 80 do not have coverage for pre-existing conditions.

MSH visitors insurance considers a pre-existing condition stable if:

- You have not been hospitalized for the condition

- There has been no new diagnosis, treatment, or prescribed medication

- Your medication or treatment has not changed (other than routine insulin or generic substitutions)

- Your test results show no deterioration, and you have not experienced new, more frequent, or worsening symptoms

- You have not been referred to a specialist or are awaiting surgery or investigation results

How much does MSH Discover Canada visitor health insurance cost?

The cost of a visitor to Canada health insurance policy from MSH ranges from $130.20 to $281.10, depending on the age, coverage amount, duration, and health status.

Sample MSH visitor insurance cost (2026)

| Age | Premium without pre-existing condition coverage | Premium with stable pre-existing condition coverage |

| 25 | $130.20 | $178.80 |

| 35 | $134.40 | $208.20 |

| 45 | $147.30 | $219.90 |

| 55 | $147.30 | $219.90 |

| 65 | $159.30 | $281.10 |

*Premium cost for $100,000 in coverage for a visitor to Canada insurance plan for 30 days

How much does Visitor Insurance cost?

Get instant quotes from Canada's top travel insurance providers and find the perfect coverage for your trip.

Powered by

![]()

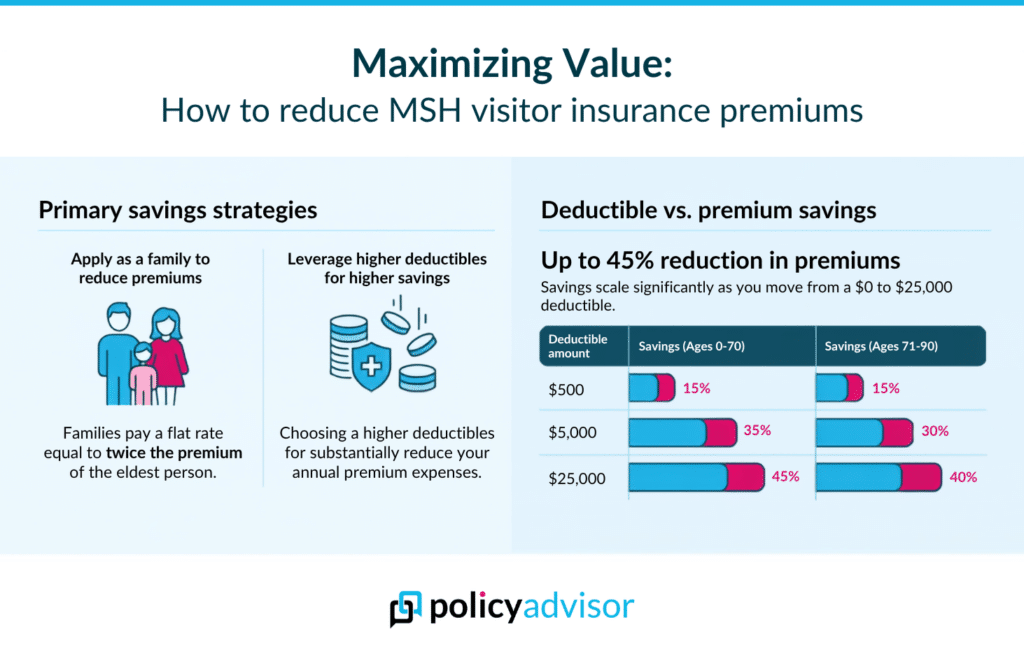

How to reduce the cost of MSH visitor health insurance?

To reduce your MSH Discover Canada Visitor to Canada Insurance premium costs, you can use two primary methods:

- Apply as a family: Pay a family rate equal to 2× the premium of the eldest insured person

- Select a higher deductible: Choose a higher deductible to lower your premium by up to 45%.

A deductible is the amount you pay out-of-pocket toward eligible medical expenses before your insurance starts covering costs. As a rule of thumb, a higher deductible results in lower premiums.

See how your MSH Discover Canada visitor to Canada insurance premiums change with different deductible amounts:

| Deductible amount | Premium reduction |

| $0 | 0% |

| $100 | 5% |

| $250 | 10% |

| $500 | 15% |

| $1,000 |

|

| $3,000 |

|

| $5,000 |

|

| $10,000 |

|

| $25,000 |

|

*Note that all deductible options, including the no-deductible ($0) option, are available to applicants aged 70 and under. The $100 and $250 deductible options are not available to applicants over age 70.

Are there any exclusions or limitations to MSH visitor health insurance?

Yes, there are certain exclusions and limitations to MSH Discover Canada visitor health insurance, such as medical tourism, claims resulting from alcohol or drug use, and more. While the plan offers comprehensive emergency coverage, certain conditions and procedures are not covered.

