Employee benefits are no longer just an added perk in Canada; they are a key part of financial satisfaction in the workplace. According to employee benefits statistics published in January 2026, 89% of employees in Canada say benefit plans are important for their financial health and security.

For small businesses, offering competitive benefits can help attract and retain talent, but finding the right insurance company may not be easy. This guide highlights the best employee benefits providers for small businesses in Canada to help employers stay competitive and support their workforce.

How much does Group Insurance cost?

Get instant quotes from Canada's top group insurance providers and find the perfect coverage for your business.

Powered by

![]()

Quick verdict

If you are looking for reliable group benefits providers for a small business, several insurers in Canada stand out for their flexibility and overall value. Some focus on affordability and plan customization, while others are known for strong customer service.

Below are some of the best small business employee benefits companies in Canada:

- Manulife

- Equitable Life

- Sun Life

- Empire Life

- Canada Life

- Desjardins

- GreenShield

- Blue Cross

Refer to the table below to see the strengths of employee benefits providers in Canada and our ratings.

| Company name | Best for | PolicyAdvisor rating |

| Manulife | Flexible & customizable coverage | 5/5 |

| Equitable Life | Standardized & pooled plans | 5/5 |

| Sun Life | High dental and vision coverage | 5/5 |

| Empire Life | Mental health & virtual care support | 4.5/5 |

| Canada Life | Extensive nationwide coverage | 4.5/5 |

| Desjardins | High paramedical coverage options | 4/5 |

| GreenShield | Integrated digital care & claims process | 4/5 |

| Blue Cross | Higher travel coverage | 3.5/5 |

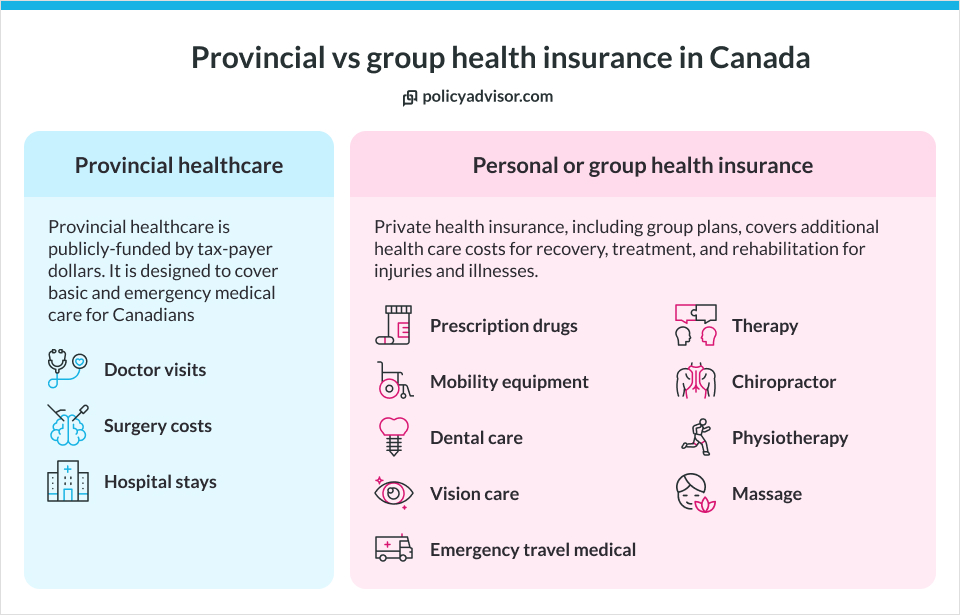

What are employee benefits for small businesses?

Employee benefits are employer-sponsored insurance and wellness programs offered to employees as part of their overall compensation package. For small businesses in Canada, group benefits serve as effective plans that help employees manage health care costs, access preventive care, and maintain financial stability during illness or disability.

Some employers may provide Employee Assistance Programs (EAPs), Health Spending Accounts (HSAs), and various wellness benefits. Together, these benefits help small businesses support employee well-being in the best way possible.

What are some common employee benefits offered by small businesses in Canada?

