The Immigration, Refugees and Citizenship Canada (IRCC) launched the super visa program in December 2011 to help Canadian families bring their parents and grandparents for extended visits, up to five years at a time. Over the years, the demand for super visa insurance in Canada has continued to rise, and families are actively searching for the cheapest options available to meet visa requirements without overspending.

In this blog, we break down the most affordable Super Visa insurance providers for 2026, explain who they are best suited for, and share smart ways to reduce costs while ensuring your loved ones stay fully protected during their visit.

How much does Visitor Insurance cost?

Get instant quotes from Canada's top travel insurance providers and find the perfect coverage for your trip.

Powered by

![]()

What is super visa insurance in Canada?

Super visa insurance is a mandatory medical insurance policy required for parents and grandparents who want to visit their family in Canada under the super visa program. This insurance protects visitors from high out-of-pocket expenses related to emergency health care during their stay and ensures that they receive necessary medical attention without becoming a financial burden on their Canadian host.

Super visa eligibility

The IRCC enforces strict rules for super visa insurance. To be eligible for a super visa, each applicant must:

- Provide proof of private medical insurance from a Canadian insurance company or a company outside Canada that is approved by IRCC

- Show that the insurance offers a minimum of $100,000 in emergency medical coverage

- Ensure the policy is valid for at least one year from the date of entry

- Be a parent or grandparent of a Canadian citizen or permanent resident of Canada

Need insurance answers now?

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

What are the affordable super visa insurance options in Canada?

Finding the cheapest medical insurance for super visa holders in Canada depends on the visitor’s age, health condition, duration of stay, and budget. In 2026, the most affordable super visa medical insurance providers include Secure Travel, 21st Century, GMS, Destination Canada, TuGo, and Manulife.

- Cheapest for older travellers: Secure Travel

- Cheapest for the lowest base premiums: 21st Century

- Cheapest for low deductibles: GMS

- Cheapest for comprehensive benefits: Destination Canada

- Cheapest for unstable pre-existing conditions: TuGo

- Cheapest for value-added services: Manulife

-

-

1. Cheapest Super Visa insurance for older travellers: Secure Travel

For older travellers, especially those aged 60 and above, Secure Travel stands out as one of the most affordable and straightforward super visa medical insurance options in Canada. With consistently low monthly premiums and a flexible structure, Secure Travel plans are well-suited for seniors aged 60 to 75, even if they have stable pre-existing medical conditions. Applicants can choose to include or exclude coverage for pre-existing conditions, depending on their needs and budget. With the option to pay in monthly instalments, families don’t need to worry about paying the full annual premium upfront.

Why PolicyAdvisor recommends Secure Travel:

- Helps older travellers and their families find the most affordable super visa insurance quickly

- Ideal for seniors with or without stable pre-existing conditions

- Offers flexible plans that cater to a wide range of medical and financial needs

- Easy claims process and responsive customer support

- Simple coverage for low-risk visits

-

-

Monthly cost of Super Visa insurance for Secure Travel

| Age | Monthly premium without pre-existing conditions | Monthly premium with stable pre-existing conditions |

| 55 years | $111.63/month | $131.40/month |

| 60 years | $110.72/month | $135.05/month |

| 65 years | $135.05/month | $170.94/month |

| 70 years | $214.13/month | $281.66/month |

| 75 years | $243.33/month | $333.37/month |

*Depicting the monthly cost of premium for an individual seeking $100k in coverage for Super Visa insurance

2. Cheapest super visa insurance for the lowest base premiums: 21st Century

21st Century offers some of the lowest base premiums in the Super Visa insurance market, especially for healthy parents and grandparents. Their plans provide excellent value for standard $100,000 or $150,000 medical coverage. They have maintained a solid reputation for competitive pricing and streamlined application processes.

Why PolicyAdvisor recommends 21st Century

- The company delivers consistently low premiums without compromising on essential coverage

- Sponsors can reduce costs further by selecting custom deductibles based on their risk tolerance

- The plan is ideal for those under 60 with no major medical conditions

- Offers monthly payment options for budget-friendly options, without compromising on IRCC requirements

Monthly cost of Super Visa insurance for 21st Century

| Age | Monthly premium without pre-existing conditions | Monthly premium with stable pre-existing conditions |

| 55 years | $113.76/month | $191.63/month |

| 60 years | $127.14/month | $228.43/month |

| 65 years | $163.03/month | $271.62/month |

| 70 years | $224.17/month | $390.25/month |

| 75 years | $278.01/month | $485.15/month |

| 80 years | $427.35/month | $651.53/month |

*Depicting the monthly cost of premium for an individual seeking $100k in coverage for Super Visa insurance

3. Cheapest Super Visa insurance for low deductibles: GMS

If you are looking for Super Visa insurance with a low deductible, GMS consistently ranks as one of the most affordable and reliable options in Canada. For families who want to minimize out-of-pocket expenses during a medical emergency, GMS offers exceptional value without compromising on coverage.

