About one-third of Canadians are currently without life insurance and 1 in 4 millennials in the country admit they are unlikely to purchase any kind of insurance in the near future.

The basics of life insurance are just not on our radars. So if you thought ‘Term to 100’ was the title of a Drake song, don’t be embarrassed, you’re not alone.

Life insurance 101 isn’t common knowledge in Canada, which is exactly why it’s a subject worth exploring, especially if you’ve increasingly found yourself in the company of real estate agents, in-laws, or babies.

But where to begin? Is a death benefit a charity concert? Does “participating insurance” come with a ribbon? Is “return-of-the-premium” a new Star Wars flick?

Let’s just start with the basics…

What is life insurance?

Life insurance is an agreement between you and a life insurance company. The agreement is if you die, they will pay a death benefit (a lump sum of tax-free money) to someone you choose. In exchange, you agree to periodically pay them an insurance premium: a small amount of money over time.

You both decide on the amounts of cash coming in and out and the timeframes involved, but in a super simplified form, that’s really it.

How does life insurance work?

Life insurance provides financial protection to your loved ones in the event of your death. There are four key aspects of how life insurance works:

- Agreement and premium payments: Life insurance is a contractual agreement between an insurance company and a policyholder. The policyholder pays monthly or annual premiums, and in return, the insurer agrees to pay a death benefit to the beneficiaries in the event of the policyholder’s death

- Beneficiary designation: Policyholders can designate both, primary and contingent beneficiaries. Minors cannot be named as primary beneficiaries

- Claim process: Upon the policyholder’s demise, the beneficiaries can file a claim process with the insurer by submitting essential documents. Once the documentation is verified, the insurance company will pay the lump sum death benefit to the primary beneficiary