Common employee benefits offered by small businesses in Canada include:

- Health and dental insurance: Covers medical expenses such as prescription drugs, doctor visits, dental treatments, and preventive care that may not be fully covered by provincial health plans

- Life insurance: Provides a tax-free lump-sum payment to an employee’s beneficiaries if the employee passes away while covered under the plan

- Disability benefits: Replaces a portion of an employee’s income if they are unable to work due to illness or injury

- Critical illness insurance: Pays a lump-sum benefit if an employee is diagnosed with a covered serious condition such as cancer, heart attack, or stroke

- Travel insurance (emergency medical): Covers emergency medical expenses if an employee becomes ill or injured while travelling outside their home province or outside Canada

- Paramedical services: Includes coverage for practitioners like physiotherapists, chiropractors, psychologists, and massage therapists

- Registered retirement savings plans (RRSPs): Allow employees to save for retirement through payroll deductions

Some businesses also offer wellness programs, mental health support, and flexible work arrangements as part of their benefits packages.

Which are the best small business employee benefits companies in Canada?

Manulife, Equitable Life, Sun Life, Empire Life, Canada Life, Desjardins, Green Shield, and Blue Cross are some of the best companies offering employee benefits in Canada. Refer to our review below to see the strengths of each company and our ratings.

1. Manulife

Manulife mobile app on the go for access

Health Service Navigator for employees

Manulife provides group benefits tailored for Canadian small businesses with 2 to 50 employees. It is a great option for businesses looking to offer flexible and customized benefits to their employees.

Manulife’s group benefit plans provide coverage for extended health care, dental care, and short- and long-term disability. Critical illness insurance and accidental death and dismemberment coverage are available as optional benefits. With many flexible options available, Manulife makes it easy to customize a benefits package that fits your team’s needs perfectly.

Unique selling point (USP): Stands out for its flexible and customizable group benefits plans tailored to diverse workforce needs

- Option to customize the plan with critical illness insurance at no additional cost

- Provides centralized and easy access to all of Manulife’s pharmacy-related resources and programs, including industry-leading drug lookup tools

- Allows employees to use web-enabled devices to easily submit claims and review recent claims/claim details

- Specialty Drug Care Program that manages specialty drugs to save costs and improve health outcomes

- DrugWatch is a rigorous oversight program designed to ensure plan sponsors get value for the dollars they spend as drug costs increase

- Prescription drugs

- Vision

- Dental

- Health care spending account

- Employee and family assistance program

- Paramedical practitioners

2. Equitable Life

Virtual medical care through Dialogue

Homewood Health EFAP

Equitable offers group benefits specifically designed for businesses with 2–25 employees, with a strong focus on standardized, pooled plans to ensure stable pricing and coverage. It provides a range of plan options, including Bronze, Silver, Gold, and Platinum.

Their plans can cover everything from dental and vision care to life insurance and even mental health support. Their health coverage includes prescription drugs and paramedical services like physiotherapy, chiropractic, and massage therapy. Employees also get access to dental coverage along with mental health support.

Unique selling point (USP): Pooled group plans for 2-25 lives that offer stable benefits and small renewal hikes

- Competitive pre-packaged plan design options to fit every need and budget

- 24/7 access to medical professionals via Virtual Healthcare (Dialogue)

- Counselling services through phone, web, or in-person via the Employee and Family Assistance Program (Homewood Health)

- Online wellness resources for health and financial challenges (Homeweb)

- DrugAssistTM program to help you get coverage for high-cost drugs

- Self-guided mental health support using Cognitive Behavioural Therapy

- Vision

- Hospital accommodation

- Paramedical practitioners

- Health care spending account

- Life, accident, and critical illness insurance

- Dental care

- Taxable Spending Account (TSA)

3. Sun Life

Teladoc Medical Experts® Services

Flexible benefits

Sun Life’s group plan provides the best health coverage through personalized health services and comprehensive health solutions (Lumino Health Virtual Care). To be eligible, the plan requires the business to be in force for at least 3 months and a minimum 75% employee participation rate.

Sun Life’s SunAdvantage plan, designed for businesses with 3 to 49 employees, offers strong dental coverage with up to $2,500 for basic/preventive care, $3,000 for major services, and up to $3,500 lifetime for orthodontics. Vision care is also included as an option, with coverage ranging from $75 to $500, supporting routine eye care and eyewear needs.

Beyond this, employers can customize plans with options like short- and long-term disability, extended health care, health spending accounts, and employee assistance programs.

