An extreme disability benefit rider is a life insurance rider that allows you to access a portion of your death benefit while you are still alive if you become permanently and severely disabled or have a severe loss of independent existence. Upon such an event, the policyholder receives an early payout of the death benefit. This tax-free sum can help cover major medical expenses and provides a temporary safety net for the insured and their loved ones.

While it is not a replacement for disability insurance, it can provide a tax-free lump sum to help cover major expenses and offer a temporary safety net. The Extreme Disability Rider can usually be purchased as an add-on for participating life insurance policies in Canada. However, select insurers like Beneva and Assumption Life provide it as a built-in benefit with select policies.

Need insurance answers now?

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

What is an extreme disability rider?

An extreme disability benefit rider is an optional rider available with some Canadian life insurance policies that allows you to receive a portion of your life insurance death benefit early if you suffer a permanent and severe disability.

Usually, life insurance policies pay the death benefit after you pass away. With an extreme disability benefit rider, you can access part of that payment to cover major medical expenses, adjustment costs, and other immediate financial obligations. Since the early payout is deducted from your death benefit, your beneficiaries will receive less by the amount paid under the rider.

Extreme disability rider in Canada: At a glance

| Feature | Details |

| Purpose / Use case | A rider that allows policy owners to ask for an advanced death benefit when the policyholder has a disease or injury that will cause death within 24 months of diagnosis |

| Benefit type | Tax-free lump-sum payment (subject to policy terms) |

| Typical payout | Usually 25%–50% of the policy’s death benefit, subject to insurer limits |

| Eligibility | Must meet the insurer’s definition of extreme disability or severe loss of independent existence |

| Common qualification | Inability to perform multiple Activities of Daily Living (ADLs) permanently or medical confirmation that the insured has 12 to 24 months or less to live. |

| Does it replace disability insurance? | No. It complements disability insurance but does not replace income protection |

| Available as | Rider to select life insurance policies and free add/benfit with select insurers |

How does an extreme disability rider work?

The Extreme Disability Benefit Rider essentially provides a portion of your death benefit in an accelerated manner. Instead of waiting until your beneficiaries receive your life insurance payout after your death, the rider allows you to receive a portion of that benefit if you are diagnosed with an illness or injury that results in decreased lifespan or an inability to perform Activities of Daily Living (ADLs).

Here is how an Extreme Disability Benefit Rider typically works:

Step 1: Purchase a life insurance policy

You buy a life insurance policy that includes an Extreme Disability Benefit Rider, either automatically or as an optional add-on at an additional cost.

Step 2: Experience a qualifying disability

If you suffer a severe, permanent disability that meets your insurer’s definition of extreme disability during your policy period, you may be eligible to claim benefits under the rider.

Step 3: Submit a claim

Submit the necessary documentation to qualify for the extreme disability benefit rider. The insurer assesses whether your condition satisfies the policy’s eligibility criteria.

Step 4: Receive a lump-sum benefit

Once approved, the insurer pays a lump sum representing a portion of your life insurance coverage in the form of an accelerated death benefit. When you eventually pass away, your beneficiaries receive the remaining death benefit after deducting the amount already paid as part of the rider.

What qualifies as an extreme disability in Canada?

While the definition of extreme disability varies by insurer, it generally refers to a permanent physical or cognitive conditions that leave you unable to live or function independently. You must be completely unable to perform a specific number of activities of daily living (ADLs) without human assistance to qualify for the rider.

Most Canadian insurers require inability to perform at least 4 of the following 6 activities:

- Bathing: Washing your body in a tub or shower

- Dressing: Putting on and taking off necessary clothing

- Toileting: Getting to and from the toilet and maintaining hygiene

- Transferring: Moving into or out of a bed, chair, or wheelchair

- Continence: Controlling your bowel or bladder functions

- Eating: Feeding yourself prepared food

Essentially, a severe loss of independent existence can qualify individuals for the Extreme Disability Benefit Rider. However, it is worth noting that the definition differs between insurers. Consult your advisor to determine what qualifies you for the rider.

Cognitive impairment in extreme disability rider

Apart from ADLs, severe cognitive impairment can also qualify individuals for the extreme disability benefit rider. Situations such as advanced dementia and irreversible organic loss (such as total blindness or the loss of two limbs) can also trigger the rider.