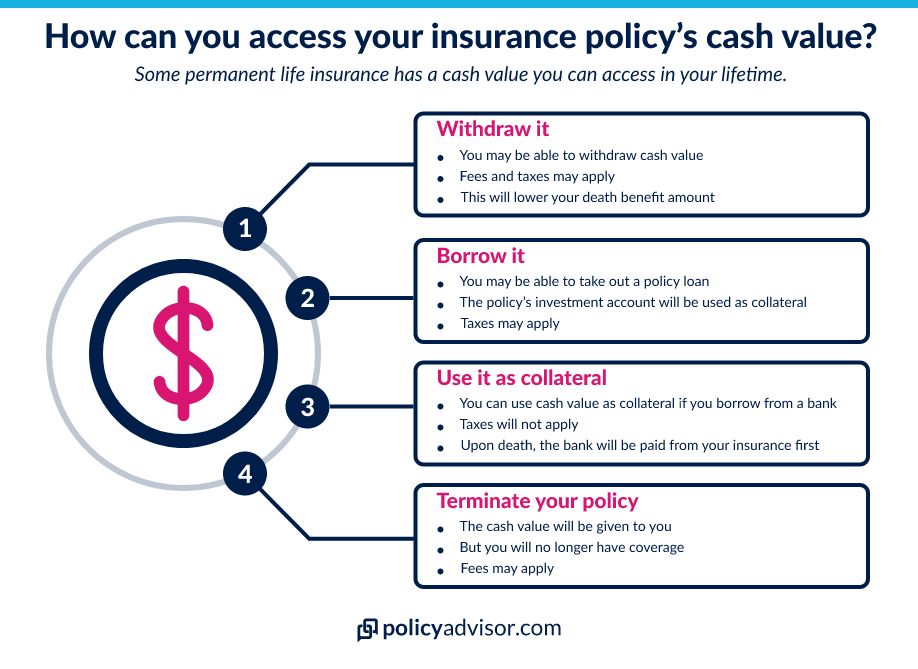

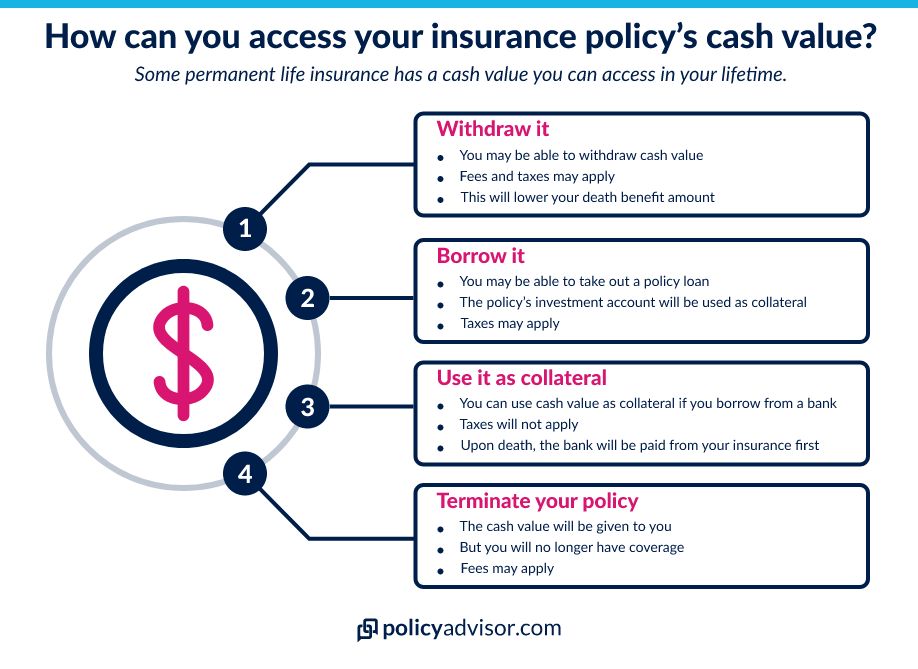

- Living benefits: Some permanent life insurance policies such as whole life insurance allow the policyholder to access a portion of the death benefit during their lifetime. This is known as cash value

What does life insurance cover?

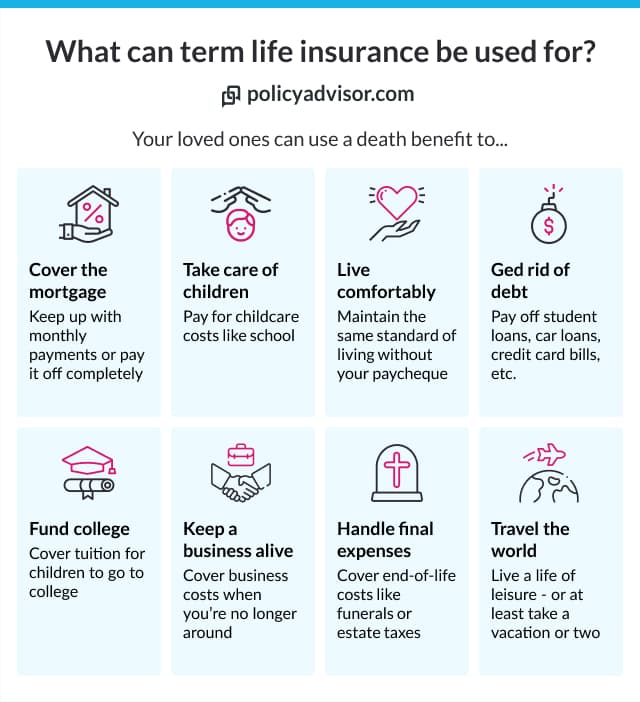

A life insurance policy payout can be used by the beneficiaries in any way they want to, including for:

- Funeral and burial expenses

- Replacing lost income

- Covering outstanding debts

- Funding your children’s education

- Covering everyday living expenses

Life insurance terminology

Here are some handy definitions for common life insurance terminology:

| Term | Definition |

| Policyholder | The person who owns the life insurance policy |

| Insured | The individual whose life is covered by the policy |

| Insurer | The company that provides life insurance coverage |

| Premium | The amount paid regularly to maintain the policy |

| Beneficiary | The person or entity designated to receive the death benefit |

| Death benefit | The amount paid to beneficiaries upon the insured’s death |

| Cash value | The savings component of a permanent life insurance policy that grows over time |

| Policy term | The length of time the insurance coverage is in effect |

| Riders | Additional provisions that can be added to a policy to customize coverage |