Unique selling point (USP): Offers high coverage for dental and vision, backed by a digital health ecosystem, ensuring both high-value benefits and seamless care access

- Flexible benefit plans tailored to meet employee needs while staying within budget

- Digital experience through the my Sun Life mobile app

- A comprehensive range of insurance products designed to help small businesses achieve long-term financial and health security

- Lumino Health Virtual Care EAP connects employees to health and well-being resources

- User-friendly administrative tools like sponsor kits, a dedicated website, and toll-free access to a personalized customer service administrator

- Bright Promise service guarantees to meet your service needs and provide compensation if it remains unfulfilled

Standard coverage

- Life insurance

- Dependent life insurance

- Accidental death and dismemberment (AD&D) insurance

- Short-term disability

Additional options

- Extended health care

- Dental care

- Health spending account

- Employee assistance program

- Stress management and well-being

- Critical illness insurance

4. Empire Life

Mental Health Navigator for mental well-being

AssistNow Employee Assistance Program

Empire Life offers flexible group benefits designed to support employees’ well-being, with a strong emphasis on mental health and virtual care through integrated services such as Teladoc Medical Experts and Mental Health Navigator. Through Teladoc, employees can get the convenience of finding a doctor, expert medical opinion, personal health navigator, and medical records eSummary.

With a strong focus on affordability and ease of administration, Empire Life provides valuable tools like online benefits management, helping employers streamline processes. Employees can also enjoy reliable access to health services, making it a comprehensive solution for businesses looking to prioritize employee care.

Unique selling point (USP): Built-in mental health navigation and virtual care access, ensuring employees get the right support quickly

- Continually evolving with digital connectivity and innovation

- Mental Health Navigator to offer personalized services related to mental well-being

- Known for their flexibility in adjusting the cost and coverage as per needs

- Teladoc Medical Experts to offer virtual medical services

- Known for their personal touch and commitment to customer service

Core benefits:

- Accidental death and dismemberment coverage (AD&D)

- Life insurance

Optional benefits:

- Weekly indemnity

- Critical illness

- Long-term disability

- Healthcare Spending Account

- Extended health benefit

- AssistNow Employee Assistance Program

5. Canada Life

360 Total Care to manage illness

Digital admin tools for online enrollment

Canada Life’s group benefits plan for small businesses, known as Freedom at Work, offers tailored benefits and savings packages for businesses with up to 75 employees. The plan is backed by extensive nationwide coverage and global medical assistance support.

Through the 24/7 worldwide emergency medical assistance, employees get access to a global network that helps locate care, coordinate services, and secure approvals during medical emergencies while travelling for vacation, business, or education. This group benefit plan is affordable and helps businesses attract and retain top talent while supporting employees’ health and financial well-being.

Unique selling point (USP): Combines extensive nationwide coverage with 24/7 global medical assistance, ensuring employees have seamless access to care wherever they are

- Provides 24/7 global emergency medical assistance for travelling employees

- A dedicated service team with in-depth knowledge of your specific benefits plan

- Comprehensive digital experience for submitting and tracking claims, along with personalized notifications about your benefits

- Access digital tools for health information, participate in individual wellness challenges, and connect with a virtual health coach through Consult+ Virtual Health Care

- DrugSolutions to manage the plan’s drug costs

- Life and accident insurance

- Critical illness

- Disability management program

- Prescription drugs

- Dental care

- Health care spending accounts

6. Desjardins

Gender affirmation coverage

Health is Cool 360° platform for health management resources

Desjardins’ customizable solution, PerformPlus, is designed for companies with 3 to 49 employees, providing options such as life, disability, extended healthcare, and dental care insurance. The plan stands out for its wide-ranging paramedical benefits, covering services from physiotherapists, psychologists, chiropractors, massage therapists, kinesiologists, speech therapists, and more.

The plan is available for small businesses employing permanent staff working at least 10 hours per week, as well as eligible temporary employees. With Desjardins group benefits, employers also get access to the Omni app, which offers seamless digital tools like online claims, a drug card, a drug cost simulator, and a pharmacy value finder, ensuring both flexibility and convenience.

