Curious about life insurance costs for a 50-year-old and over?

Your fifties mark a transformative period, bringing financial considerations like retirement, mortgage completion, and children’s education. As life events shift, so do your needs for financial planning and protection. Whether you’re exploring life insurance for the first time or looking to update coverage, understanding the costs is crucial.

Discover what term life insurance entails for those in their 50s and why considering it now is a smart move.

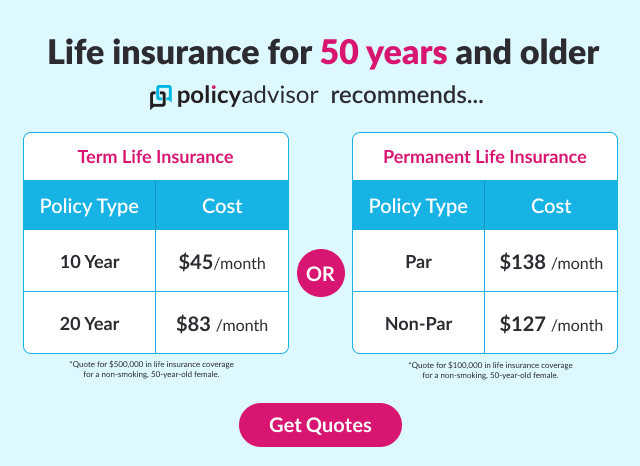

What is the average cost of term life insurance for age 50 and over?

The average price for life insurance in your 50s is $80-125 per month for about $500,000 worth of 20 year term life insurance coverage. This is an average price range—the exact monthly premium that you would pay depends on your specific personal and policy profile.

Term life insurance premiums are based on various factors like your specific health, gender, and lifestyle. Other factors, like your smoking status, having pre-existing health conditions, or participating in any extreme sports, can have an influence on your monthly cost of life insurance. Additionally, the type of policy you choose has an impact on the cost of your insurance.

Take a look at the chart below to understand what the average premiums are for a term life insurance policy in your fifties.

Life Insurance Premiums – Male, 20-Year Term Life Insurance

| Age | $250K | $500K | $1MM |

|---|---|---|---|

| 50 | $72 | $124 | $235 |

| 51 | $81 | $144 | $274 |

| 52 | $91 | $163 | $311 |

| 53 | $101 | $181 | $346 |

| 54 | $113 | $201 | $385 |

| 55 | $127 | $223 | $427 |

| 56 | $142 | $257 | $495 |

| 57 | $160 | $290 | $559 |

| 58 | $179 | $324 | $638 |

| 59 | $201 | $358 | $696 |

*Representative values, based on regular health

The story is similar for women in their fifties. The 20-year term life insurance rates for women who are 50-59 years old are lower than men’s at this age.

Life Insurance Premiums – Female, 20-Year Term Life Insurance

| Age | $250K | $500K | $1MM |

|---|---|---|---|

| 50 | $52 | $86 | $162 |

| 51 | $57 | $98 | $187 |

| 52 | $63 | $110 | $212 |

| 53 | $70 | $124 | $239 |

| 54 | $77 | $140 | $267 |

| 55 | $85 | $155 | $300 |

| 56 | $96 | $179 | $349 |

| 57 | $107 | $202 | $393 |

| 58 | $120 | $227 | $440 |

| 59 | $135 | $251 | $488 |

*Representative values, based on regular health

These are estimated prices for 20-year term life insurance rates for ages 50 and over based on representative data and will still vary depending on factors like health and medical exam results, smoking status (not just cigarettes), family medical history, and more. You may also want a higher death benefit or a longer year term depending on your financial situation, life insurance coverage needs, and all the other things that accompany life in your 50s.

Only you know how much coverage you require and can reasonably afford, but these numbers give an over-arching view of what the average cost of 20-year term life insurance for people who are 50 years old and over might pay for such coverage.

To get an exact quote, check out our easy quoting tool below! Simply enter your information and you’ll get a quote in seconds!

Why should I get life insurance in my 50s?

The reasons at this age vary. While you won’t take advantage of the low rates offered to someone in their 20s or 30s, life insurance is still relatively inexpensive for someone in their 50s who is in good health. And actually, if you find yourself not having suffered any critical or recurring illnesses yet, it might be time to secure a great rate. And if you happened to have developed any health concerns, you may want to think about exercising options available within your existing coverages and/or asking an experienced insurance broker to guide you through new plans you may want to establish. Luckily, the best online insurance broker in Canada can help.

Need insurance answers now?

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

How much life insurance does someone in their 50s need?

Before figuring the cost of life insurance at 50 years old and over, you need to know how much life insurance you should buy. Of course, the amount of life insurance you need at 50 years old depends entirely on your own personal situation – as we mentioned above.

However, there are some clear indicators of whether you need life insurance at the age of 50 and over:

- You are the main earner for your family, with dependents like your children, grandchildren, partner, or elderly parents

- You and your partner plan on spending the rest of your life together as you approach retirement

- You have children or grandchildren of any age

- You are paying for their education and plan to continue to pay for some of their education costs over the next few years

- You have a mortgage, or plan on buying or renovating your home in the near future

- You have other forms of debt like credit cards or a line of credit

- You are accumulating assets that you want to be able to transfer efficiently to your dependents

It makes sense that a Canadian in their fifties, with a remaining mortgage, children, and a partner also earning an income would need at least $500,000 in coverage to cover the last of the house payments, cost of living, and children’s education costs (or grandchild to spoil) in the next 20 years. However, like the Bermuda shorts you’ll need post-retirement, this isn’t one-size-fits-all. To find your specific life insurance coverage needs, try out our easy-to-use life insurance calculator.

With all this considered, let’s take a look at what 20 year term life insurance costs for a 50-year old for some representative amounts.

Which is the best life insurance at age 50 and over?

While you may have coverage through a group plan at your work – retirement is looming or you might find yourself in line for a final career change or promotion before you pack up the RV and live your twilight years sitting in a lawn chair in Arizona. In this case, you could find yourself with a gap in coverage or no coverage at all depending on your future plans. If you are dependent on group benefits for your life insurance at the moment, you should read why group plans can be lacking in life insurance coverage.

You may already have life insurance you purchased in your thirties or forties, but the plan, benefits, and options no longer suit your evolving needs. Be it marriage, children branching out on their own, or maturing mortgages, your financial and protection needs can change dramatically as you approach retirement age and consider life insurance as a senior – especially for such needs that are temporary in nature. Whether for full first-time coverage or to augment your existing insurance plans – the best term life insurance is simple and flexible insurance that can suit any of these situations.

How do I buy the best life insurance in my 50s?

You now have an idea of what term life insurance might cost as you approach this exciting stage of your life – but everyone’s situation is different. If you have 5 minutes to spare, you can determine your needs and get customized term life insurance quotes for a 50 year old instantly with PolicyAdvisor’s online term life insurance quote tool.

Still need help with your coverage needs? Try our life insurance needs calculator now. Otherwise, our licensed advisors are always here to chat.