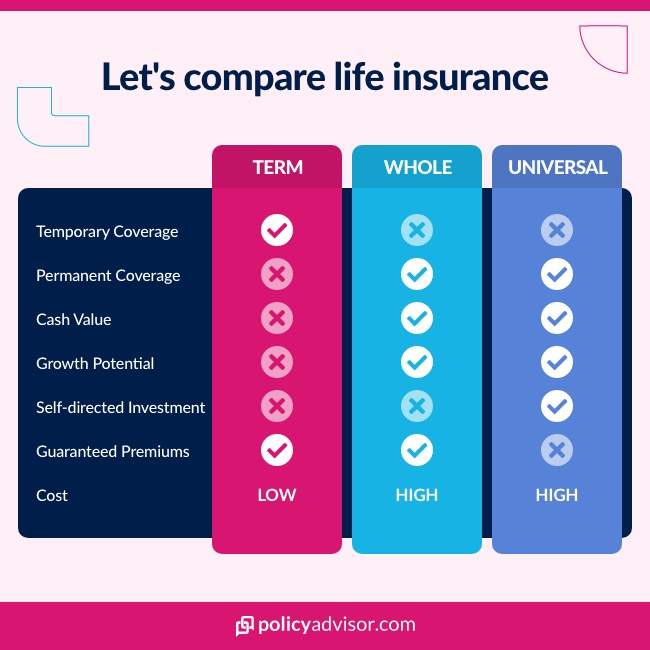

What are the different types of life insurance in Canada?

There are two main types of life insurance:

- Term life insurance, which lasts for a period of time called a term

- Permanent life insurance, which covers you for the rest of your life

Most Canadians wind up with term insurance, either through individual plans or through their employer as a group plan.

Learn more about the different types of life insurance.

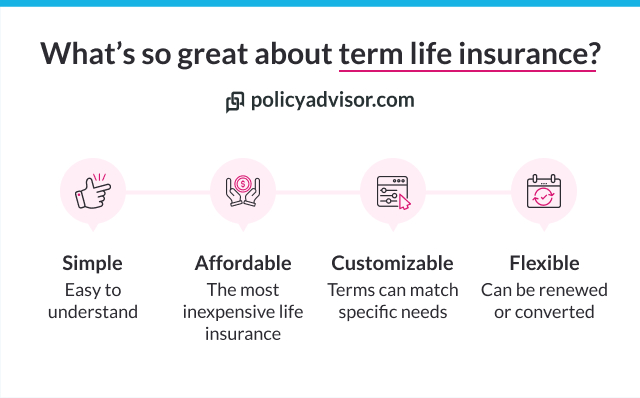

Term life insurance

Term life insurance makes the promise if you die, we’ll pay, but only if that were to happen within a specified period of time, or ‘term’. These terms are generally 10, 20, or 30 years, but you can choose smaller or larger term lengths or coverage that last until a specific age.