Unique selling point (USP): Delivers extensive paramedical coverage with flexible reimbursement across a wide network of health professionals

- The Health PACT grants employees access to licensed healthcare professionals for early chronic illness intervention

- Their Assistance Programs provide professional support for employees and managers during difficult times

- They have tools to control drug costs, including a cost simulator

- Gender affirmation coverage includes surgeries and treatments not covered by public health insurance, plus a workplace support kit

- Life insurance

- Accidental death and dismemberment insurance

- Critical illness insurance

- Health insurance

- Health Spending Account and wellness account

- Gender affirmation surgery and procedures

- Dental care

- Travel insurance and trip cancellation insurance

- Short and long-term disability insurance

- Vision care options

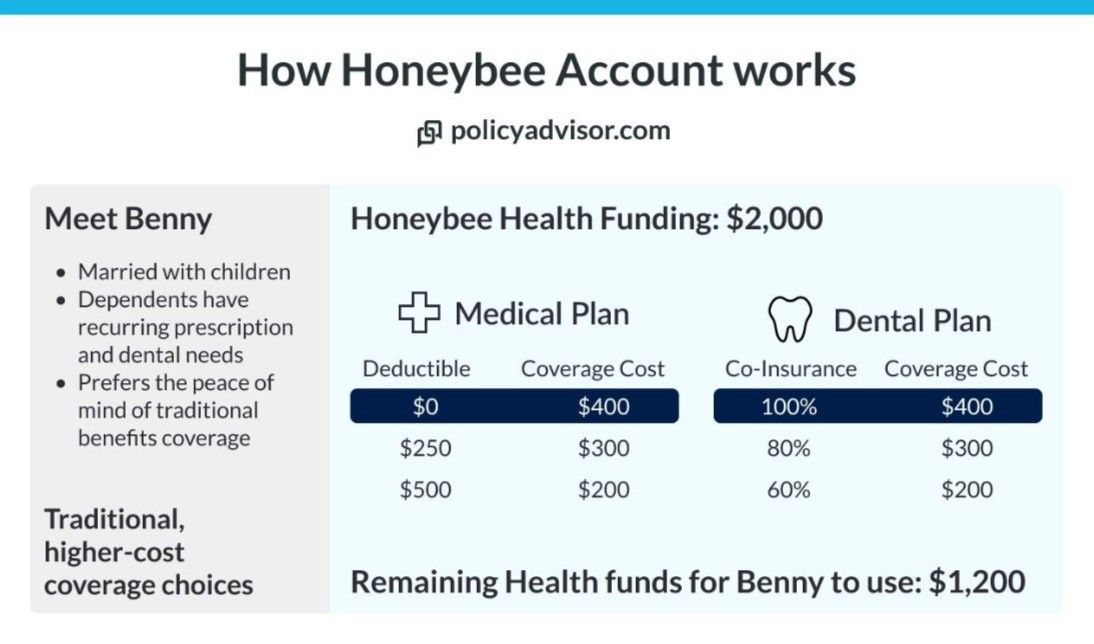

7. GreenShield

Administration Services Only feature

Integrated digital administration platform

GreenShield offers the Honeybee Select group benefits plan for small businesses with fewer than 25 employees. Honeybee Select groups receive full access to Honeybee’s digital benefits platform with a streamlined user experience.

This digital solution provides essential coverage options, including health, dental, and travel insurance, along with mental health support from Inkblot Therapy. The plan also includes add-on allowance accounts for customizable coverage options, making it an innovative solution for small businesses new to employee benefits.

Unique selling point (USP): Integrated digital administration platform that provides a complete view of employee benefits on one platform

- Customizable plans that align with your company’s needs, with scalable pricing to grow with your organization

- Honeybee Allowance Account allows for employee-directed spending without premiums

- Lifestyle benefits for modern workplaces, like fitness and wellness programs

- Transparent “pay for what you use” model through their Administration Services Only (ASO) feature

- Health and dental insurance

- Vacations, volunteer work, adventure & sports activities

- Fitness, sports & equipment benefits

- Travel insurance

- Claims management assistance

8. Blue Cross

Easy claim submission through the Medavie app

Virtual medical care and Employee Assistance Program

Blue Cross offers three plans: Entry, Essential, and Enhanced, which are designed for businesses with at least two employees and have been operational for a minimum of six months. Eligible individuals include Canadian residents under 75 with full-time employees working at least 20 hours per week.

While Blue Cross offers life insurance, accidental death and dismemberment coverage, and extended health benefits, its standout feature is its comprehensive emergency medical travel coverage for up to $5M. They also have additional benefits like health spending accounts, personal spending accounts and long-term disability.

