Sun Life whole life insurance is one of Canada’s most trusted permanent coverage options. Founded in 1865, Sun Life has grown into a top-rated global insurer. With over 160 years of experience, Sun Life offers Canadians coverage that balances predictable growth, reliable cash value accumulation, and flexible options for long-term financial goals. It manages $1.62 trillion in assets and holds strong financial ratings, including A+ from A.M. Best and AA from S&P.

A key strength of Sun Life’s whole life insurance is its Participating Account, which holds approximately $21.2 billion in assets and supports over 400,000 active policies, one of the strongest par fund structures in Canada. In this review, we cover Sun Life’s key features, plan options, financial strength, and what makes it stand out among Canadian insurers.

Sun Par Accumulator II

Sun Par Accelerator

SunSpectrum Permanent Life II

10-pay

15-pay

20-pay

pay-to-100

PolicyAdvisor rating

Sun Life whole life insurance earns a 4.5 out of 5 rating from PolicyAdvisor for its strong appeal to high-net-worth Canadians who want global diversification, durable dividend performance, and industry-leading financial strength. Sun Life has one of the strongest par fund structures in Canada, with approximately $21.2 billion in assets supporting more than 400,000 active participating policies

Sun Life’s participating plans share in company profits through annual dividends. The Dividend Scale Interest Rate (DSIR) reflects par account performance and directly influences payouts. Sun Life maintains a 6.25% DSIR, supported by a diversified asset mix and stable underlying earnings.

Sun Life’s participating account financials:

- DSIR: 6.25%

- Participating fund size: $21.2 billion

- Underlying net income: $1.047 billion

- LICAT ratio: 154%

- Asset mix: 27.0% public bonds, 11.9% corporate bonds, 15.6% private fixed income, 8.7% commercial mortgages, 19.2% equities, 15.3% real estate, 2.3% cash/short-term

This diversified mix pairs fixed-income stability with equity and real-asset growth, helping support long-term dividend consistency.

See how much whole life insurance coverage you can get

Get instant quotes from Canada's top life insurance providers and find the perfect coverage for your family.

Powered by

![]()

The DSIR reflects Sun Life’s internal estimate of expected net returns after taxes, claims, and expenses. It influences pricing and dividend projections but is not a direct return to policyholders. Dividends depend on investment results, policyholder experience, and surplus allocation. The Board of Directors approves the final dividend each year, and rates may change.

| Period | DSIR |

| 2017–2021 | 6.25% |

| 2021–2022 | 6.00% |

| 2024–2026 | 6.25% |

The stable DSIR over the past decade reflects disciplined management of participating assets and resilient long-term performance.

Sun Life offers three participating whole life options:

- Par Accumulator II focuses on earlier cash-value growth and liquidity

- Par Protector II emphasizes long-term value and estate planning

- Par Accelerator drives faster early cash-value buildup for clients wanting quicker access to policy value

Rating methodology

PolicyAdvisor rates Sun Life whole life insurance 4.5/5 based on six factors: long-term dividend stability, early/long-term cash-value performance, premium flexibility, par fund strength, fees, and riders.

Dividend Scale - Participating Whole Life Insurance

Compare dividend rates from top Canadian insurers

| 2022 | 2023 | 2024 | 2025 | |

|---|---|---|---|---|

| Equitable | 6.05% | 6.25% | 6.40% | 6.40% |

| Manulife | 6.10% | 6.35% | 6.35% | 6.35% |

| iA Financial Group | 5.75% | 6.00% | 6.25% | 6.35% |

| Desjardins Insurance | 5.75% | 6.20% | 6.30% | 6.30% |

| RBC Insurance | 6.00% | 6.00% | 6.25% | 6.30% |

| Sun Life | 6.00% | 6.00% | 6.25% | 6.25% |

| Empire Life | 6.00% | 6.00% | 6.00% | 6.25% |

| Foresters Financial | 5.50% | 5.50% | 5.50% | 6.25% |

| Co-operators | 5.90% | 5.90% | 6.00% | 6.00% |

| Assumption Life | 5.75% | 5.75% | 5.75% | 5.75% |

| Canada Life | 5.25% | 5.50% | 5.50% | 5.75% |

Powered by

![]()

Pros and cons of Sun Life whole life insurance

The pros and cons of Sun Life whole life insurance show its mix of lifetime stability and growth potential. With three participating plans, one non-participating plan, and a guaranteed issue option, Sun Life’s whole life lineup offers something for every financial need. Here’s a quick look at the overall pros and cons.

Pros:

- Top-tier financial strength with Sun Life’s long history and scale

- Multiple payment-term options (life-pay, 10-pay, 20-pay, 8-pay) offering flexibility

- For participating plans, dividend participation adds value potential

- Non-participating and guaranteed plans offer predictable premiums and simpler structure

Cons:

- Premiums for whole life are significantly higher than term life insurance for the same face amount

- Dividends are non-guaranteed; participating plans carry variability

- In the non-par and guaranteed plans, growth is lower compared to participating options

- Whole life insurance from Sun Life fits best when your goals are long-term, lifetime coverage and legacy or estate planning, not short-term cost minimization

Key benefits of Sun Life whole life insurance

Sun Life whole life insurance comes with a range of long-term benefits designed to provide stability, growth, and protection. It combines guaranteed lifetime coverage with opportunities to build cash value and enhance long-term financial security through these key benefits:

- Lifetime coverage: Your policy remains in force for life

- Fixed level premiums: Premium payments stay the same throughout your chosen premium-pay period

- Tax-advantaged death benefit: Beneficiaries receive the death benefit tax-free

- Cash value accumulation: Your policy builds cash value over time, which you can access through loans or withdrawals

- Dividend potential (for participating plans): Eligible policies may receive annual dividends, which can be used to buy paid-up additions, reduce premiums, withdraw as cash, or earn interest

- Predictable structure options: Non-participating and guaranteed-issue plans offer simpler structures with guaranteed costs and coverage

- Flexible payment terms and optional riders: Choose from life-pay, 10-pay, 20-pay, or 8-pay options (depending on the plan), and enhance coverage with riders such as accidental death, child term, disability waiver, or guaranteed insurability

Types of Sun Life whole life insurance

Sun Life offers five whole life insurance options, including three participating plans, one non-participating plan, and one guaranteed plan. These plans are designed to meet different financial goals and payment preferences.

Participating whole life plans by Sun Life:

- Sun Par Protector II Life Insurance

- Sun Par Accumulator II Life Insurance

- Sun Par Accelerator life insurance

Non-participating whole life insurance by Sun Life:

- SunSpectrum Permanent Life II Insurance

Guaranteed whole life insurance by Sun Life:

- Sun Life Go Guaranteed life insurance

Key features of Sun Life’s participating whole life insurance plans

Sun Life’s participating whole life plans include all the standard benefits of whole life insurance: lifetime coverage, fixed premiums, cash value accumulation, and a guaranteed death benefit. Additionally, they pay annual dividends based on the profits generated by the “par” account, which is funded by participating policy premiums.

Sun Life offers three participating whole life plans:

Sun Par Protector II: Best for long-term estate growth

Sun Par Protector II is ideal for Canadians who want lifetime protection with conservative, reliable cash value growth. It focuses on building guaranteed coverage and steady long-term value.

- Coverage: $50,000 (adults), $25,000 (children) to $15 million

- Cash value: Begins after year 5

- Premium options: Life-pay, 10-pay, or 20-pay

- Dividend options: Paid-up additions, premium reduction, cash payout, or interest-bearing deposit

- Riders available: Accidental death, child term, guaranteed insurability, disability waiver

- Best for: Estate planners or families focused on preserving wealth for future generations while maintaining lifelong coverage

Sun Par Accumulator II: Best for early cash access

Sun Par Accumulator II is designed for those who want to build cash value early and maintain flexibility. It offers faster accumulation and easier access to funds without sacrificing lifetime protection.

- Coverage: $250,000 to $15 million

- Cash value: Begins after year 1

- Premium options: Life-pay, 10-pay, or 20-pay

- Dividend options: Paid-up additions, premium reduction, cash payout, or interest-bearing deposit

- Riders available: Accidental death, child term, guaranteed insurability, disability waiver

- Best for: Professionals and business owners who want access to policy value sooner, or who plan to use the cash value strategically

Sun Par Accelerator: Best for fast equity build-up

Sun Par Accelerator builds equity faster by being fully paid up in just eight years. It’s built for high-income earners who want to grow policy value quickly and enjoy long-term benefits without ongoing payments.