Whole life insurance

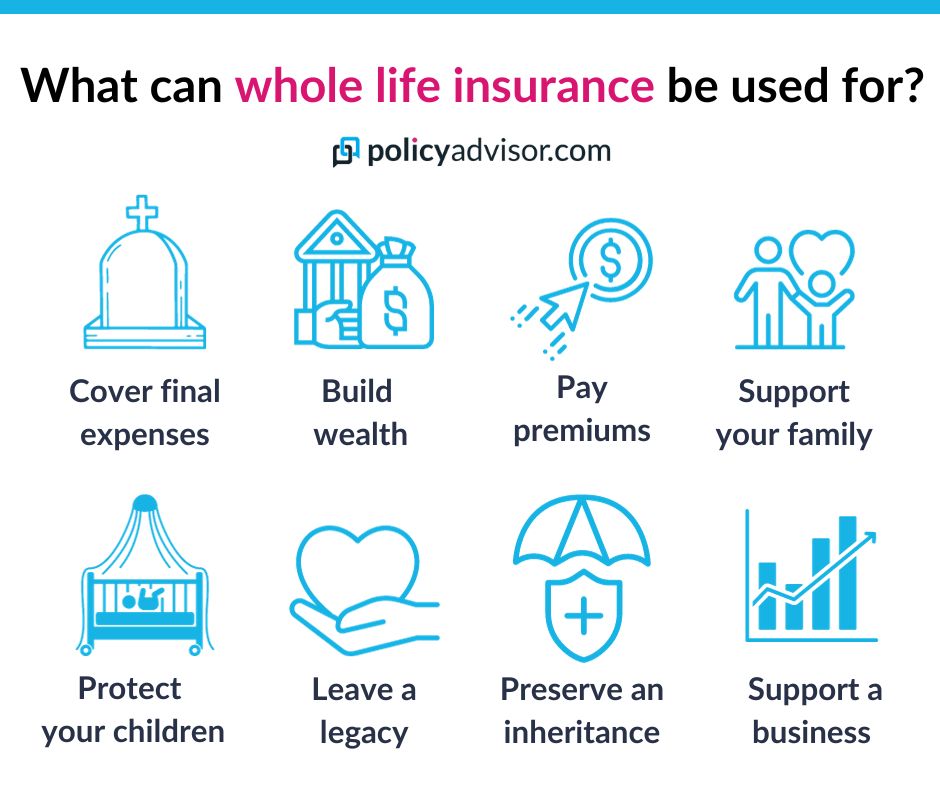

Whole life insurance covers you for your entire life and there is a cash value associated with your policy. Sometimes, whole life policies will also pay dividends based on the insurance company’s profits. This is known as participating insurance.

Limited-pay whole life insurance

Limited-pay insurance is similar to whole life, except the payment plan is condensed. For example, the term could be 20 years: once you’ve paid your premiums over that 20-year period, your insurance is guaranteed for life and you’re off the hook for premiums. This type of coverage is typically the most expensive policy option. This is because premiums are front-loaded to offset the years where you will no longer be paying.

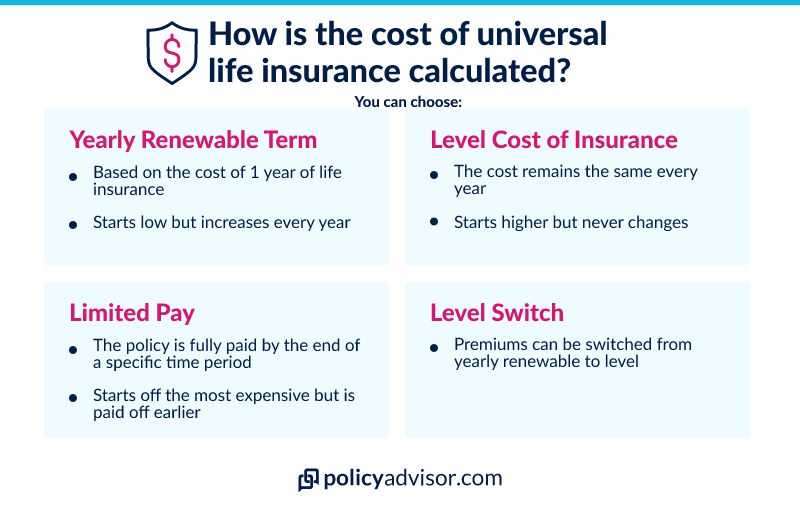

Universal life insurance

Universal life insurance is the same as whole life insurance, except you have more choice of where your cash value is invested. If you’re a savvy investor, this gives you the opportunity to generate a larger return than what is guaranteed from a traditional whole life policy. That said, it requires you to actively monitor the investment choices you’ve made with the cash value. Alternative investment solutions may help you achieve your financial goals faster.

Term to 100 life insurance

Even though the word term is in the name, term to 100 is a whole life insurance policy that covers you until your death. The difference is with this policy there is no cash value or investment component, making the premiums a little cheaper. As a bonus, if you do live beyond age 100, you are no longer required to pay premiums and retain your coverage. Term to 100 life insurance policies are unique to Canada.

Annual renewable term life insurance (ART)

A less popular life insurance option, annual renewable term life insurance (ART) is designed for those looking for short-term life insurance coverage. ART is available on an annual basis with the possibility of renewal and can protect people who are between jobs, who want to improve their health before locking in a longer-term policy, or those with short-term debt.

