Deciding to start therapy for mental health can feel like a big step. However, right after that decision, a practical question usually comes to mind: “Will my insurance actually cover this?” With session costs in Canada often running well over $150–$250 per 50–60 min session, it’s worth knowing whether this is included under your plan.

If you’re insured through Sun Life Financial, the good news is that therapy for mental health is included under its health insurance plans.

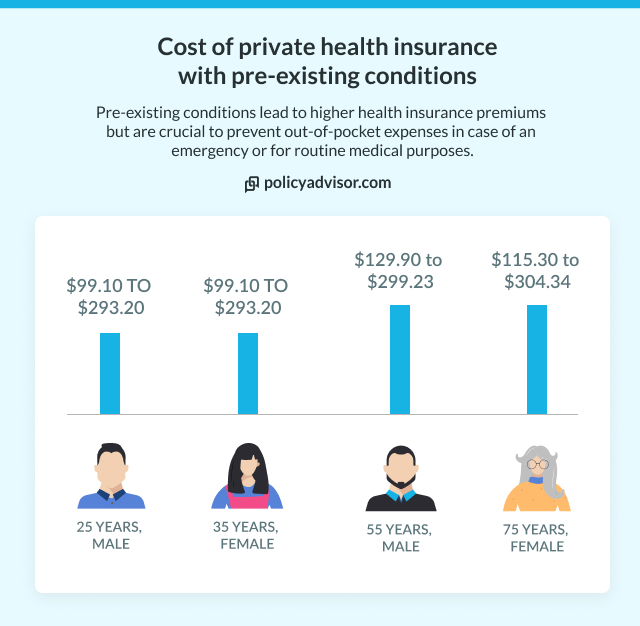

How much does Personal Health Insurance cost?

Get instant quotes from Canada's top health insurance providers and find the perfect coverage for you and your family.

Powered by

![]()

Which Sun Life health insurance plans cover therapy?

Therapy is covered under health insurance benefits within:

- Extended Health Care (EHC) under employer group benefits

- Personal Health Insurance (PHI) for individuals who purchase coverage directly

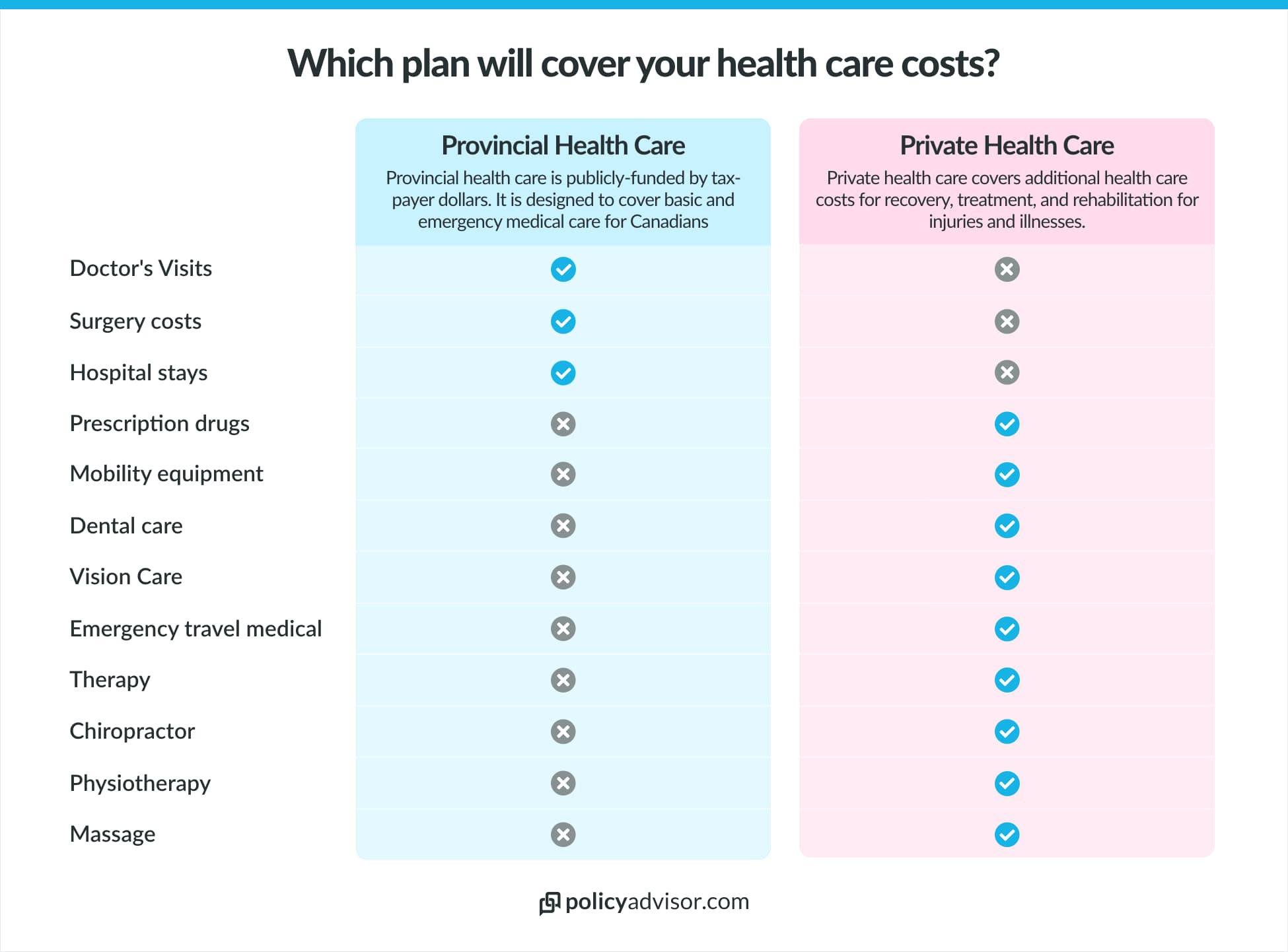

Within these plans, therapy services fall under the category of paramedical services.

Paramedical services refer to care provided by regulated health professionals who are not physicians. This means therapy sessions for mental health support are reimbursed through paramedical benefits and not hospital or medical coverage.

Which therapy providers are covered by Sun Life health insurance in Canada?

Sun Life recognizes specific regulated professionals for therapy under its standard health plans. Eligible practitioner types include:

- Psychologists

- Registered Social Workers

- Registered Psychotherapists

- Registered Clinical Counsellors

Recently, Sun Life expanded its standard Extended Health Care plans to formally include psychotherapists and clinical counsellors, in addition to psychologists and social workers. This expansion has significantly increased access to mental health practitioners.

Eligibility requirements for therapy reimbursement under Sun Life

Even if your plan includes mental health coverage, not every therapy session automatically qualifies for reimbursement. Sun Life Financial sets specific criteria that must be met before a claim is approved. To qualify for reimbursement, the following conditions generally apply:

1. The provider must be regulated and licensed

The therapist must be registered or licensed with a recognized provincial regulatory body in Canada. Coverage applies only to professionals who fall under the eligible practitioner categories outlined in your plan.

2. Services must fall within the provider’s scope of practice

The treatment provided must align with the practitioner’s regulated scope of practice. Services delivered outside their professional designation may not be eligible.

3. The service must be included in your specific plan

Coverage depends on whether your Extended Health Care or Personal Health Insurance plan includes paramedical benefits for mental health practitioners.

4. Annual maximums must not be exceeded

All therapy benefits are subject to annual maximums. Once your plan’s yearly cap is reached, additional sessions within that benefit year will not be reimbursed.

5. Documentation must meet claim requirements

Sun Life may require detailed receipts, the provider’s registration number, clinic address, date and duration, description (e.g., psychotherapy), amount, payment method, and ‘paid in full’ note.

Claims that do not meet documentation standards may be delayed or denied. Keep your provider number visible for faster processing.

Therapy coverage under Sun Life employer group benefits

If you receive Sun Life insurance through your employer, your therapy coverage comes through group benefits. However, employers may customize the plan design, meaning coverage varies by workplace. Your employer may determine:

- The annual maximum for mental health services

- The reimbursement percentage (e.g., 80% or 100%)

- Whether limits are combined across paramedical practitioners

- Whether per-visit caps apply

For example, if your plan covers 80% up to $1,000 per year and your therapist charges $180, you’d pay $36 and Sun Life would reimburse $144, until you reach the $1,000 annual maximum. If your plan has a $20 per‑visit cap, Sun Life would pay the lesser of coinsurance or the per‑visit cap.

Therapy coverage under personal health insurance

If you do not have employer benefits, Sun Life offers personal health insurance (PHI) in Canada. Therapy services are included within coverage categories for psychologists and social workers.