Here are some conditions that may qualify you for an extreme disability benefit rider in Canada:

- Paralysis resulting from a spinal cord injury

- Advanced multiple sclerosis (MS)

- Severe stroke with permanent impairment

- Traumatic brain injury

- Advanced Parkinson’s disease

- Late-stage dementia or Alzheimer’s disease

- Certain progressive neurological disorders

- Permanent loss of mobility requiring full-time assistance

Note that the rider does not pay out based on a medical diagnosis alone. Instead, insurers assess the functional severity and the permanent physical or cognitive impact caused by these conditions.

Is there a waiting period before an extreme disability benefit is paid?

Yes, there is a waiting period before an Extreme Disability Benefit is paid. Before the insurer approves a claim, you must satisfy the rider’s eligibility requirements, provide medical evidence, and remain in a state of continuous extreme disability for a set period specified in your policy. This waiting period varies by insurer and is outlined in the policy contract, typically ranging from 3 to 6 months.

Many Canadian insurers define eligibility based on a permanent and irreversible disability, typically requiring the policyholder to be unable to perform activities of daily living and with no reasonable expectation of recovery. Once it is medically certified and the waiting period is over, the accelerated death benefit is paid out to the insured.

What conditions typically do not qualify for the extreme disability rider in Canada?

The Extreme Disability Benefit Rider in Canada is designed for permanent and severe disabilities, making many conditions unlikely to qualify on their own.

Here are some situations where an individual may not qualify for the rider:

- Temporary disabilities

- Broken bones or fractures expected to heal

- Short-term recovery after surgery

- Mild mobility limitations

- Partial disabilities that do not affect independent living

How much does an extreme disability rider pay in Canada?

The payout of the Extreme Disability Benefit Rider depends on the terms set by your insurer and your policy’s death benefit. Typically, the rider pays a one-time, lump-sum amount, allowing you to cover major disability-related expenses and other living costs.

In many cases, the amount paid by the Extreme Disability Benefit Rider is calculated as a percentage of your life insurance coverage, subject to a maximum limit. Many insurers pay up to 50% of the policy’s death benefit, subject to a maximum dollar limit (typically ranging between $50,000 and $250,000, depending on the insurer and coverage amount).

Here are some illustrative examples of how your Extreme Disability Benefit Rider benefit is calculated:

| Life insurance coverage | Maximum rider benefit* | % of death benefit paid early | Remaining death benefit |

| $250,000 | $100,000 | 40% | $150,000 (60%) |

| $500,000 | $250,000 | 50% | $250,000 (50%) |

*Maximum amount is subject to policy terms and insurer discretion.

Does the extreme disability benefit rider payout reduce your death benefit?

Yes, an Extreme Disability Benefit Rider is considered a form of accelerated death benefit. This essentially means that the money is paid from your existing life insurance coverage and not in addition to it. Once the policyholder passes away, the beneficiaries will receive the remaining amount.

Additionally, the extreme disability rider payout may affect your premiums. Some insurers may adjust premiums to reflect the reduced amount of coverage, while others may continue charging the original premium. If your policy also includes a Waiver of Premium rider, your future premiums may be waived entirely while your coverage remains in force.

Extreme disability rider vs. disability insurance

Although both an Extreme Disability Benefit Rider and disability insurance provide financial support if you are unable to work or live independently, they serve different purposes.

An Extreme Disability Benefit Rider is designed for permanent disabilities that affect your daily living, while disability insurance replaces a portion of your income if an illness or injury prevents you from working. Unlike an extreme disability benefit rider, disability insurance in Canada usually pays a monthly benefit calculated as a percentage of your employment income, rather than your policy amount.