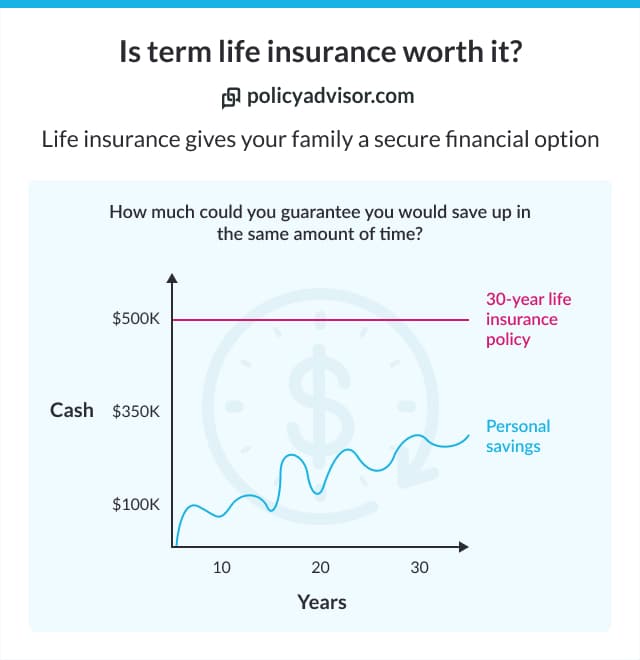

Is life insurance worth it?

If you have dependents, life insurance premiums are worth the cost. Life insurance provides peace of mind knowing that your family will be taken care of financially when you pass away.

If you don’t have dependents, there could be other circumstances where the benefits of life insurance is worth the price of premiums. These can include:

- Taking advantage of your youth and health to ensure a lower premium and future insurability

- Providing a charitable gift to your favorite cause or organization

- Leaving a financial gift or legacy to children or grandchildren, regardless if they are dependents or not

When should I buy life insurance?

Life events create the need for life insurance. Buying a home, having children, and getting married are good indicators that there are those in your life who depend on your income to maintain their quality of life. Premiums rise as you age, so purchasing insurance earlier in life can save you money.

Do I need life insurance?

Perhaps a better question is, do the people in your life need it?

Insurance is for clearing out debts (personal or business-related) and supplying an income replacement source to someone who relies on you because you’re no longer around.

Buying life insurance lets you secure assets for your family’s future by investing in an alternate income source. Without life insurance and the security of this death benefit, you’re putting all your family’s financial eggs in one basket: you, being alive and able to earn an income.

You may assume you have life insurance through your work’s group benefits, but such policies require a close look to ensure it covers everything you need.

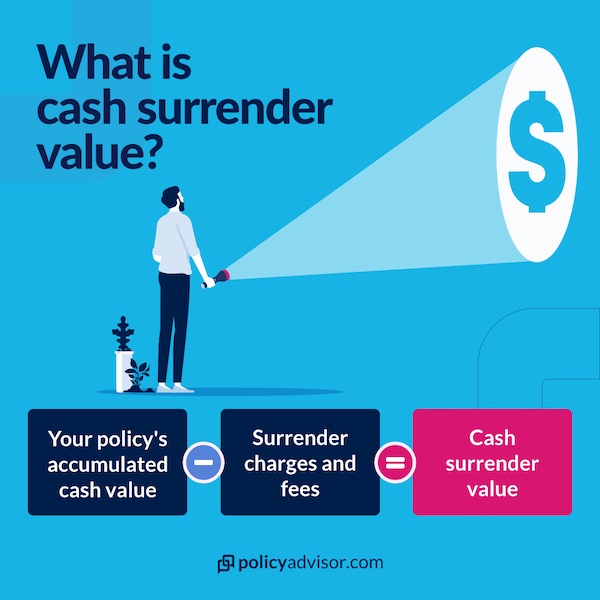

Does life insurance have cash value?

Permanent life insurance policies accumulate a cash value as the insurance companies invest your premiums. Policies such as whole life and universal life insurance have this investment feature. You can either cash it out, save it, loan against it, or apply the value to your existing policy.

Learn more about the cash value of life insurance.

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

How much does life insurance cost?

The cost of life insurance depends on several individual factors. For most young, healthy adults life insurance costs are quite reasonable on a 20-year term policy.

For instance, a 30-year old, non-smoking Ontario woman of average health, would only pay $21 per month for a $500,000 death benefit on a 20-year policy. If you’re personalizing your insurance policy so that it suits your specific needs and budget, life insurance can and should be affordable.

| Coverage | 10-Year Term | 20-Year Term |

|---|---|---|

| $250,000 | $11/month | $14/month |

| $500,000 | $15/month | $21/month |

| $1,000,000 | $23/month | $36/month |

Premiums for female, non-smoker, 30-years old

Personal factors affect your life insurance cost. Factors include:

- Age: Insurance premiums rise in cost as you age.