- Coverage: $250,000 to $15 million

- Cash value: Begins after year 1

- Premium options: 8-pay only

- Dividend options: Paid-up additions only

- Riders available: Accidental death, child term, guaranteed insurability, disability waiver

- Best for: Canadians seeking early premium completion and fast-growing equity, ideal for those with higher income and short-term cash flow flexibility

Key differences between Sun Par Protector II, Sun Par Accumulator II, and Sun Par Accelerator

Each of Sun Life’s participating plans serves a distinct goal. Sun Par Protector II focuses on long-term estate growth. Sun Par Accumulator II balances protection and cash value. Sun Par Accelerator builds cash value faster for earlier access.

All three plans offer guaranteed lifetime protection, tax-deferred cash value growth, access to policy loans and living benefits, optional riders like accidental death benefit, child term benefit, and waiver of premium.

However, they differ in how soon cash value grows, how long you pay premiums, and which dividend options are available.

| Category | Sun Par Protector II | Sun Par Accumulator II | Sun Par Accelerator |

| Cash value accumulation | Starts accumulating after 5 years | Start accumulating after 1 year | Start accumulating after 1 year |

| Premium type | Life Pay, 10 Pay, and 20 Pay | Life Pay, 10 Pay, and 20 Pay | 8-pay |

| Coverage amount range |

|

$250,000 to $15,000,000 | $250,000 to $15,000,000 |

| Dividend options |

|

|

Paid-up additions |

| Policy loan availability | 100% of the total cash value minus one year’s interest | 100% of the total cash value minus one year’s interest | 100% of your total cash value minus one year’s interest |

| Tax benefits |

|

|

|

| Payment flexibility | Monthly or annually | Monthly or annually | Monthly or annually |

| Living benefits |

|

|

|

| Death benefit guarantee | Guaranteed for life | Guaranteed for life | Guaranteed for life |

| Additional riders | Accidental death benefit, child term benefit, total disability waiver benefit, guaranteed insurability benefit, business value protection benefit, term insurance benefits, etc. | Accidental death benefit, child term benefit, total disability waiver benefit, guaranteed insurability benefit, business value protection benefit, term insurance benefits, etc. | Accidental death benefit, child term benefit, total disability waiver benefit, guaranteed insurability benefit, business value protection benefit, term insurance benefits, etc.

|

The value of participating plans depends on how Sun Life’s participating account performs over time. This is reflected in its Dividend Scale Interest Rate (DSIR) and overall portfolio performance.

Key features of Sun Life’s non-participating whole life insurance

Sun Life’s non-participating whole life insurance provides guaranteed lifelong protection with predictable costs. Unlike Sun Life’s participating plans, it doesn’t pay annual dividends, instead, it offers guaranteed cash value growth and fixed premiums for complete predictability.

SunSpectrum Permanent Life II Insurance: Best for long-term guaranteed coverage

- SunSpectrum Permanent Life II is ideal for Canadians who prefer predictable costs and steady value accumulation.It offers guaranteed lifelong coverage and stable premiums, without the variability of dividends. It is Sun Life’s non-participating whole life insurance option. This makes it Guaranteed death benefit: Lifetime protection with a guaranteed payout to your beneficiaries

- Fixed premiums: Payments remain constant throughout your chosen payment period

- Cash value accumulation: Cash value grows at a guaranteed rate starting after two years of coverage

- Coverage range: $25,000 to $25,000,000 for individuals up to age 85

- Premium payment options: Life-pay, 20-pay, 15-pay, or 10-pay

- Optional riders: Term riders, accidental death, child term, and waiver of premium for disability

- Best for: Canadians seeking long-term coverage with guaranteed costs and no exposure to dividend fluctuations

For those who need simpler coverage or may not qualify for traditional underwriting, Sun Life also offers a guaranteed issue whole life option with no medical questions.

Key features of Sun Life guaranteed issue whole life insurance

Sun Life Guaranteed Issue Whole Life Insurance provides lifetime protection with guaranteed acceptance and no medical questions. It’s designed for Canadians who want simple, accessible coverage, especially for final expenses or smaller insurance needs.

Sun Life Go Guaranteed Life Insurance: Best for easy, no-medical exam coverage

Sun Life Go Guaranteed Life Insurance provides guaranteed acceptance for Canadians aged 30 to 74, no medical exams or health questions required. It’s designed for those seeking simple, accessible protection, especially for final expenses or smaller coverage needs.

Key features of Sun Life Go Guaranteed Life Insurance

- Guaranteed acceptance: No medical exam or health questionnaire required

- Coverage range: $5,000 to $25,000

- Eligibility: Canadians aged 30 to 74

- Premiums: Fixed for life and guaranteed not to increase

- Payout structure:

- If death occurs within the first two years (non-accidental), Sun Life refunds premiums with interest

- Full coverage applies after two years or for accidental deaths anytime

- Online application: Instant approval available through Sun Life’s digital platform

- Best for: Seniors or individuals with health concerns who need affordable, guaranteed protection for final expenses

| Feature | SunSpectrum Permanent Life II | Go Guaranteed Life Insurance |

| Policy type | Non-participating whole life insurance | Guaranteed whole life insurance |

| Cash value accumulation | Guaranteed cash value accumulation after 2 years | No cash value accumulation |

| Premium type | Fixed premiums with 4 payment options: Life Pay, 20 Pay, 10 Pay, and 15 Pay | Fixed monthly premiums until the age of 95 |

| Coverage amount range |

|

$5,000 to $25,000 (can only be purchased in units of 5,000) |

| Policy loan availability | 100% of the guaranteed cash value minus one year’s interest minus any existing loans | Not applicable |

| Tax benefits | Tax-free death benefit and tax-deferred cash value growth | Tax-free death benefit |

| Payment flexibility | Monthly or annually | Monthly |

| Living benefits |

|

Lump-sum payment equal to 50% of the insurance amount in case of terminal illness |

| Death benefit guarantee | Guaranteed for life | Guaranteed for life |

| Additional riders | Accidental death benefit, child term benefit, total disability waiver benefit, guaranteed insurability benefit, business value protection benefit, term insurance benefits, etc. | Not applicable |

Which limited pay whole life insurance plans are available from Sun Life

Sun Life offers limited pay options across its whole life plans, letting policyholders finish premiums early while keeping lifetime coverage. Sun Par Protector II and Sun Par Accumulator II are available in 10-pay, 20-pay, and pay-to-age-100 options, while Sun Par Accelerator (8‑pay) is fully paid up in eight years. The non-participating SunSpectrum Permanent Life II also offers 10-pay, 20-pay, and pay-to-age-100 options.

Why Sun Life stands out

Sun Life’s whole life insurance lineup is strengthened by the company’s financial profile, product depth, and global business model. Here’s why Sun Life stands out in Canada’s whole life market:

- Strengthens long-term performance through global diversification and multi-market earnings stability

- Supports long-term guarantees with exceptional capital strength and a 154% LICAT ratio

- Offers flexibility through multiple par product designs, including estate, accumulation, and 8-pay options

- Provides scalable planning advantages for affluent and corporate clients seeking tax-efficient wealth transfer and surplus management

How to choose the right Sun Life whole life insurance plan

Choosing the right Sun Life whole life insurance plan depends on your goals, income, and long-term financial priorities. Each plan is built for a specific purpose, from wealth transfer and estate planning to affordable lifetime protection. Understanding what matters most to you helps narrow down the right fit.

Here’s how to match your plan to your needs:

- For wealth transfer or estate planning, choose a participating plan like Sun Par Protector II

- For flexibility and liquidity, choose Sun Par Accumulator II

- For early premium completion and fast cash-value build-up, choose Sun Par Accelerator

- For guaranteed but simpler lifetime coverage, choose the non-participating plan SunSpectrum Permanent Life II

- For health-challenged individuals or smaller coverage needs, choose the guaranteed-issue plan Sun Life Go Guaranteed Life Insurance

How to buy Sun Life whole life insurance with PolicyAdvisor

Ready to explore Sun Life Whole Life insurance? Get a personalized Sun Life whole life illustration and compare it to top Canadian insurers with PolicyAdvisor’s licensed experts.

Get covered in three easy steps:

- Speak with a licensed PolicyAdvisor expert

- Review Sun Par Protector II, Sun Par Accumulator II, and Sun Par Accelerator alongside top competitors

- Receive a personalized illustration and finalize your application online

PolicyAdvisor licensed experts help you compare options and find the perfect plan for your long-term financial goals.