Here’s an overview of the general exclusions and limitations of the MSH travel medical insurance:

| Exclusion Category | What You Need to Know |

| Symptoms before coverage starts | Conditions or symptoms that would have reasonably required medical advice or treatment within the 90 days before coverage begins are not covered. |

| Elective, non-emergency, and ongoing care | Elective or cosmetic procedures, non-emergency treatment that can wait until you return home, routine or chronic care, rehabilitation, home care, investigative testing, and treatment after the emergency ends are not covered. |

| Policy timing and travel restrictions | Illnesses or injuries that occurred before a policy extension, travelling against a physician’s advice, terminal illnesses diagnosed before coverage, and medical treatment sought in your country of origin are excluded. |

| Medical tourism | Expenses are not covered if the policy was purchased primarily to obtain medical treatment outside your country of origin. |

| Transplants, prosthetics, and medical devices | Organ and bone marrow transplants, artificial joints, prosthetic devices, implants, and loss or replacement of eyeglasses, contact lenses, hearing aids, prosthetics, or prosthetic teeth are excluded. |

| Pregnancy and congenital conditions | Pregnancy that began before coverage, childbirth and related complications (except eligible maternity benefits), and congenital conditions in children under age two are excluded. |

| Mental health | Mental, emotional, and psychological conditions are excluded unless hospitalization is required or the policy specifically provides psychiatric/psychological benefits. |

| Alcohol, drugs, and illegal acts | Claims resulting from alcohol or drug use, criminal acts, or self-inflicted injuries (including suicide or attempted suicide) are not covered. |

| High-risk activities | Injuries sustained while participating in hazardous sports or activities, including professional sports, motor racing, parachuting, hang gliding, bungee jumping, mountaineering, certain scuba diving, or operating an aircraft as a pilot or crew, are excluded. |

Note: Refer to the policy document for the full list of limitations and exclusions

How do you file an MSH Discover Canada visitor insurance claim?

If you experience a medical emergency during your stay in Canada, you should contact Intrepid 24/7, MSH’s emergency assistance provider, as soon as possible to initiate the claims process. MSH offers 24/7 emergency assistance and direct billing where possible.

Here’s how you can initiate the MSH visitors insurance claim process:

- Call the assistance centre immediately: You can contact the assistance centre in Canada and the United States at 1-800-203-8508 and internationally at +1-416-646-3107. Failure to contact assistance within 24 hours and before surgery may make you responsible for 20% of eligible expenses

- Submit claim: Submit the fully completed claim form, which will be provided by Intrepid 24/7 upon notification of a claim

- Gather supporting documentation: You will need to provide medical records, proof of treatment expenses (including itemized bills and payment receipts), and travel documents such as your passport, visa, or airline ticket

- Submit proof of claim: Submit written proof of your claim to Intrepid 24/7 within 90 days of the illness or injury

Can you cancel or get a refund on MSH Discover Canada visitor insurance?

Yes, MSH visitor insurance allows policy cancellations and refunds under certain conditions. Your refund depends on whether coverage has started, whether you have filed claim, and the reason for cancellation.

Here is the MSH visitors insurance refund policy at a glance:

| Situation | Refund Eligibility |

| Changed your mind before coverage starts | Eligible for a full refund if cancelled before the effective date, including if you change your mind after purchasing or your trip is cancelled. |

| Super Visa application refused | Yes. Receive a full refund if you provide satisfactory proof of Super Visa refusal within 60 days. If proof is not provided, a $250 cancellation fee applies. |

| Leaving Canada early | Eligible for a prorated refund for the unused portion of the policy, subject to a $25 administration fee, proof of early return, and no paid or pending claims. |

| Eligible for provincial health coverage | Eligible for a prorated refund from the date provincial health coverage begins, subject to a $25 administration fee, proof of eligibility, and no paid or pending claims |

| Multiple visits to Canada | No refund for periods spent in your country of origin between separate trips to Canada |

| Claim submitted | Not eligible. No refund is available if a claim has been paid or is pending, regardless of the cancellation reason |

Can you extend MSH visitor insurance?

If you plan to stay in Canada beyond your current policy’s expiry date, you can purchase a new MSH Discover Canada policy to maintain your coverage. Essentially, it is not an extension of your existing policy but the purchase of a new policy. To avoid a coverage gap, you must apply before your current policy expires. Contact your broker or MSH directly to arrange your new policy.

You can purchase a new policy only under the following circumstances:

- You remain eligible for insurance

- You have not experienced any changes in your health since your effective date or arrival date

- The request for the new policy is received prior to the expiry date of your coverage

- The required premium is paid in full

It is worth noting that all policy exclusions, terms, and conditions will be based on the effective date of the new policy. Additionally, the cost to extend your insurance will be calculated based on your age on the effective date of the new policy, using the premium schedule in effect when the extension is requested.

In addition, MSH offers automatic extension of the policy for up to 72 hours at no extra premium. To activate this, you must notify Intrepid 24/7. Your policy automatically extends under the following circumstances:

- Travel delay: Your flight, bus, train, ferry, or other scheduled transportation is delayed beyond your control before your policy expires, and the transportation was due to arrive before the expiry date.