Here’s a quick comparison of Extreme Disability Benefit Rider and Disability Insurance:

| Feature | Extreme Disability Benefit Rider | Disability Insurance |

| Purpose | Provides early access to part of your life insurance death benefit | Replaces a portion of your income if you cannot work |

| Benefit type | One-time lump-sum payment | Monthly income benefit |

| Trigger | Severe permanent disability that meets the policy definition and medically approved reduced lifespan | Inability to work due to illness or injury |

| Benefit amount | Percentage of your life insurance coverage, subject to limits | Percentage of your employment income |

| Payment duration | One-time payment | Monthly until recovery, benefit period ends, or policy expires |

| Affects death benefit? | Yes, reduces the remaining death benefit | Not applicable |

| Available as | Rider on a life insurance policy | Standalone insurance policy |

| Waiting period | Typically 3 to 6 months, or more | Typically 0-14,30, 60, 90, or 180 days |

Extreme disability rider vs. critical illness insurance

Just like disability insurance, many individuals confuse an extreme disability benefit rider with critical illness insurance. Critical illness insurance pays when you are diagnosed with a covered illness, while an Extreme Disability Benefit Rider pays only if you become permanently and severely disabled according to the policy’s definition.

An extreme disability benefit rider pays based on the effect that diseases or impairments have on your ability to function, while critical illness insurance pays based on eligible medical diagnoses.

Here’s a quick comparison of Extreme Disability Benefit Rider and Critical Illness Insurance:

| Feature | Extreme Disability Benefit Rider | Critical Illness Insurance |

| Purpose | Provides early access to part of your life insurance death benefit | Pays you if you are diagnosed with a severe, covered medical condition |

| Trigger | Permanent severe disability or loss of independent existence | Diagnosis of a covered critical illness |

| Common covered events | Inability to perform 4 of 6 Activities of Daily Living (ADL) | Cancer, heart attack, stroke, and other covered conditions |

| Benefit type | Advanced lump-sum payment of a portion of the death benefit | Lump-sum payment |

| Uses existing life insurance? | Yes | Separate insurance policy |

| Reduces life insurance death benefit? | Yes | Not applicable |

| Purpose | Cover disability-related expenses by getting an advance of the death benefit | Help manage the financial impact of a serious illness |

| Can you recover and keep the benefit? | Depends on policy terms | Yes, if the claim is approved |

| Available as | Rider on a life insurance policy | Standalone insurance policy |

Is an extreme disability rider worth it?

If you want comprehensive protection for yourself and your family, you can consider an Extreme Disability Benefit Rider. The benefits essentially allow policyholders to access and request an advanced payout of their death benefit, which can then be used for managing costs and other financial obligations.

Here is an overview of who should consider an extreme disability benefit rider:

| If you | Why an Extreme Disability Benefit Rider can help |

| Own a home | Covers accessibility upgrades like ramps, stair lifts, widened doorways, or bathroom renovations |

| Have a young family | Helps replace lost income and pay for childcare, caregiving, and daily living expenses |

| Are self-employed | Provides financial support if you do not have employer-sponsored disability benefits and helps keep the business running |

| Have major financial obligations | Helps cover mortgage payments, education costs, household bills, and other ongoing expenses |

If you have any surplus budget, you can consider purchasing an Extreme Disability Rider to strengthen your policy and overall coverage.

Can you have an extreme disability rider with Critical Illness or Disability insurance?

Yes, in most cases, you can have an Extreme Disability Benefit Rider alongside a Critical Illness Insurance rider and Disability Insurance rider, when purchased as part of an eligible life insurance policy. Since each covers different situations and serves a different purpose, this combination offers enhanced protection and comprehensive coverage.

While Disability Insurance provides ongoing monthly income and Critical Illness Insurance pays a lump sum after a covered diagnosis, the Extreme Disability Benefit Rider offers an advance of your life insurance death benefit to cover immediate costs and other financial obligations.

However, you cannot purchase the Extreme Disability Rider as an add-on to a standalone Critical Illness Insurance or Disability Insurance policy. It is offered as a built-in or optional feature for participating life insurance policies.

Pros and cons of an Extreme Disability rider

Which Canadian Life Insurance companies offer a built-in extreme disability benefit?

While an Extreme Disability Rider is available as a paid add-on with most major Canadian insurers, some insurers offer it as a built-in benefit on participating policies.

Here’s a list of some of the major Canadian insurers that offer built-in Extreme Disability Benefits in Canada:

- Beneva

- UV Insurance

- Assumption Life

Apart from this, many insurers may offer Extreme Disability benefits as part of a different feature. Consult with your advisor and check if your policy offers these add-ons.