- Smoking Status: Smokers pay more for life insurance.

- Gender: Generally, men have higher life insurance premiums than women.

- Health: Insurance providers see health problems as adding to the risk of insuring you.

- Family Medical History: Insurance providers also calculate the risk of known hereditary illnesses.

Details of your life insurance policy will also affect the price of your monthly premium. These aspects include:

- Term Length: The longer your coverage period, the higher the premiums.

- Coverage Amount: A larger death benefit will also dictate higher insurance premiums.

- Type of Insurance: Term life insurance is less expensive than whole life insurance.

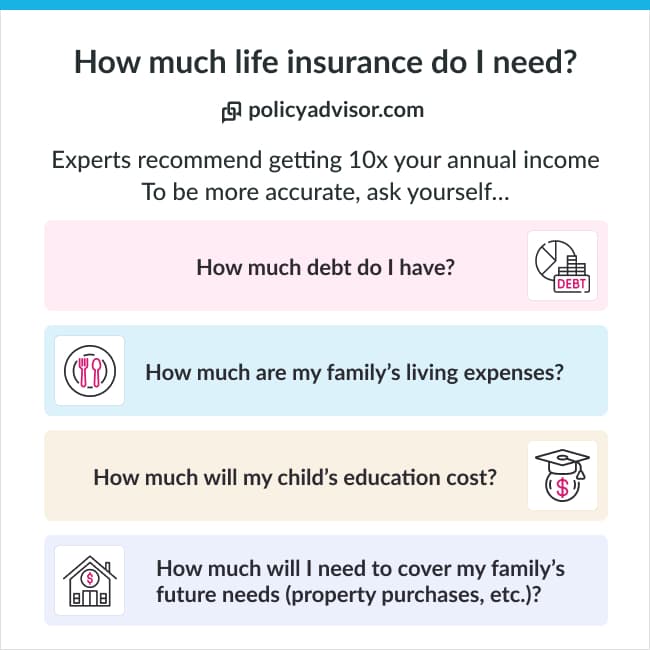

How much life insurance do I need?

You should get as much life insurance as you can afford. Most wish to leave a multi-million dollar fortune to their family and loved ones when they die. But that’s not financially realistic for most.

Determine what “affordable premium” means to you. Build a budget to assess your family’s current financial needs, their future needs, your current liabilities and debts, and any costs associated with your death. That’ll reveal what kind of coverage amount you should aim for and the costs associated with it.

Some use the 10x your annual income rule, but we highly recommend using our life insurance coverage calculator to get a quick but comprehensive recommendation.

Should I get life insurance through work?

Getting life insurance through work can be a convenient and cost-effective option, but it’s important to consider your specific needs and circumstances. Here are a few points to help you decide:

- Employer-provided life insurance is often easier to obtain and may come at a lower cost since it’s typically part of a group plan. The premiums are often subsidized by your employer, making it an affordable option

- While convenient, the coverage amount offered through work might be limited, often equating to one or two times your annual salary. This may not be sufficient to cover all your needs

- One of the downsides of employer-provided life insurance is that it’s not always portable. If you change jobs or lose your job, you might lose your coverage. Having a separate individual policy ensures that you maintain coverage regardless of your employment status