- Medical emergency: A covered sickness or injury makes you medically unfit to return home before your policy expires

- Hospitalization: You are hospitalized on your policy expiry date due to a covered sickness or injury. Coverage extends for the period of hospitalization plus 72 hours after discharge.

How does MSH Discover Canada compare to other visitor insurance options?

Here’s a quick overview of the MSH visitor health insurance policy compared to similar policies offered by GMS, TuGo, Allianz, and others:

| Provider | Pre-Existing Conditions Coverage | Monthly Payments | Maximum Coverage |

| MSH International Discover Canada | Yes, if stable (90 days ≤70 years; 180 days ages 71–80) | No | Up to $1,000,000 |

| GMS (Group Medical Services) | Yes, if stable for 180 days | No | Up to $150,000 |

| Manulife | Yes, if stable for 180 days (Enhanced Plan) | No | Up to $200,000 |

| Travelance | Yes, if stable for 180 days (Premier Plan; Essential Plan excludes pre-existing conditions) | Yes | Up to $150,000 |

| TuGo | Yes, if stable

|

No | Up to $500,000 |

| Allianz | Yes, if stable (90 days ≤59 years; 180 days ages 60–89) | No | Up to $500,000 |

| Destination Canada | Yes, if stable (90 days ≤59 years; 180 days ages 60–79) | Yes | Up to $300,000 |

| 21st Century | Yes, if stable for 180 days (Enhanced Plan) | Yes | Up to $200,000 |

| Secure Travel | Yes, if stable (90 days ≤69 years; 180 days ages 70–84) | Yes | Up to $1,000,000 |

For a comprehensive review and comparison, head over to our list of the best medical insurance for visitors to Canada (2026).

Our advisor’s take on MSH Discover Canada visitor health insurance

At PolicyAdvisor, we recently helped a 40-year-old visitor coming to Canada for an extended stay who wanted comprehensive emergency medical coverage with added benefits. They wanted a plan that offered strong medical protection, flexible deductible options, and extended coverage for multiple medical emergencies.

The client profile

- Age: 40

- Purpose of visit: Extended stay in Canada

- Primary concern: Comprehensive coverage with multiple benefits

- Coverage needed: $500,000 for a 365-day stay (Super Visa applicant)

Why we recommended MSH Discover Canada

While some visitor insurance plans focus primarily on emergency medical expenses, MSH provides a broader range of benefits and extended support that can be valuable during longer stays in Canada. The higher coverage amount of up to $1,000,000 also makes it easier for those seeking higher amounts.

We recommended the plan because it includes:

- Emergency medical evacuation and repatriation coverage

- Flexible deductible options that can help lower premiums

- Automatic extension of coverage due to cancelled flights or hospitalization on or before the expiry date

- The complimentary psychiatric, eye, vaccination, and physical examination services after six or nine months add another layer of protection and coverage

- Coverage extension options for travellers whose plans change while in Canada

- 24/7 emergency assistance and direct billing, where available, through Intrepid 24/7

How to purchase MSH Discover Canada visitor health insurance in Canada?

PolicyAdvisor’s licensed advisors help visitors find the right MSH Discover Canada visitors to Canada Insurance plan by comparing coverage limits, deductibles, and eligibility requirements based on their unique needs. Our advisors can also guide you through customizing your policy based on your age, health history, and plans during your visit.

Whether you are visiting family, applying for a Super Visa, or waiting for provincial health coverage to begin, our team can guide you through the policy’s coverage options, exclusions, and other features.

Frequently Asked Questions

Does MSH Discover Canada visitor medical insurance cover pre-existing medical conditions?

Yes, MSH visitor insurance covers pre-existing medical conditions, subject to age-based eligibility requirements and a stability period of 90 days for applicants aged 70 and under and 180 days for applicants aged 71 to 80. Applicants over 80 do not have coverage for pre-existing conditions.

Is MSH Discover Canada suitable for the Super Visa?

Yes, MSH is eligible for Super Visa insurance when the coverage amount is $100,000 or more in emergency medical coverage for one year, as required by the Canadian government’s Super Visa program.

What is the maximum coverage available under MSH visitor insurance?

MSH offers emergency medical coverage of up to $1,000,000, with variable deductible options ranging from $0 to $25,000

Does MSH visitors to Canada insurance include dental coverage?

Yes, MSH travel insurance includes up to $4,000 for accidental dental treatment and up to $500 for emergency dental pain relief.

Are side trips outside Canada covered by MSH Discover Canada visitors to Canada insurance?

Yes, MSH visitors to Canada insurance supports trips taken to other countries from Canada (the trip must start and end in Canada). To remain eligible for coverage during a side trip, you must have at least 51% of your covered days in Canada at the time of the claim. Note that the policy does not cover medical expenses incurred in your country of origin. Additional conditions apply.

What are the benefits of purchasing a visitor health insurance policy before arriving in Canada?

Purchasing an MSH visitor health insurance policy before arriving in Canada offers several benefits, including immediate coverage upon entry, protection against unexpected medical emergencies, and peace of mind during travel.