How to purchase an extreme disability rider in Canada?

PolicyAdvisor’s licensed life insurance advisors can help you compare life insurance policies with an extreme disability benefit rider from leading Canadian insurers based on your age, health, coverage needs, and budget.

Whether you are protecting your family or looking for additional financial security, our advisors can help you find the right life insurance policy with the appropriate rider. Our advisors at PolicyAdvisor compare rider availability and benefits across multiple insurers to help you choose the coverage that best fits your needs.

Frequently Asked Questions

Is an extreme disability benefit rider included with every life insurance policy?

Some insurers include it on eligible policies, while others offer it as an optional rider for an additional premium. Availability varies by insurer and policy type.

How much does an extreme disability benefit rider pay?

The payout for an Extreme Disability Benefit Rider depends on your insurer and policy. Many riders provide a percentage of your life insurance coverage, subject to a maximum benefit limit.

Can I add an extreme disability benefit rider after purchasing life insurance?

Some companies allow riders to be added later, while others require you to select them when you first purchase your policy.

Can seniors qualify for this rider?

Yes, but eligibility depends on the insurer’s issue age limits, underwriting rules, and the terms of the rider. Many insurers limit the ages at which you can add the rider to a life insurance policy, and some riders expire at a specified age or stop providing benefits after a certain age.

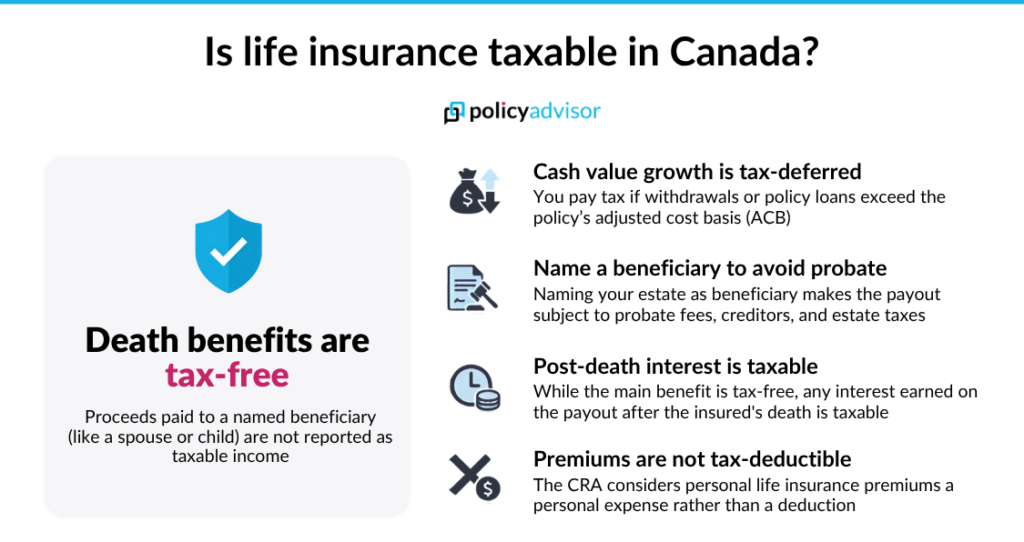

Is extreme disability benefit taxable in Canada?

Extreme disability benefit is typically not taxable in Canada. However, the amounts received by a policyholder while alive can create a taxable policy gain if proceeds exceed the policy’s adjusted cost basis.

Is the extreme disability rider the same as disability insurance?

No, the Extreme Disability Rider is not the same as disability insurance. The rider advances a portion of your life insurance death benefit for a permanent, catastrophic condition, while disability insurance replaces lost income during a temporary or long-term inability to work, usually with a much shorter waiting period.

Is an Extreme Disability Rider the same as a Compassionate Benefit or Compassionate Advance?

No. While both allow you to access part of your life insurance death benefit before you pass away, they are triggered by different circumstances.

An Extreme Disability Benefit Rider pays a lump sum if you become permanently and severely disabled and meet the policy’s definition of extreme disability, whereas a Compassionate Benefit pays a portion of the death benefit if you are diagnosed with a terminal illness. However, both of these benefits are accelerated death benefits, essentially reducing your final payout.