These services are covered as paramedical benefits but with an increased coverage. Sun Life outlines three primary plan tiers with defined annual limits:

1. Basic plan

- General paramedical services: 60% reimbursement, $25 maximum per visit, up to $250 per year, per type of practitioner

Psychology/social workers: Increased coverage to a shared maximum of $500 per year, $35 maximum per visit

2. Standard plan

- General paramedical services: 100% reimbursement, no per-visit maximum, up to $300 per year, per type of practitioner

Psychology/social workers: Increased coverage to a shared maximum of $1,000 per year

3. Enhanced plan

- General paramedical services: 100% reimbursement, no per-visit maximum, up to $400 per year, per type of practitioner

- Psychology/social workers: Increased coverage to a shared maximum of $1500 per year

These maximums apply per benefit year and are subject to plan terms and conditions.

If a provider charges more than the per-visit reimbursement amount (for example, under the Basic plan), the policyholder is responsible for the difference.

Are virtual therapy sessions covered?

Sun Life does not restrict eligible therapy services to in-person appointments. If a session is delivered virtually by a regulated provider who meets plan requirements, it may still qualify under paramedical benefits.

The session may qualify for reimbursement under paramedical benefits if virtual therapy is delivered by:

- A regulated provider

- Practising within their licensed province

- Meeting eligibility criteria under your plan

Additionally, some employer group benefits plans may include:

- Mental health coach

- Virtual care services

- Employee Assistance Programs (EAP)

These services are employer-selected benefits and are not automatically included in every group plan.

How annual maximums work for therapy coverage

All therapy coverage under Sun Life health plans is subject to annual maximums.

An annual maximum sets the total amount reimbursed during a benefit year and resets at the start of each new benefit year. It may apply specifically to mental health practitioners or to all paramedical services combined.

For example, a personal Enhanced plan allows up to $1,500 per year for services provided by psychologists and social workers, so once you reach the annual maximum, additional sessions within that benefit year are not reimbursed.

How to confirm your exact coverage for therapy

To confirm your therapy coverage:

- Log in to your Sun Life account.

- Navigate to Extended Health Care benefits.

- Look for the section “Paramedical Services” or “Mental Health Specialists.”

- Check:

- Annual maximum

- Per-visit reimbursement

- Percentage covered

- Eligible provider types

If clarification is needed, you can contact your human resources (HR) department (for group plans) or Sun Life Customer Care (for personal health insurance).

What is not covered under Sun Life’s therapy benefits

Therapy coverage is limited to regulated practitioners recognized under your plan. Services may not be reimbursed if they are provided by:

- Unlicensed counsellors

- Coaches or wellness consultants

- Providers not registered with a provincial regulatory body

- Services exceeding annual limits

Also the following are typically not covered: missed appointment fees, late cancellation charges, administrative forms/letters, services delivered outside the provider’s scope of practice, and services performed outside Canada or by providers not licensed where you receive care.

How to choose the best Sun Life health plan in Canada

Sun Life offers Basic, Standard, and Enhanced plans, each with different reimbursement levels, annual limits, and coverage for services like prescriptions, dental care, and therapy under paramedical benefits. The right choice depends on how often you expect to use these services and how much coverage you’ll actually need.

If you’re unsure how to compare these options, PolicyAdvisor can help simplify the process and guide you toward a Sun Life plan that balances cost with meaningful coverage.

Frequently asked questions

Does Sun Life cover therapy sessions in Canada?

Yes. Sun Life Financial covers therapy sessions under its Extended Health Care (EHC) employer group benefits and Personal Health Insurance plans. Therapy is reimbursed under paramedical benefits when provided by eligible regulated practitioners and within your plan’s annual maximum limits.

Is therapy automatically covered under all Sun Life plans?

Therapy coverage depends on your specific plan design. Employer-sponsored plans may include mental health benefits, but reimbursement limits, percentage coverage, and whether limits are combined or separate vary by employer contract. Personal Health Insurance plans include defined annual maximums based on plan tier.

Does Sun Life cover online or virtual therapy?

Yes. Virtual therapy may be covered if it is provided by a regulated practitioner who meets your plan’s eligibility requirements. Some employer-sponsored plans may also include additional virtual mental health programs or Employee Assistance Programs (EAP).

What happens if I exceed my annual therapy limit?

Once you reach your plan’s annual maximum for mental health or paramedical services, additional therapy sessions within that benefit year will not be reimbursed. The maximum resets at the start of your next benefit year.

Are all therapists covered under Sun Life?

No. Coverage applies only to regulated professionals recognized under your plan, such as psychologists, registered social workers, registered psychotherapists, and clinical counsellors. Services provided by unlicensed counsellors or non-regulated practitioners are generally not eligible for reimbursement.