Frequently asked questions

Is Sun Life whole life insurance worth it?

Yes, Sun Life whole life insurance is worth considering, especially if you’re focused on estate planning, lifelong protection, or building tax-deferred cash value. It provides guaranteed lifetime coverage and stable long-term growth. However, whole life insurance costs more than term coverage, so make sure the premiums fit your long-term budget. A licensed advisor can help you compare options and understand trade-offs before you buy.

Can I borrow against my cash value?

Yes, you can borrow against the cash value of your Sun Life whole life insurance policy. Minimum and maximum loan limits vary by plan. Loans accrue interest and reduce your cash value and death benefit. If the loan balance plus interest exceeds your cash value, the policy may lapse and could trigger tax implications, so it’s important to review your statements regularly.

This feature allows policyholders to access funds for short-term needs without surrendering their policy. However, any outstanding balance plus interest will reduce your death benefit if not repaid.

What happens if I stop paying premiums?

If you stop paying premiums, your Sun Life whole life policy won’t immediately lapse. You can choose to activate the Automatic Premium Loan (APL) option, which uses your policy’s cash value to cover missed payments and keep coverage in force. The APL must be elected at issue or added later by request.

If the loan balance ever exceeds the total cash value, your Sun Life whole life insurance policy could lapse. To avoid lapse, you’ll need to repay or resume regular premium payments.

Does Sun Life offer participating policies with dividends?

Yes, Sun Life offers three participating whole life insurance plans such as Sun Par Protector II, Sun Par Accumulator II, and Sun Par Accelerator. These plans may pay annual dividends, depending on the performance of Sun Life’s participating account.

Dividends may include paid-up additions (to increase coverage and cash value), premium reduction, cash withdrawals, or interest on deposit. Dividends are not guaranteed and may change over time, and available options vary by plan, with the Accelerator offering paid-up additions only.

What is Sun Par Protector II Life Insurance?

Sun Par Protector II is a participating whole life plan designed for affordable, long-term protection. It offers lifetime coverage, fixed premiums, and a guaranteed death benefit. The plan’s cash value starts building after five years, and policyholders can choose flexible payment options such as life-pay, 10-pay, or 20-pay. It also offers four dividend options: paid-up additions, cash withdrawal, premium reduction, and interest-bearing dividends on deposit.

What is Sun Par Accumulator II Life Insurance?

Sun Par Accumulator II is a participating whole life insurance plan built for faster cash value access and long-term growth. It offers lifetime coverage with premiums payable through life-pay, 10-pay, or 20-pay structures. Cash value begins accumulating after the first policy year, and policyholders can benefit from annual dividends through options like paid-up additions, premium reduction, cash withdrawal, or interest-bearing dividends on deposit. This makes the Accumulator II ideal for those seeking both protection and early access to policy value.

What is Sun Par Accelerator Life Insurance?

Sun Par Accelerator is a participating whole life insurance plan designed for faster premium completion. It becomes fully paid-up after eight years (8-pay), offering lifetime coverage with no further payments required.

Like other participating plans, it builds cash value starting after the first year and pays dividends as paid-up additions. The shorter payment period makes it suitable for individuals seeking long-term coverage with accelerated ownership.

What is SunSpectrum Permanent Life II Insurance?

SunSpectrum Permanent Life II is a non-participating whole life insurance plan that provides guaranteed lifetime coverage and steady cash value growth. Unlike participating policies, it doesn’t pay annual dividends. Premiums are fixed and can be paid through multiple structures, life-pay, 10-pay, or 20-pay. The plan’s cash value builds gradually over time and can be accessed through withdrawals or policy loans. It’s a good fit for those who want predictable costs and long-term stability without dividend fluctuations.

What is Sun Life Go Guaranteed Life Insurance?

Sun Life Go Guaranteed Life is a guaranteed issue whole life insurance plan designed for those with pre-existing health conditions or difficulty qualifying for traditional coverage. It offers lifetime protection with coverage amounts ranging from $5,000 to $25,000. There are no medical exams or health questions, and approval is automatic for applicants aged 30 to 74. The plan builds a small cash value over time and includes fixed premiums payable up to age 95. A two-year waiting period applies, if the insured passes away during this time (for any reason other than accidental death), the beneficiary receives a refund of premiums paid plus interest. After two years, the full death benefit becomes payable.

Are par account investments affected by market conditions?

Yes, par account investments are affected by market conditions. While Sun Life employs a long-term investment strategy and diversifies across various asset classes to stabilize returns, fluctuations in interest rates and stock prices can still affect the account’s earnings.

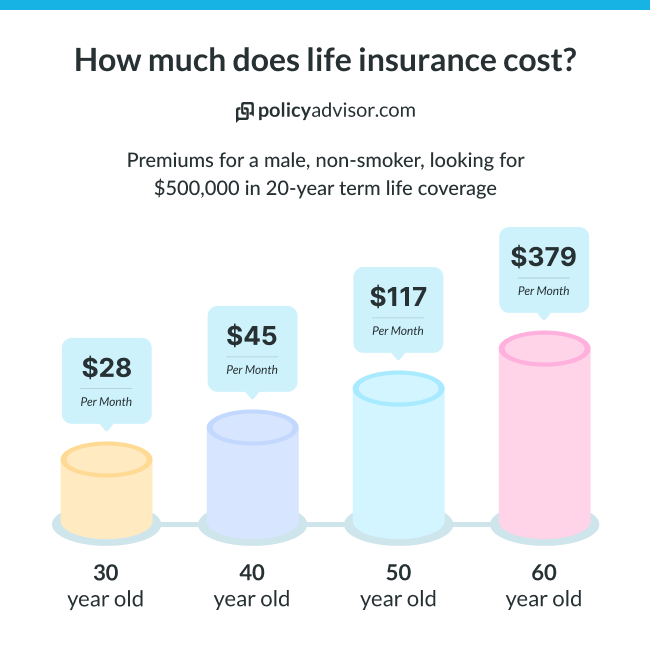

How much does life insurance cost in Canada in 2026?

The cost of life insurance in Canada depends on several factors, including your age, health, lifestyle, and the type of coverage you choose. Typically, life insurance rates range from $30 to $70 per month for $500,000 in coverage for a 30- to 50-year-old individual, though they can be significantly higher for individuals with pre-existing health conditions, high-risk jobs, or lifestyle habits like smoking. In this blog, we break down life insurance rates in Canada in 2026, the key factors that influence premiums, and tips to help you secure the right coverage at the best price.

How much does Life Insurance cost?

Get instant quotes from Canada's top life insurance providers and find the perfect coverage for your family.

Powered by

![]()

Average cost of life insurance in Canada

The cost of life insurance in Canada for a 30-year-old male looking for $100,000 in coverage is around $40 per month for a smoker and $22 per month for a non-smoker. Generally, younger and healthier applicants pay lower premiums, while older individuals or those with pre-existing conditions may face higher costs.

Cost of life insurance by policy type

The cost of your life insurance premiums in Canada can also vary based on the kind of policy that you have purchased. There are a few policy types for you to choose from:

- Term life insurance

- Whole life insurance

- No medical life insurance

- Children’s life insurance

For instance, if you choose term life insurance, the cost of your premiums tends to be lower. Whole life insurance policies typically have a higher premium range, as they ensure coverage for your entire life and provide cash value growth.

Average cost of term life insurance

Term life insurance in Canada offers a budget-friendly way to secure financial protection. For a $500,000 coverage amount, monthly costs can range from $14 to $380, depending on the age of the applicant.

As individuals age or develop health conditions, premiums increase to reflect the higher risk of payout. Since term life insurance provides coverage for a fixed period, such as 10, 20, or 30 years, it is an affordable choice to safeguard a family’s financial future.

Cost of term life insurance for a 10-year period

| Age | Male | Female |

| 20 years | $22/month | $14/month |

| 30 years | $22/month | $15/month |

| 40 years | $27/month | $19/month |

| 50 years | $61/month | $45/month |

| 60 years | $200/month | $145/month |

*Illustrating the cost of term life insurance for a 10-year period for individuals of various age ranges opting for $500,000 in coverage

Average cost of whole life insurance

Whole life insurance, which is a type of permanent insurance, usually costs more because it covers you for your entire life and also has a cash value component attached to it. Typically, for $100,000 in coverage, participating whole life insurance may cost between $54 and $263 per month, whereas a non-participating policy may cost between $47 and $245 per month.