Unlike many other insurers that increase premiums significantly for lower deductibles, GMS maintains competitive rates, even at deductibles of $0 or $100. This makes it a smart choice for Super Visa applicants who prefer cost predictability and broader benefits.

Why PolicyAdvisor recommends GMS

- Trusted brand with a strong presence in Canada

- One of the most budget-friendly choices for low-deductible Super Visa insurance

- Reduces financial risk for families by minimizing upfront medical costs

- Ideal for those who want comprehensive coverage without high out-of-pocket payments

- Simple online application and responsive customer service

- Offers coverage for pre-existing conditions that is stable for 180 days

Annual cost of Super Visa insurance for GMS

| Age | Annual premium without pre-existing conditions | Annual premium with stable pre-existing conditions |

| 55 years | $1,602.35/year | $1,602.35/year |

| 60 years | $1,799.45/year | $1,799.45/year |

| 65 years | $2,405.35/year | $2,405.35/year |

| 70 years | $4,296.05/year | $4,296.05/year |

| 75 years | $5,533.40/year | $5,533.40/year |

*Depicting the annual cost of premium for an individual seeking $100k in coverage for Super Visa insurance

4. Cheapest Super Visa insurance for comprehensive benefits: Destination Canada

Destination Canada is often the best value for price in terms of additional perks such as Accidental Death & Dismemberment (AD&D) coverage, and dental plans. They offer notable premium reduction options for those willing to choose a higher deductible, making them one of the most cost-effective options for elderly visitors with or without stable conditions.

Why PolicyAdvisor recommends Destination Canada

- Destination Canada provides age-friendly pricing that many competitors do not match

- Families can take advantage of customizing their coverage and choosing to include or exclude pre-existing conditions

- The insurer is reliable for older applicants, offering clear, transparent policies with minimal exclusions

- Offers monthly payment options to ensure financial flexibility

Monthly cost of Super Visa insurance for Destination Canada

| Age | Monthly premium without pre-existing conditions | Monthly premium with stable pre-existing conditions |

| 55 years | $131.06/month | $146.27/month |

| 60 years | $131.06/month | $146.27/month |

| 65 years | $183.38/month | $228.70/month |

| 70 years | $248.47/month | $358.27/month |

| 75 years | $305.95/month | $441.92/month |

*Depicting the monthly cost of premium for an individual seeking $100k in coverage for Super Visa insurance

5. Cheapest Super Visa insurance for unstable pre-existing conditions: TuGo

TuGo Insurance stands out as one of the most affordable options for Super Visa applicants with controlled pre-existing conditions, such as diabetes, blood pressure, or heart disease. TuGo offers a stability period of 7 days for travellers with a recent medical condition under age 70. They also offer additional riders to make the plan more comprehensive.

Why PolicyAdvisor recommends TuGo

- TuGo is one of the few insurers that includes pre-existing coverage at a reasonable cost

- Their straightforward stability clause removes confusion for families dealing with chronic illnesses/li>

- The company has a reliable claims track record, especially important when medical history is involved

- The coverage option will extend beyond the basic emergency medical care

Annual cost of Super Visa insurance for TuGo

| Age | Annual premium without pre-existing conditions | Annual premium with stable pre-existing conditions |

| 55 years | $1,704.55/year | $1,993.99/year |

| 60 years | $1,810.40/year | $2,398.05/year |

| 65 years | $2,149.85/year | $2,844.81/year |

| 70 years | $3,011.25/year | $3,984.70/year |

| 75 years | $3,810.60/year | $5,042.47/year |

*Depicting the annual cost of premium for an individual seeking $100k in coverage for Super Visa insurance

6. Cheapest super visa insurance for value-added services: Manulife

Manulife may not have the lowest base premium, but their plans are packed with value-added services, making them the most affordable for those seeking comprehensive protection. The brand’s global footprint and responsive emergency assistance make it a reliable choice for families who want to ensure coverage quality without compromise.