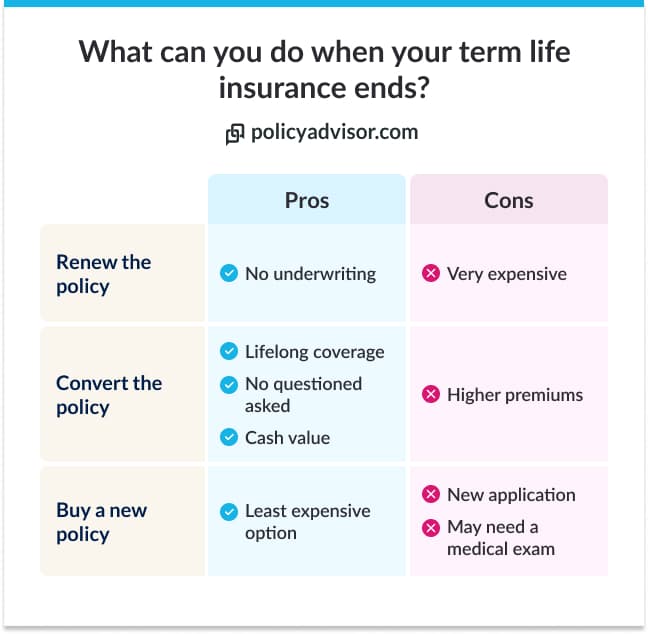

What happens to a term life insurance when it expires?

When your insurance policy expires you have several options. Typically you

- can convert a policy to whole life coverage

- renew the policy at a higher premium

- apply for a brand new life insurance policy

- let the coverage expire if you no longer need it

Learn more about what to do if you outlive your term life insurance policy.

Can I renew a term insurance policy?

Most term life plans come with a renewability clause, that lets you extend your coverage upon expiry without having to redo your medical exam.

The downside of renewing your coverage is the cost: your premiums are reassessed (increased) to match your older age. Thus, some Canadians prefer to apply for a new insurance policy at the end of the term.

What personal information do I need to share with my insurance company?

Life insurance companies have a mandatory set of questions they ask during the underwriting process. They include:

- your gender

- your age

- where you live

- whether you smoke

- your physical health history (cancer, diabetes, high blood pressure, sleep apnea)

- your mental health history (anxiety and/or depression, bipolar disorder, other mental health conditions)

- your family’s medical history

- how much you drink

- your history with drugs

- your passion for extreme sports

- how dangerous your job is

Based on your answers to these questions, you’ll be placed into a risk category and offered premiums accordingly.

Additional in-person medical exams will be required from time to time, especially when applying for larger coverage amounts.

Learn more about how to prepare for a life insurance medical exam.

What is an attending physicians statement?

The provider may also ask for a health report (called an attending physicians statement or APS) from your family doctor or any specialists you see about ongoing health conditions.

Who should you name as your life insurance beneficiaries?

Your beneficiaries are those you name in your policy that receive the death benefit when you die. It’s important to list the right people so that your policy’s payout is used as you intended. If you do not name a beneficiary or there is ambiguity at the time of your death then probate can affect your life insurance benefit.

Are there different types of beneficiaries?

Yes, there are revocable and irrevocable beneficiaries.

- Revocable Beneficiary: a beneficiary that can be changed without their consent.

- Irrevocable Beneficiary: a beneficiary that has to sign off on any changes to the policy, including coverage and beneficiary changes.

Should you name your children as beneficiaries?

In Canada, minor children cannot legally receive the funds from a life insurance policy until they reach the age of majority. Thus, many people create a trust to manage the funds of life insurance death benefits meant for their children.

A trust is an estate planning tool that allows you to choose another party (the trustee) to manage financial assets for a beneficiary until a pre-determined time or when they reach the age where they can legally manage their own funds.

Learn more about managing life insurance benefits with a trust.

Who needs life insurance in Canada and why?

Canadian life insurance can help different people with varying circumstances, like:

- Couples: Life insurance is important for couples, as it ensures that one partner’s death doesn’t create a financial burden for the surviving partner. It can help cover living expenses, debts, and future financial goals

- Business owners: Business owners should consider life insurance to protect their business interests. It can provide funds for succession planning, cover outstanding business debts, and help ensure the business continues smoothly in the event of their death

- Seniors: Seniors may need life insurance coverage to cover final expenses, such as funeral costs, and to leave a financial legacy for their heirs. It can also help with estate planning and ensure that the estate is not burdened with unexpected costs

- Parents with young children: Parents with young children should consider life insurance to secure their children’s financial future. It can help cover education costs, daily living expenses, and ensure that their children are cared for financially in their absence

- Single individuals: Single individuals without dependents may still benefit from life insurance. It can help cover personal debts, funeral costs, and leave a financial gift or charity donation

- Professionals with high incomes: High-income professionals often have significant financial responsibilities and goals. Life insurance can help protect their income, ensure the continuation of their lifestyle for their family, and address any large debts or estate taxes

- Parents with adult children: Parents with adult children may want life insurance to provide a financial cushion or to leave an inheritance. It can also help with estate planning and cover any remaining debts

- Individuals with significant debts: If you have substantial debts, such as a mortgage or student loans, life insurance can ensure that these debts are paid off and don’t become a burden to your loved ones

Should I add life insurance riders to my policy?