Cost of whole life insurance in Canada

| Age | Participating ($100k coverage) | Non-participating ($100k coverage) |

| 20 years | $52/month | $45/month |

| 30 years | $73/month | $60/month |

| 40 years | $107/month | $85/month |

| 50 years | $163/month | $134/month |

| 60 years | $259/month | $224/month |

*Illustrative costs for a male individual of various age ranges seeking a whole life insurance policy with $100,000 in coverage

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

Cost of no medical life insurance

The cost of life insurance policies that do not require a medical exam, also called no-medical insurance, tends to be higher than comparable fully underwritten coverage; pricing varies by product type and face amount. This type of policy is popular for people who have poor health or who want to get coverage quickly.

Here is an illustration of the cost of a 20-year no medical life insurance policy, with $500,000 in coverage:

Cost of a no medical life insurance policy

| Age | Male | Female |

| 20 years | $76.95/month | $48.15/month |

| 30 years | $80.10/month | $51.30/month |

| 40 years | $89.55/month | $74.70/month |

| 50 years | $233.10/month | $164.70/month |

| 60 years | $634.50/month | $418.50/month |

*Illustrative cost of a 20-year no-medical plan with $500,000 in coverage

Cost of children’s life insurance

It is generally a good decision if parents or grandparents opt to purchase whole life insurance for their grandchildren. The cost of children’s whole life insurance is quite low, and the child can reap the benefits of accumulated cash value throughout their life.

Here’s what a $100/month 20-pay whole life insurance policy for a 5-year-old girl can look like:

Cost of life insurance for children

| Age | Monthly premiums | Accumulated cash value | Death benefit |

| 5 years | $100/month | $0 | $180,000 |

| 20 years | $100/month | $15,000 | $180,000 |

| 35 years | No payment of premiums after the first 20 years | $50,000 | $250,000 |

| 50 years | $120,000 | $400,000 | |

| 70 years | $400,000 | $700,000 |

*Illustrative accumulated cash value and death benefit for a $100/month, 20-pay whole life insurance policy for a 5-year-old girl

What factors impact the cost of life insurance in Canada?

Apart from the type of life insurance that you choose, several other factors, such as age, smoking status, occupation, and more, can impact the cost of your life insurance policy. In the section below, we have elaborated on some of these factors:

- Age: The age of the individual directly affects the life insurance cost. The older the individual, the higher the life insurance premium

- Gender: Typically, men have a shorter life expectancy, so their life insurance premiums are higher. Women pay lower premiums

- Health: An individual’s health also affects premium rates. A healthy individual, compared to someone with a history of medical conditions, will pay a lower premium

- Smoking: Any insurance company in Canada will charge a higher premium if you are a smoker. This is because the health risks associated with smoking are higher than those for a non-smoker

- Lifestyle: If you are involved in high-risk activities as a result of your hobby or occupation, then the insurer views you as higher risk. This increased liability will also result in you paying higher premiums

Cost of life insurance by coverage amount

The cost of life insurance premiums can vary quite significantly based on the chosen coverage amount. Typically, if you are opting for $50,000 in coverage, you have to pay between $10 and $58 per month, depending on your age and gender.

For $500,000 coverage, the cost may go higher, ranging between $22 and $400 per month. For $1 million in coverage, you may have to pay between $35 and $787 per month, with older individuals paying higher premiums.

Cost of life insurance for a 20-year period with varying coverage amounts

| Age | $50,000 coverage | $500,000 coverage | $1M coverage |

| 30 years | $10/month | $29/month | $51/month |

| 40 years | $12/month | $44/month | $82/month |

| 50 years | $23/month | $121/month | $228/month |

| 60 years | $56/month | $399/month | $776/month |

*Illustrative costs for a 20-year term for a male individual of various age ranges, in good health, and maintaining a non-smoking status

Cost of life insurance for seniors

Life insurance premiums are usually expensive for seniors. Typically, the average life insurance rate for seniors in Canada is around $100 per month. Although the cost for term insurance remains the same, term options and durations narrow with age, while small permanent policies are often used for final expense needs.

Depicting the cost of life insurance for seniors

| Age | 10-year term policy | Whole life policy |

| 50 years | $35/month | $111/month |

| 60 years | $55/month | $149/month |

| 70 years | $94/month | $99/month |

| 80 years | $205/month | $131/month |

*Quote for $100,000 in life insurance coverage for a non-smoking female resident of Ontario in good health

Cost of life insurance for smokers

Premiums for smokers can cost almost twice as much as non-smoker rates. This is because smoking can lower your life expectancy.

Cost of life insurance for smokers and non-smokers (male) for varying age groups

| Age | Smoker | Non-smoker |

| 30 years | $42.30 | $22.04 |

| 40 years | $67.95 | $26.99 |

| 50 years | $202.50 | $60.30 |

| 60 years | $556.20 | $198.45 |

*Illustrative costs for a male individual seeking $500,000 in life insurance coverage for a 10-year policy

Cost of life insurance for smokers and non-smokers (female) for varying age groups

| Age | Smoker | Non-smoker |

| 30 years | $25.20 | $15.30 |

| 40 years | $53.10 | $19.35 |

| 50 years | $124.41 | $44.60 |

| 60 years | $325.80 | $144.44 |

*Illustrative costs for a female individual seeking $500,000 in life insurance coverage for a 10-year policy

Cost of life insurance for couples in Canada

The average cost of life insurance for couples is around $30/month if they purchase a joint policy that covers both of them together, and they are both fairly young and healthy. The price does not differ that much from individual term life insurance quotes (except for admin and set-up costs), and it covers both partners at once.

Below are some sample monthly premium costs based on a $500,000 term life insurance policy.

Depicting the cost of life insurance in Canada for smoking and non-smoking couples

| Age group | Monthly premium (Non-smoking couples) | Monthly premium (Smoking couples) |

| 25-35 years | $35 – $60/month | $70 – $110/month |

| 36-45 years | $60 – $90/month | $120 – $170/month |

| 46-55 years | $90 – $140/month | $180 – $250/month |

| 56-65 years | $140 – $220/month | $280 – $400/month |

*Quotes based on $500k in coverage for smoker and non-smoker couples in regular health.

Cost of life insurance for high-risk activities

Engaging in high-risk activities can significantly impact life insurance premiums, as insurers assess these activities as potential threats to longevity. Life insurance for individuals involved in high-risk activities can range from $80 to $350 per month, depending on the activity, coverage amount, and personal risk profile.

Moreover, individuals who participate in hazardous hobbies or professions often pay higher premiums or may be required to obtain specialized coverage. Below are some high-risk activities that can increase life insurance costs:

- Extreme sports: Skydiving, scuba diving, bungee jumping, and rock climbing

- Motorsports: Motorcycle racing, car racing, and dirt biking

- Aviation: Private piloting, flying experimental aircraft, or aerial acrobatics

- Hazardous professions: Construction work, firefighting, offshore oil rig work, and logging

- High-risk travel: Visiting politically unstable regions or countries with high crime rates

Do individuals with pre-existing health issues pay higher life insurance premiums?

Yes, individuals with a history of pre-existing health conditions typically pay higher life insurance premiums. However, insurers assess applicants based on their overall health and medical history to determine the level of risk they pose.

If an individual has pre-existing conditions or a history of serious illnesses, they are considered a higher-risk applicant, leading to increased premium rates. Here are some of the health conditions that may lead to higher premiums:

- Heart disease and hypertension: Individuals with a history of heart attacks, high blood pressure, or other cardiovascular issues

- Diabetes (Type 1 and Type 2): Those with diabetes, especially if poorly managed, are at risk of complications like kidney failure or neuropathy

- Cancer history: A past diagnosis of cancer, even if in remission, can impact premiums

- Obesity: Higher BMI levels, which can lead to various health risks, including diabetes, heart disease, and sleep apnea

- Mental health disorders: Conditions such as severe depression, bipolar disorder, or anxiety, especially if there is a history of hospitalization or medication use

- Respiratory conditions: Chronic illnesses like asthma or COPD (Chronic Obstructive Pulmonary Disease)

How much life insurance do I need to buy?