Unique selling point (USP): Offers high coverage for emergency travel coverage, offering up to $5M protection for employees on the go

- Their travel insurance coverage provides 100% reimbursement under all three plan types: Entry, Enhanced, and Essential

- With Blue Advantage, members can save up to 20% on medical, health, and wellness expenses

- Their 360° Total Care program offers Health Coaching and Chronic Disease Management for conditions like asthma, diabetes, hypertension, obesity, and more

- The super-fast online enrolment process takes only a few minutes and can be signed electronically

- Comprehensive coverage for cognitive behavioural therapy, along with live, online, and text-based counselling

Core benefits:

- Basic and dependent life insurance coverage

- Accidental death and dismemberment

- Extended health care

- Prescription drugs

- Dental care

- Worldwide travel insurance

Additional benefits:

- Critical illness

- Long-term disability

- Health spending account

- Personal wellness account

Methodology for reviewing the best small business group benefits companies in Canada

To determine the best small business employee benefits in Canada, our experts assessed companies based on the following criteria:

- Coverage: Scope of health, dental, vision, paramedical, prescription drugs, life insurance, disability, and critical illness options available

- Affordability: Average premium required to pay for the total number of employees

- Flexibility and customization: Modular plans, health spending accounts, coinsurance choices, guaranteed acceptance limits, and scalability for growing teams from 2-50 employees

- Customer experience: Digital tools for claims, mobile apps, dedicated advisors, EAP/wellness programs, and 24/7 support accessibility

Group health benefits cost comparison

| Category | Blue Cross | Desjardins | Equitable | Empire Life | Green Shield | Sun Life | Manulife | Canada Life |

| Health | ||||||||

| Drug maximum | – Entry: $3,000

-Essential: $5,000 -Enhanced: $20,000 |

An amount of your choice between $2,000 and $15,000 per insured per year, in increments of $1,000 | -Bronze: $5,000/year

-Silver- $25,000/year. -Gold: $100,000/year -Platinum: $100,000/year |

Varied by plans | -$3,000/person

-$10,000/person |

Vary depending on the drug

formulary selected |

$2,000 per year – the maximum you pay annually. Coverage then increases to 100% | Varies |

| Drug coinsurance | 80% | 80% | 80% | 80% | 80% | 50% to 100% | 100% | 100% |

| Paramedical services | Varies | Varies | -Bronze: No coverage.

-Silver: $300/practitioner/year -Gold: $500/practitioner/year -Platinum: $500/practitioner/year |

$500 | -$300/practitioner -$500/practitioner | $100 to $1,000, or $1,250 combined | $350 maximum per calendar year for each practitioner | Varies |

| Vision care (frame lenses and eye exams) | – Entry: No coverage

– Essential: $200 per 24 months for frames and lenses -Enhanced: $300 per 24 months |

Maximum: $100 to $500 in increments of $25, in any 12-month period | No coverage in bronze and Silver.

-Gold: $200/year -Platinum: $250/year |

$200 every 24 months | – $150/24 months/person

– $250/24 months/person |

$75 to $500 | $200 per 24 months | -$200 every 24 months -$250 every 24 months |

| Vision coinsurance | 80% | Varies | 100% | 80% | 80-100% | 100% | 70-100% | |

| Dental | ||||||||

| Basic dental maximum | – Entry: $1,000

-Essential: $1,500 -Enhanced:$1,500 |

From $500-

$4,000, or unlimited |

No coverage in bronze

-Silver: $1,500/year -Gold: $2,000/year -Platinum: $2,500/year |

$1500 | -$750/person – $15,00/person | $2,500 | $3,000 per person, per calendar year | Varies based on the province of your residence |

| Basic dental coinsurance | 80% | Varies | 70-90% | 80% | 80% | 50% to 80% | 80% | 80% |

| Recall exam | Three choices: Every 6, 9 or 12 months | Varies | Varies | 1 every 6 months | Varies | Varies | Yes | |

| Pooled benefits (as requested) | ||||||||

| Life insurance | Entry: $25,000

– Essential and enhanced: $50,000 |

–Minimum $10,000

–Maximum $1,000,000 (in combination with plan member’s optional life insurance) |