A life insurance rider is an optional feature added to your life insurance policy to better address your unique insurance needs. An insurance rider typically requires an additional payment which is added to your monthly premium, though some riders may also be included at no extra cost. There is a wide range of available riders. Common riders include additional term riders, critical illness riders, and guaranteed insurability.

Learn about life insurance for riders or read more about:

Which is the best life insurance policy?

The life insurance policy you should choose isn’t an answer in the back of the book. Life insurance is a deeply personal purchase and there are a lot of factors to consider. Not only should you factor in your family’s current financial needs, but you should also account for future costs like tuition fees, funeral arrangements, estate taxes, and any other debts or obligations you would want settled should you die. There a lot of options to choose from and a myriad of coverage combinations when you search for life insurance quotes. But, you should only purchase a policy you can afford and that you’re confident makes the most sense for you and your family.

Luckily, we’ve built a pretty great tool that can help you figure that out.

Head to our life insurance calculator, learn more about the best term life insurance or best whole life insurance in Canada, or check out the ratings below.

| Term Life Insurance Company | Rating |

|---|---|

| Assumption Life | ★★★★★ |

| Beneva | ★★★★ |

| BMO Insurance | ★★★★★ |

| Canada Life | ★★★★ |

| Canada Protection Plan | ★★★★★ |

| CIBC Insurance | ★ |

| Desjardins | ★★★★ |

| Empire Life | ★★★★★ |

| Equitable Life | ★★★★ |

| Foresters Financial | ★★★★ |

| Humania | ★★★★ |

| Industrial Alliance (iA) | ★★★★★ |

| ivari | ★★★ |

| Manulife | ★★★★★ |

| RBC Insurance | ★★★★★ |

| Sun Life | ★★★ |

| Wawanesa | ★★★★ |

Should I get life insurance for my children?

As a parent or grandparent, there are benefits to purchasing a life insurance policy for your child or grandchild. Life insurance for children ensures future insurability for your child, regardless of health issues. The policy also offers an effective way to build wealth and can be an attractive alternative to Registered Education Savings Plans (RESPs).

Do you need insurance to travel to Canada?

Certain visas that allow for travel or stays in Canada do require insurance coverage. Super visa insurance is mandatory for those seeking approval for their super visa status. While other visitors to Canada need insurance, it is not mandatory for entrance into the country.

Frequently asked questions

What does life insurance cover?

Life insurance provides a death benefit to your beneficiaries, which is typically tax-free. It can cover expenses such as funeral costs, outstanding debts, income replacement, education costs, and estate taxes, helping to ensure financial stability for your loved ones.

How does a term life insurance policy work?

A term life insurance policy offers coverage for a specific period, such as 10, 20, or 30 years. If the insured dies during this term, a death benefit is paid to the beneficiaries. If the term ends and the insured is still alive, the policy expires unless renewed or converted to a permanent policy.

How does life insurance payout work?

When a policyholder dies, beneficiaries file a claim with the insurer, providing a death certificate and policy details. Once the claim is approved, the insurer pays out the death benefit, usually as a lump sum, though other payout options may be available.

Why life insurance?

Life insurance ensures your loved ones are financially protected if you pass away. It helps cover living expenses, pay off debts, fund education, and manage estate planning, providing financial security for your family.

How to use life insurance while alive in Canada?

In Canada, permanent life insurance policies can offer access to cash value through loans or withdrawals. Some policies may also include riders for terminal or critical illnesses. You can also surrender the policy for its cash value, though this will end the coverage.

What are the tax implications of life insurance in Canada?

In Canada, life insurance death benefits are generally tax-free for beneficiaries. Permanent policies with cash value grow tax-deferred, but withdrawals or loans may be taxable if they exceed the premiums paid.

Employer-paid group life insurance is considered a taxable benefit to employees. If owned personally, life insurance bypasses probate, but corporate-owned policies may have tax implications.