The right life insurance coverage depends on your financial responsibilities, income, debts, and family’s needs. Here’s how to estimate the amount:

- Income replacement: Aim for 7-10 times your annual income. For instance, if you have an annual salary of $70,000, your life insurance coverage should range between $500,000 and $700,000

- Debt & expenses: The payout should cover the mortgage, loans, funeral costs, and daily living expenses for dependents

- Future needs: Consider childcare, education, and long-term financial security for your family

- DIME formula (Debt, Income, Mortgage, Education): Use the DIME formula and add up these expenses for a tailored estimate

- Affordability: Balance coverage with budget to make sure you purchase a plan that you can afford to pay for

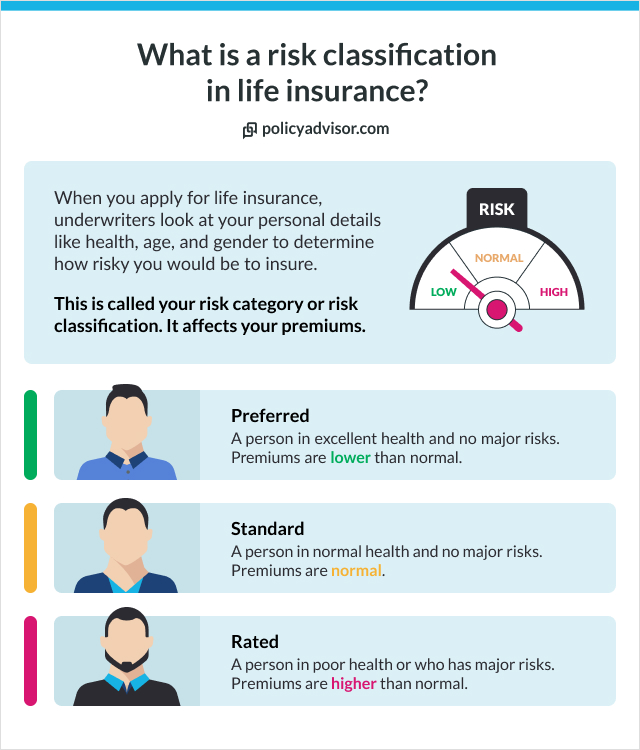

How do insurance companies calculate the cost of your life insurance premiums?

Insurance companies base your premiums on your risk profile — this is their assessment of how risky it would be for them to cover you.

- Insurance companies want to avoid risk as much as possible

- The shorter your life expectancy, the higher the chance that they will have to pay out a lot of money soon — and that’s a risk for them

- Insurers look at personal information about you and your lifestyle to gauge your life expectancy

- They then compare your life expectancy with the amount of coverage you request and use that to decide your cost and whether to cover you at all

What are life insurance premiums?

Life insurance premiums are the payments policyholders make to maintain their coverage. They can be paid monthly, quarterly, or annually, depending on the policy. The cost of your premium will be based on factors like age, health, coverage amount, and policy type.

Is life insurance paid monthly?

Life insurance payments can be made either monthly or annually. Most people choose monthly payments. However, you can get lower prices by switching to a yearly plan. For permanent insurance, you also have the option to condense your payments so you only pay for a certain number of years. This is called a limited-pay plan.

What is the cheapest life insurance?

The cheapest form of coverage is term life insurance. This type of insurance policy provides coverage for a set period of time or term. Term life insurance rates tend to be lower than permanent coverage that lasts your entire life.

Learn more about the cheapest life insurance in Canada.

How can I get preferred rates for life insurance?

Preferred rates are only offered to people who have a low-risk profile. This usually means they:

- Maintain excellent health

- Don’t smoke or have quit smoking

- Don’t participate in risky activities like extreme sports

- Choose the right coverage

Is life insurance worth the cost in Canada?

Yes, life insurance is well worth the cost, especially since premiums are often very affordable.

- Financial security for your family

- Peace of mind in knowing that they’ll be provided for

- Reliable estate planning

- A way to clear outstanding debts

- Future college funding for young children

- A business continuity strategy

- Tax-deferred savings

Does inflation affect the price of life insurance premiums in Canada?

Yes, inflation can affect life insurance rates by:

- Increasing the cost of new premiums

- Making the death benefit have less buying power

- Making your whole life cash value increase

What is the average cost of life insurance in Canada?

The average cost of life insurance in Canada varies based on factors like policy type, age, province, coverage, health status, etc. Any insurance company in Canada takes into account these factors to evaluate the average cost of life insurance in Canada.

Canada Life whole life insurance review (2026)

Canada Life’s participating life insurance policies maintain a dividend scale interest rate of 5.75%, unchanged from the previous two years. Additionally, Canada Life has consistently paid dividends for over 170 years, and its participating account has never missed a distribution year. This is a remarkable record that reflects the insurer’s financial resilience and reliability across economic cycles.

In this review, we explore Canada Life’s whole life insurance offerings, that provide lifelong protection, guaranteed cash value accumulation, and long-term dividend potential.

Wealth Select

My Par Gift

20-pay

pay-to-100

PolicyAdvisor rating

Canada Life whole life insurance earns a 4 out of 5 rating from PolicyAdvisor. It is a leading choice for Canadians who want to use whole life insurance to support charitable giving. Its My Par Gift plan is specifically designed for charitable contributions, with a single premium and cash value starting from year one. It is also known for its long history of dividend payments, a large and financially strong participating account, and disciplined long-term financial management.

Canada Life’s participating plans share in company earnings through annual, non-guaranteed dividends. Dividends depend on participating account investment returns, insurance claims, expenses, taxes, lapses, policyholder behaviour, and surplus management. Each year, Canada Life’s Board of Directors reviews and approves the dividend scale for the following policy year.

Canada Life participating account financials:

- Participating account size: $59.2 billion in total assets

- Policies in force: 1.4 million participating life insurance policies

- Participating account surplus: $3.06 billion

- Dividend history: Dividends paid to participating policyowners since 1848

- Participating account structure: Canada Life operates the largest combined open participating account in Canada

- Dividend drivers: investment experience, mortality experience, expenses, taxes, lapses, withdrawals, and policy terminations

Canada Life’s long dividend history and sizable participating account support stable long-term performance. However, like all insurers, dividends are not guaranteed and can increase or decrease depending on annual experience.

See how much whole life insurance coverage you can get

Get instant quotes from Canada's top life insurance providers and find the perfect coverage for your family.

Powered by

![]()

Canada Life offers two participating whole life options

- Estate Select: A traditional participating whole life policy focused on long-term guarantees and stable estate protection

- Wealth Select: A participating whole life policy designed for higher early cash value growth, long-term accumulation, and estate enhancement potential

Both plans provide lifetime coverage with guaranteed base values and the opportunity to enhance policy value through dividends.

Source: Canada Life Financial Facts 2024

Need insurance answers now?

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

Canada Life whole life insurance costs and value

This example shows the projected premiums, cash value growth, and death benefit for a 30-year-old non-smoker female purchasing $100,000 of Canada Life whole life coverage with life pay and enhanced paid-up additions.

| Policy Year | Age | Annual premium paid | Total premiums paid | Total cash value | Death benefit |

| 0 | 30 | $800.00 | $800.00 | $0 | $100,000.00 |

| 10 | 40 | $800.00 | $8,000.00 | $1,745 | $100,000.00 |

| 20 | 50 | $800.00 | $16,000.00 | $13,419.00 | $100,000.00 |

| 30 | 60 | $800.00 | $24,000.00 | $36,739.00 | $100,000.00 |

| 40 | 70 | $800.00 | $32,000.00 | $68,267.00 | $121,507.00 |

| 50 | 80 | $800.00 | $40,000.00 | $118,346.00 | $164,409.00 |

| 55 | 85 | $800.00 | $44,000.00 | $151,779.00 | $192,112.00 |

| 60 | 90 | $800.00 | $48,000.00 | $190,882.00 | $224,144.00 |

* Values shown are non-guaranteed illustrations based on current assumptions and the insurer’s dividend scale. Actual premiums, cash values, and death benefits may vary. This example is for informational purposes only and does not constitute a policy guarantee.

What are the benefits of Canada Life’s whole life insurance?