Why PolicyAdvisor recommends Manulife

- Manulife’s brand reputation and service quality instill trust among applicants

- The company supports digital claims and renewals, making it easy to manage from overseas

- Offers global 24/7 emergency support with multilingual services

- Provides flexible plan options for those with and without pre-existing medical conditions

- Includes companion benefits, prescription drug coverage, and accidental death

Annual cost of Super Visa insurance for Manulife

| Age | Annual premium without pre-existing conditions | Annual premium with stable pre-existing conditions |

| 55 years | $1,969.91/year | $2,165.36/year |

| 60 years | $2,299.50/year | $2,529.45/year |

| 65 years | $2,613.77/year | $2,874.38/year |

| 70 years | $3,801.84/year | $4,181.26/year |

| 75 years | $4,932.43/year | $5,426.82/year |

*Depicting the annual cost of premium for an individual seeking $100k in coverage for Super Visa insurance

What factors can impact the cost of your Super Visa insurance in Canada?

Several key factors affect how super visa insurance costs in Canada. While all plans must meet IRCC’s minimum coverage of $100,000 for one year, your parents’ age, health, and coverage options can significantly change the premium. Here are the main factors that influence its costs:

- Applicant’s age: Insurance companies charge higher premiums as the applicant gets older, with sharp increases after age 60 or 70

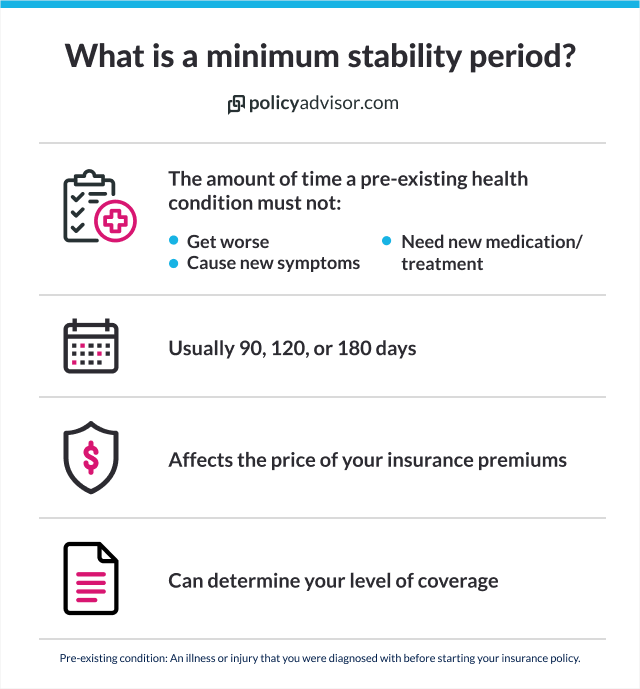

- Pre-existing medical conditions: If you include coverage for stable conditions like diabetes or hypertension, insurers will raise the cost of the plan

- Stability period: Plans that accept shorter stability periods typically come with higher premiums due to greater risk

- Coverage amount: Choosing higher coverage amounts, such as $200,000 or $300,000, increases your premium compared to the $100,000 minimum

- Deductible chosen: Selecting a higher deductible lowers your premium, while opting for a $0 deductible raises it

- Payment method: Paying monthly may help with cash flow, but it ends up costing more than paying the full amount upfront

-

Does a higher deductible lower the cost of super visa insurance in Canada?

Yes, choosing a higher deductible can significantly lower the cost of super visa insurance in Canada. A deductible is the amount the insured person agrees to pay out of pocket before the insurance coverage begins. When applicants select a higher deductible, such as $1,000, $2,500, or even $5,000, insurance companies reduce the overall premium because the financial risk to the insurer decreases.

This option works well for healthy parents or grandparents who are unlikely to make a claim or who want to save on upfront insurance costs. However, applicants must weigh the savings against their ability to afford the deductible in case of a medical emergency. Always read the policy carefully to understand how the deductible applies in real-life situations.

How can I lower the cost of my Super Visa insurance?

Lowering the cost of your super visa insurance in Canada is possible with a few smart strategies. Since premiums vary based on age, health, and coverage choices, selecting the right plan can make a big difference without sacrificing essential protection.