Canada Life’s whole life policies provide lifelong coverage while building guaranteed cash value that you can use during your lifetime. They also allow you to pay off your policy quickly (in 10 or 20 years) or spread payments over a longer period of time (until age 100). Key benefits include:

- No maximum coverage: Canada Life’s whole life policies have no set upper limit, meaning you can get as much coverage as you need. However, amounts over $50 million require special underwriting

- Four dividend options: Dividends can be received in the form of cash payments, premium reductions, paid-up additions, and enhanced insurance

- Additional deposit option (ADO): You can increase your policy’s coverage and cash value by making extra payments. However, ADO is subject to MTAR limits, so excess payments may be restricted once the policy is close to the tax-exempt shelf

- Flexibility with premium offset: You can cover some or all of your premium payments using dividends. However, you must bear in mind that premium offset is not guaranteed and depends on investment performance, interest environment, and company experience

- Children’s term life insurance rider: You can include term life insurance on your children with these policies. Future children are added at no additional cost until you turn 55

When it comes to coverage, Canada Life offers several options, including:

- Single life: Covers one person and pays a death benefit upon their passing

- Joint-first-to-die: Covers two people and pays a death benefit when the first insured person dies. The surviving person remains covered for an additional 60 days, during which they can buy a new policy on their life, with no underwriting

- Joint-last-to-die (premiums to first death): Covers two people with premiums payable until the death of the first insured person. Premium payments are higher under this plan

- Joint-last-to-die (premiums to last death): Covers two people with premiums payable until the death of the second insured person. Premium payments are lower under this plan

Types of whole life insurance offered by Canada Life

Canada Life offers two participating whole life policies with lifetime coverage, cash value growth, and annual dividends. Here’s how they differ:

- Estate Select: Provides higher cash value and payout in later years and is ideal for parents looking to secure their children’s future

- Wealth Select: Offers early cash value growth and is ideal for business owners seeking near-term liquidity

| Category | Estate Select | Wealth Select |

| Premium type | Fixed, with flexible payment options (Max 10, Max 20, and Pay to age 100) | Fixed, with flexible payment options (Max 10, Max 20, and Pay to age 100) |

| Coverage amount range | $25,000 to no maximum | $100,000 to no maximum |

| Dividend options |

|

|

| Policy loan availability | Allow loans from cash value. However, ADO premium payments are paused while a loan is active. They resume after full repayment | Allow loans from cash value. However, ADO premium payments are paused while a loan is active. They resume after full repayment |

| Payment flexibility | Monthly or annually | Monthly or annually |

| Living benefits |

|

|

| Additional riders | Accidental death benefit, waiver of premium benefit, guaranteed insurability rider, business growth protection rider (if policy corporately-owned), and child’s term life insurance rider | Accidental death benefit, waiver of premium benefit, guaranteed insurability rider, business growth protection rider, and child’s term life insurance rider |

Source: Canada Life

What are the pros and cons of Canada Life’s whole life insurance?

Canada Life’s whole life policies offer several benefits, from unlimited coverage to multiple payment and dividend options. However, they also have some limitations. Let’s take a closer look at them:

| Pros | Cons |

| Offers unlimited coverage based on your needs (special quote needed for amounts over $50M) | Under the joint-last-to-die (first death) plan, Additional Deposit Option (ADO) payments stop after the first insured person’s death. That means the survivor can no longer enhance their policy using ADO contributions |

| Includes term life insurance rider for children that covers future children at no additional cost (until you turn 55) | Premium offset availability depends on the participating account’s earnings |

| Offers flexibility to increase coverage and cash value through the additional deposit option (ADO) | Canada Life has the lowest dividend rate compared to other insurers |

| Allows you to offset some or all of your premiums using dividends |

Highlights of Canada Life’s whole life insurance policy document

A Canada Life whole life insurance policy document (for Estate Select or Wealth Select) typically includes the following core sections and details:

- Policyholder and insured information: Names, birth dates, and identifying information for the policy owner and the insured person

- Coverage amount: The face amount payable as the death benefit, along with any additional coverage or riders selected.

- Premium schedule: The premium amount, payment frequency (monthly, annual, etc.), and payment duration (10-pay, 20-pay, or to age 100). This section also outlines grace periods and the consequences of missed payments

- Dividend options: The available choices for using annual dividends, such as receiving them in cash, reducing premiums, purchasing paid-up additions, or selecting enhanced coverage

- Guaranteed values: Tables showing the annual buildup of guaranteed cash value and death benefit. Non-guaranteed values based on current dividend scales are also typically included

- Policy loans and withdrawals: Rules for accessing cash value, including loan interest rates and how additional deposits are treated if a policy loan is active

- Riders and optional benefits: Information on add-on features such as children’s term insurance, accidental death benefits, waiver of premium, and guaranteed insurability, along with the conditions for each

- Beneficiary designation: Instructions for naming or changing beneficiaries and an explanation of revocable versus irrevocable beneficiary status

- Plan structures: Details on whether the contract is single life, joint-first-to-die, or joint-last-to-die, and any related privileges such as survivor purchase rights

- Termination and surrender conditions: Requirements and outcomes if the policy is cancelled or surrendered, including any surrender charges and the cash value payable to the owner

- Investment and participating account disclosure: Information on how premiums are invested within the participating account and how dividends are determined for policyholders

- Other legal provisions: Definitions, limitations, exclusions, such as the suicide clause, incontestability rules, reinstatement rights, and instructions on how to submit a claim

These sections are designed to give policyholders clear disclosure of their coverage, obligations, and available options throughout the life of a Canada Life whole life insurance policy.

What are the different limited-pay options offered by Canada Life?

Canada Life offers its participating whole life policies (Estate Select and Wealth Select) with three standard premium payment structures: 10-pay, 20-pay, and pay-to-age-100. The first two are true limited-pay designs, while pay-to-100 is a lifetime premium schedule that is often grouped with them as a third option.

- Max 10 (10-pay): All required premiums are paid over 10 years. After year 10, the base policy is fully paid-up as long as no new riders or additional deposits are added

- Max 20 (20-pay): Premiums are level and payable for 20 years. After year 20, the base policy becomes paid-up for life

- Pay to age 100: Premiums remain level and continue until age 100. This is not a limited-pay option in the strict definition, but it is one of the three standard payment patterns available

Estate Select and Wealth Select can be issued using any of the three premium schedules (Max 10, Max 20, or pay-to-100) for both single-life and joint-life structures. Policyholders can later use features such as premium offset, where dividends cover ongoing premiums, to reduce or eliminate out-of-pocket payments. Contractually, however, the three payment structures listed above are the available choices at issue.

What are the different whole life dividend options that Canada Life offers?

Canada Life offers four dividend options that allow policyholders to customize the performance of their participating whole life insurance to their financial goals.

- Cash payments: Dividends can be received as cash payouts, providing immediate flexibility, though the amount received may be taxable depending on the policy’s adjusted cost basis

- Premium reductions: Dividends can reduce or eventually eliminate out-of-pocket premiums through a premium-offset strategy, depending on long-term dividend performance

- Paid-up additions: Many policyholders reinvest dividends to buy paid-up additional coverage, which increases the death benefit, guaranteed cash value, and future dividend-earning potential, helping the policy compound over time

- Enhanced coverage: This option combines paid-up additions with a term insurance component, offering higher early protection while gradually transitioning to permanent paid-up coverage as the policy matures

How are dividends for Canada Life’s participating policies distributed

Dividends in Canada Life’s participating policies are distributed based on the earnings of the participating (or “par”) account. This account combines premiums from all participating policyholders and invests them in a diverse portfolio of assets.

“Par” account earnings depend on several factors, including investment returns, policy cancellations, insurance claims, and operational costs. When the account outperforms expectations, Canada Life shares the excess earnings with policyholders through dividends.

While dividends are not guaranteed and can vary, Canada Life has a strong track record of maintaining its dividend scale, having paid annual dividends at an interest rate of 5.25% to 5.75% over the past three years.

Dividend Scale - Participating Whole Life Insurance

Compare dividend rates from top Canadian insurers

| 2022 | 2023 | 2024 | 2025 | |

|---|---|---|---|---|

| Equitable | 6.05% | 6.25% | 6.40% | 6.40% |

| Manulife | 6.10% | 6.35% | 6.35% | 6.35% |

| iA Financial Group | 5.75% | 6.00% | 6.25% | 6.35% |

| Desjardins Insurance | 5.75% | 6.20% | 6.30% | 6.30% |

| RBC Insurance | 6.00% | 6.00% | 6.25% | 6.30% |

| Sun Life | 6.00% | 6.00% | 6.25% | 6.25% |

| Empire Life | 6.00% | 6.00% | 6.00% | 6.25% |

| Foresters Financial | 5.50% | 5.50% | 5.50% | 6.25% |

| Co-operators | 5.90% | 5.90% | 6.00% | 6.00% |

| Assumption Life | 5.75% | 5.75% | 5.75% | 5.75% |

| Canada Life | 5.25% | 5.50% | 5.50% | 5.75% |

Powered by

![]()

| Asset class | % of Account | What it means for policyholders |

| Fixed income (Total 60.0%) | Stable returns that support guarantees | |

| Public bonds | 28.3% | Long-term stability and predictable income |

| Private placements | 14.9% | Higher yield with controlled risk |

| Mortgages | 9.8% | Strong cash flow and diversification |

| Cash & equivalents | 7.0% | Liquidity for claims and guarantees |

| Non-fixed income (Total 30.7%) | Helps support future dividend potential | |

| Public equity | 13.7% | Market growth participation |

| Real estate | 12.3% | Inflation hedge and rental income |

| Private equity | 4.7% | Long-term growth with low correlation |

| Other assets | 9.3% | Derivatives and other holdings used for risk management |

Source: Canada Life Combined Open Participating Account – June 30, 2025

Are “par” account investments affected by market conditions?

Yes. While Canada Life employs a long-term investment strategy and “smoothing” mechanism to spread investment gains and losses over several years, changes in interest rates, stock prices, and real estate can still affect the “par” account’s investments.

How can I access my Canada Life whole life cash value?

You can access your policy’s cash value through:

- Cash withdrawals: You can withdraw part or all of your cash value. A full withdrawal will result in your policy’s cancellation

- Policy loans: You can borrow against your cash value. However, you won’t be able to make Additional Deposit Option (ADO) payments while your loan is active

- Collateral loan: You can use your policy as collateral for a loan

- Premium offset: If you have enough cash value, you can use it to pay part or all of your due premiums

What additional benefits or riders does Canada Life offer on their whole life plans?

Canada Life offers several additional benefits or riders on its whole life policies, including:

- Total disability insurance benefit: Covers required premium payments if the insured experiences certain disabilities. To qualify, the insured must be 18 or older when the policy is issued

- Accidental death benefit: Provides a higher payout if death is caused by certain types of accident. This can help beneficiaries manage unexpected payments that may arise due to the covered accident

- Waiver of premium benefit: Covers required premium payments if the insured under this benefit becomes disabled

- Guaranteed insurability rider: Allows you to obtain new permanent policies on the insured person without medical underwriting

- Business growth protection rider: Allows you to purchase additional permanent policies on the insured person over a 10- or 15-year period

- Children’s term life insurance rider: Provides term life insurance coverage for your children, including adopted and stepchildren. Future children are automatically added at no additional cost until you turn 55

How to apply for Canada Life’s whole life insurance with PolicyAdvisor?

You can get a personalized whole life insurance quote for Canada Life through PolicyAdvisor, where you can compare different plans and policies from Canada’s top providers. Schedule a free consultation with our licensed advisors to explore the best options to protect your legacy.

Frequently asked questions

Is Canada Life’s whole life insurance worth it?

If you want lifelong protection with cash value growth that you can access in many ways, a whole life policy could be a smart choice. However, premiums for whole life insurance are generally higher than those for term life and may exceed some budgets.

Does Canada Life offer participating policies with dividends?

Yes. Canada Life offers two participating whole life policy plans, Estate Select and Wealth Select, with flexible payment options.

Do I need medical underwriting for a Canada Life whole life insurance plan?

Yes, Canada Life requires medical underwriting for new whole life insurance policies. However, if you already have whole life insurance, you can enhance your coverage using the Guaranteed Insurability Rider, without any underwriting.

How does the Canada Life participating account work?

Canada Life’s participating account pools premiums from all participating policyholders and invests them in a diversified portfolio of assets. The account’s earnings are influenced by various factors, including investment returns, mortality claims, policy cancellations, and operational expenses. When the account’s earnings exceed expectations, the surplus is distributed among policyholders as dividends.

What is the children’s term life insurance rider?

The children’s term life insurance rider is an optional add-on to Canada Life’s whole life insurance policies. It provides term life coverage for your biological, adopted, and stepchildren. Future children are automatically covered at no additional cost until you turn 55.

What happens if I stop paying my premiums?

If you miss a payment on your Canada Life whole life insurance policy, you have 31 days to make it up. If the premium remains unpaid after this period, Canada Life will automatically take out a policy loan on your behalf, provided your policy has enough cash value. This loan will keep your policy active as long as there’s sufficient cash value to cover future premiums and interest charges.

Manulife whole life insurance review (2026)

Whole life insurance continues to attract Canadians who want lifetime coverage, affordable premiums, and the ability to build long-term cash value. Manulife is one of the most established names in this space and is known for its financial strength and stable participating account performance.

In this review, we’ll help you take a closer look at Manulife’s whole life insurance plans, how they build cash value, the available dividend options, key features, and who can benefit most from this type of coverage.

Manulife Par with Vitality Plus

Performax Gold

20-pay

pay-to-100

PolicyAdvisor rating

Manulife whole life insurance earns a 5 out of 5 rating from PolicyAdvisor for its overall performance, disciplined long-term dividends, and industry-leading financial strength. Manulife operates one of Canada’s largest participating life insurance platforms, supported by a $15.98 billion participating account and more than 307,000 active participating policies.

See how much whole life insurance coverage you can get

Get instant quotes from Canada's top life insurance providers and find the perfect coverage for your family.

Powered by

![]()

Compare dividend rates from top Canadian insurers

| 2022 | 2023 | 2024 | 2025 | |

|---|---|---|---|---|

| Equitable | 6.05% | 6.25% | 6.40% | 6.40% |

| Manulife | 6.10% | 6.35% | 6.35% | 6.35% |

| iA Financial Group | 5.75% | 6.00% | 6.25% | 6.35% |

| Desjardins Insurance | 5.75% | 6.20% | 6.30% | 6.30% |

| RBC Insurance | 6.00% | 6.00% | 6.25% | 6.30% |

| Sun Life | 6.00% | 6.00% | 6.25% | 6.25% |

| Empire Life | 6.00% | 6.00% | 6.00% | 6.25% |

| Foresters Financial | 5.50% | 5.50% | 5.50% | 6.25% |

| Co-operators | 5.90% | 5.90% | 6.00% | 6.00% |

| Assumption Life | 5.75% | 5.75% | 5.75% | 5.75% |

| Canada Life | 5.25% | 5.50% | 5.50% | 5.75% |

Powered by

![]()

Manulife offers two participating whole life options:

- Manulife Par: A traditional participating whole life plan designed for long-term value, disciplined growth, and strong guaranteed features

- Manulife Par with Vitality Plus™: Combines participating whole life coverage with the Vitality rewards program, adding lifestyle-based benefits and engagement incentives

Rating methodology

PolicyAdvisor rates Manulife whole life insurance 5/5 based on six factors: long-term dividend stability, early/long-term cash-value performance, premium flexibility, par fund strength, fees, and riders.

What are the key features of Manulife whole life insurance?

Manulife’s whole life insurance plans start building cash value from the early years of the policy. The maximum issue age for Manulife whole life insurance is 80 years and they offer two dividend options: paid-up insurance and cash.

Insured individuals can avail of policy loans up to 90% of the total cash value. However, non-repayment of these loans can lead to a deterioration in the policy’s overall value. With Manulife whole life insurance, policy holders can get additional riders including child protection, guaranteed insurability, term insurance, and total disability waiver.

| Category | Details |

| Cash value accumulation | Immediate |

| Premium payment frequency | Monthly, annual, and PAC (pre-authorized chequing) |

| Maximum issue age | 18-80 years |

| Coverage amount range | Coverage starts at $100,000 for 10 year, 20 year and pay to age 90 premium durations, and $500,000 for pay to age 100 |

| Coverage options | Single life or joint-last-to-die coverage options |

| Dividend options | Paid-up insurance, cash, and premium reduction |

| Policy loan availability | Yes, up to 90% of the total cash value |

| Additional riders |

|

What are the different Manulife whole life plans I can choose from?

Manulife offers two participating whole life insurance plans, Manulife Par with Vitality Plus™ and Manulife Par. Both policies offer immediate cash value growth and guaranteed access to cash value in the early years. For 10-pay, 20-pay, and pay to age 90 plans, the coverage starts at $100,000. For pay to age 100, the coverage starts at $500,000.