- Choose a higher deductible: Opting for a $1,000, $2,500, or even $5,000 deductible can significantly reduce your monthly or annual premium

- Stick to the basic $100,000 coverage: Higher coverage amounts like $200,000 or $300,000 offer more protection but also raise your costs

- Pay the annual premium upfront: Paying in full typically works out cheaper than choosing monthly instalments, which often include extra fees

- Compare quotes from multiple insurers: Always request quotes from at least 3–4 providers to find the most competitive option for your situation

-

How to get the best Super Visa insurance quotes in Canada?

To get the best super visa insurance quotes in Canada, use a trusted online broker like PolicyAdvisor, which works with 30+ top Canadian insurance companies. Our licensed advisors compare multiple plans based on your age, health status, travel duration, and budget to recommend the most suitable and affordable option that meets IRCC’s Super Visa requirements.

You can view side-by-side quotes, customize coverage, and choose from flexible payment options. Beyond the purchase, PolicyAdvisor also offers dedicated after-sales support. We assist with policy changes, cancellations, refunds for visa denials, and claims guidance. Schedule a call to ensure a smooth and worry-free Super Visa insurance purchase for your parents or grandparents.

Frequently asked questions

Do super visa insurance premiums increase every year?

Yes, super visa insurance premiums typically increase with each passing age, especially for seniors. Insurers adjust rates based on age brackets, health risk data, and inflation in medical costs. If your parents or grandparents are reapplying or renewing their visit after a year, expect higher quotes even if nothing else changes.

Can I switch my Super Visa insurance provider after arrival in Canada?

Yes, you can switch Super Visa insurance providers after arriving in Canada, but only if your current policy is cancelled and refunded properly. Some insurers allow partial refunds for unused days if you haven’t made any claims.

Before switching, make sure the new plan meets IRCC’s requirements, especially the minimum one-year coverage. Contact both providers in advance to avoid any lapse in coverage, which could affect your Super Visa status or re-entry into Canada.

Can I pause or suspend Super Visa insurance if my parents leave Canada early?

No, most Super Visa insurance plans cannot be paused, but you can request a partial refund if your parents leave Canada before the policy’s end date. Refund eligibility usually depends on no claims being filed and your parents providing proof of departure, such as flight tickets or exit stamps. You must submit a cancellation request before the coverage ends.

Can I get a refund if my Super Visa application is denied after purchasing insurance?

Yes, most Canadian Super Visa insurance providers offer a full refund if your visa application gets denied, as long as you provide proof of refusal (such as an IRCC rejection letter). You must also cancel the policy before the start date. Refund policies vary slightly between insurers, so it’s crucial to review the cancellation terms before buying.

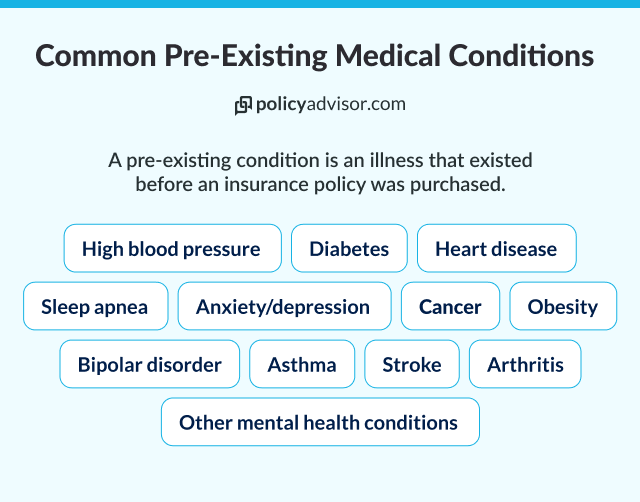

Does the affordable super visa insurance cover pre-existing medical conditions?

The cheapest Super Visa insurance plans usually offer basic emergency medical coverage and often exclude pre-existing conditions to keep premiums low. However, some affordable policies do cover pre-existing medical conditions, but only if the condition is stable for a certain period (typically 90, 180, or 365 days before the policy start date).

If your parent or grandparent has conditions like diabetes, hypertension, or heart disease, and those conditions are stable, insurers like TuGo, Manulife, and Destination Canada offer relatively low-cost options that include this coverage.

Can I pay monthly for super visa insurance in Canada?

Yes, you can pay monthly for Super Visa insurance in Canada, but only a few providers offer this option. This is especially useful for families sponsoring parents or grandparents on a tight budget. However, monthly payment plans often come with slightly higher total costs due to administrative fees. Always review the full terms before choosing the monthly payment option for your super visa insurance.