Manulife Par with Vitality Plus™ gives the insured individual access to the maximum-value benefits of Manulife Vitality, the company’s flagship rewards program. Manulife Par with Vitality Plus™ offers only single life coverage while Manulife Par offers single life and joint-last-to-die coverage options.

| Feature | Manulife Par | Manulife Par with Vitality Plus |

| Coverage amount | Starts at $100,000 for 10-year, 20-year, and pay-to-age-90 durations; $500,000 for pay-to-age-100 | Starts at $100,000 for 10-year, 20-year, and pay-to-age-90 durations; $500,000 for pay-to-age-100 |

| Policy fees | No policy fees, but some admin charges may apply | No policy fees, but some admin charges may apply |

| Payment duration options | 10 years, 20 years, to age 90, or to age 100 | 10 years, 20 years, to age 90, or to age 100 |

| Coverage options | Single life or joint last-to-die | Single life only |

| Eligibility for Vitality benefits | Access to Manulife Vitality Go™ benefits at no added cost | Access to maximum-value Manulife Vitality benefits |

| Upgrade option | Upgrade to Manulife Par with Vitality Plus before the 3rd anniversary (no underwriting required) | Not applicable |

| Issue age | 18-80 years | 18-80 years |

| Monthly Vitality® charge | Not applicable | – $15 for pay 10 years

– $10 for pay 20 years – $6 for pay to age 90 – $4 for pay to age 100 |

| Optional add-ons | – Add term life insurance

– Skip payments if disabled (conditions apply) – Guarantee future eligibility for life insurance – Protect children and guarantee their future life insurance coverage |

– Add term life insurance

– Skip payments if disabled (conditions apply) – Guarantee future eligibility for life insurance – Protect children and guarantee their future life insurance coverage |

Source: Manulife.ca

What are the pros and cons of Manulife’s whole life insurance?

Manulife’s participating whole life policies offer a range of benefits such as immediate cash value growth, the option to choose the frequency and duration of premiums, and access to riders. Manulife also offers deposit option payments where the insured individuals can make direct premium payments and increase their protection.

The downside with Manulife’s whole life insurance is that they do not offer non-participating plans and some policy owners may find the dividend and returns structure complex.

| Pros | Cons |

| Immediate cash value growth and guaranteed cash value in the early years | Manulife does not offer non-participating whole life insurance plans |

| Deposit option payments are available where policy owners can make additional premium payments to increase protection | They offer only two dividend options while other insurers typically offer up to four |

| Option to choose the frequency and duration of premium payments | Manulife Par does not offer join-first-to-die coverage |

| Variety of riders offered by Manulife for different life events and needs | |

| Access to Manulife Vitality, a rewards and discounts program |

Highlights of Manulife’s whole life insurance policy document

A Manulife whole life insurance policy document includes the following key elements:

- Policyholder and insured details: Basic information about the policy owner and the insured person, including names and ages

- Coverage amount: The death benefit or face amount, along with the type of coverage (single life or joint-last-to-die)

- Premium schedule: Premium amount, payment frequency, available payment methods, and rules for missed payments

- Payment duration options: Choices such as 10-pay, 20-pay, pay to age 90, or pay to age 100

- Dividend options: How dividends can be used, including paid-up additions or cash, and how earnings are allocated from the participating account

- Guaranteed cash value: Tables showing guaranteed and non-guaranteed cash value growth over time

- Policy loans and withdrawals: Rules for accessing cash value, including loan limits, interest rates, and the impact on policy values

- Riders and optional coverage: Available add-ons such as child coverage, guaranteed insurability, term riders, and waiver of premium

- Beneficiary information: How to name or update beneficiaries and the rules that apply

- Plan structures: Available setups such as single life or joint-last-to-die and how they affect the payout

- Surrender and termination conditions: What occurs if the policy is cancelled or surrendered and the guaranteed values payable

- Investment and par account disclosure: How premiums are invested and how dividends are determined within the participating account

- Legal and general provisions: Definitions, contestability rules, reinstatement options, exclusions, and claim procedures

What are the different limited-pay options offered by Manulife?

Manulife’s whole life insurance (Manulife Par) offers several limited-pay premium structures designed to fully fund the policy within a defined period.

- 10-pay: Premiums are payable for 10 years, after which the policy becomes paid-up for life

- 20-pay: Premiums are payable for 20 years, and the policy is fully paid-up once that period ends

- Pay to Age 90: Level premiums continue until the insured reaches age 90, with lifetime coverage following the final payment

- Pay to Age 100: Level premiums continue until age 100. This option typically includes a higher minimum coverage amount, often $500,000 or more

Policyholders can choose single life or joint last-to-die coverage. These limited-pay structures provide certainty by ensuring premiums end at a fixed point while maintaining lifelong coverage once the payment period is complete.

What is Manulife Vitality?

Manulife Vitality is a wellness-enhanced insurance program that rewards policyholders for maintaining healthy habits. It’s designed to encourage better lifestyle choices and make wellness a part of your insurance experience.

When you’re enrolled, you earn Vitality Points for completing everyday health activities like walking, exercising, getting a flu shot, sleeping well, or meditating. As your points increase, your Vitality Status improves from Bronze to Silver, Gold, and Platinum, unlocking greater rewards and premium savings. These can include discounts on leading brands, fitness devices, and even travel or entertainment perks.

There are two versions of the program: Vitality Go™, which is included at no cost with all eligible plans, and Vitality Plus™, which offers enhanced benefits and exclusive rewards, such as the opportunity to earn a free Apple Watch®, for a small monthly fee. Manulife Vitality is also available with health and dental insurance to help members integrate wellness into both their financial and physical health goals.

What factors affect the performance of Manulife’s participating account?

Factors that influence the performance of Manulife’s participating account are mortality rates, policy cancellations, expenses and taxes, and investment returns. While a participating account is managed to ensure there is always enough money to pay death benefits and cash values, these factors do influence the account’s cash flow and performance.

Let’s understand the factors influencing the participating account:

- Mortality rates: The death benefits of whole life policies are paid from the participating account. Insurers typically plan for the number of death benefits that they may have to pay in a given year. They make this assumption based on Canada’s overall life expectancy. Higher death benefits than expected will deplete the participating account’s funds faster, lower death benefits will have the opposite effect. This is why mortality rates are a crucial factor in determining how a participating account performs fiscally

- Policy cancellations: Based on past consumer behaviour, Manulife makes pricing assumptions of the number of policies that will be cancelled every year. If the cancellation numbers are lower, the participating account may be adversely affected, and vice versa

- Expenses and taxes: Underwriting costs, issuing contracts, making policy changes, and other administrative and operating expenses play a role in the participating policy’s performance. Manulife allocates resources towards these expenses in a manner that is fair and reasonable to the policy holders. If the operating charges are less than the company’s estimates, the participating account’s performance will be positive. If not, the performance may be affected negatively

- Investment returns: The expected returns on an investment play a key role in determining the profitability of a participating account. If the actual returns on an investment exceed Manulife’s pre-determined numbers, it positively affects the participating account. The latter is true if the returns are lower than anticipated

| Factor | Predictability | Stability | Impact on performance |

| Mortality | High | High | Low |

| Cancellations | Medium | Medium | Medium |

| Expenses & Taxes | High | High | Low |

| Investment Returns | Medium | Medium | High |

Need insurance answers now?

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

What dividend options does Manulife offer?

Dividends are a key feature of Manulife’s participating whole life insurance. They represent a share of the company’s financial performance and can enhance your long-term policy value. Manulife offers paid-up insurance, and cash that can be taken out or used for premium reduction. If you choose the paid-up insurance option, your annual dividends are used to automatically buy additional, fully paid-up insurance.

This means that once your dividends have been used to purchase additional coverage, you do not need to make any further premium payments for the paid-up insurance. If you choose the cash option as your dividend strategy, the annual dividends you receive are paid directly to you. In this case, there may be some tax liability.

How are Manulife’s whole life insurance dividends distributed?

Dividends are allocated to Manulife Par policyholders using a dividend scale. A dividend scale is a formula used by all insurance companies to fairly and equitably distribute the dividends among all the policy owners. The dividend scale is not guaranteed and usually increases or decreases based on the participating account’s performance.

| Year | DSIR |

| 2022 | 6.10% |

| 2023 | 6.35% |

| 2024 | 6.35% |

| 2025 | 6.35% |

Source: Manulife Sustainability Report, 2024

How to apply for Manulife whole life insurance with PolicyAdvisor?

To apply for a Manulife whole life insurance plan you would need to choose the plan type (Manulife Par or Manulife Par with Vitality PlusTM), choose your coverage options, fill in an application form, and submit. Your policy may also require medical underwriting based on your plan specifics.

For the best Manulife whole life quotes, speak to our experts at PolicyAdvisor. Our licensed advisors will help choose a plan and coverage options that best suit your needs and budget. We will also support you with the application, making the entire process seamless and easy for you!

Frequently asked questions

Is Manulife whole life insurance worth it?