-Bronze and silver: $25,000

– Gold: $50,000 – Platinum: $75,000 |

$30,000 | Yes | -$20,000 to $750,000 | Up to $1,000,000 | 100% of annual salary to a maximum of $1,250,000 |

| Accidental death and dismemberment (AD&D) | – Entry: $25,000

– Essential and Enhanced: $50,000 |

Maximum $1,000,000 | Same as life insurance | $30,000 | Up to $10,000 for repatriation and rehabilitation | Up to $50,000 | Same as life insurance | |

| Short-term disability benefits | Varies | Up to $2,000 (without evidence of insurability) | Varies | Varies | Up to $1750 per week (20+ lives) | Depends on the plan | 100% of your weekly salary for the first week; 75% for the next 15 weeks | |

| Long-term disability benefits | – Entry: No coverage

-Essential and Enhanced- $4,000 |

Depending on group size, up to $14,000 (with evidence of insurability) | Varies | Varies | Up to $12,000 per month | $12,000 | $25,000 | |

| Added benefits | ||||||||

| Hospitalization | – Essential: No coverage.

– Essential and enhanced: $200 per day for semi-private and private rooms |

Semi-private | 100% coverage for semi-private accommodation | Semi-private or private | 100% coverage for semi-private or private room | Semi-private room | ||

| Health Spending Account (HSA) | Yearly allocation choices of $200, $500 or $700 | $250 per plan member | Plan sponsor choice | Varies based on admin fees | As requested | Same number of credits for all employees | -Full-time employees: $100/year

-Part-time employees: $50/year |

Varies based on admin fees |

| Travel Insurance | -$5,000,000 per person, per incident in all 3 plans. | – Medical emergency expenses: 100% up to a lifetime maximum of $5 million | Varies based on the travel benefits | Not specified; varies by plan | Yes | Varies | Varies | Varies |

How much does a small business employee benefits package cost in Canada?

Employee benefits packages for small businesses typically cost between $150 and $275 per employee per month.

Average monthly cost per employee for a small business group health plan

| Plan Type | Average cost of coverage per employee per month |

| Basic | $150/month |

| Standard | $205/month |

| Enhanced | $275/month |

*Please note, these are average costs for one employee per month, pricing may vary based on factors like company demographics, employee’s age, etc.

Factors affecting the price of small business employee benefits

Group benefits pricing for small businesses in Canada is determined by several factors that help insurers estimate the overall risk and expected claims within a group. Here is a list of these factors:

- Number of employees in the group: The larger the group size, the lower the cost for employers because the risk is spread across more employees

- Nature of business: Businesses that have risks associated with them, such as construction or manufacturing, may end up paying higher premiums

- Employee profile: The age, gender, and family status of employees can significantly affect premiums. Older employees or groups with more dependents generally result in higher premiums

- Coverage: The level of coverage opted for directly affects the premium. For instance, plans that include higher reimbursement levels for, say, prescription drugs, dental care, paramedical services, or vision care typically cost more than the others

- Additional benefits: Optional features such as Health Spending Accounts (HSAs), Employee Assistance Programs (EAPs), critical illness coverage, and others can increase the overall cost of the group benefits plan

Who pays for group health benefits in small businesses?

In small businesses, group health benefits are typically shared between the employer and employees (based on the employer’s discretion). Many companies require employers to pay 50% of premiums, although this varies by insurer. Employees contribute the remainder through payroll deductions.

The employer’s contribution is often designed to make the benefits affordable and competitive. The exact cost-sharing arrangement can vary depending on the business’s budget and the specific health insurance plan.

In some cases, employers may choose to cover the full premium as an added benefit to attract and retain employees. The contribution structure and coverage options are customizable based on the business’s needs.

Tax advantages of group benefits in Canada

Offering group benefits can provide important tax advantages for both employers and employees in Canada. Here are some of the key tax advantages of group benefits for small businesses in Canada:

- Premiums paid by the employer toward a group benefits plan are generally treated as a business expense and can be deducted when calculating the company’s taxable income

- Employer-paid health and dental coverage is generally not considered a taxable benefit for employees, meaning they do not pay income tax on these benefits

- Many group benefits plans also include a Health Spending Account (HSA). Employer contributions to an HSA are generally tax-deductible for the business, while reimbursements for eligible medical expenses are typically tax-free for employees

How to choose the best employee benefits plan for small businesses in Canada?

In general, choosing the best group benefits packages in Canada involves several critical steps. Listed below are a few of them:

- Understand employee needs: You need to start by assessing employee requirements through surveys to understand what they value most in a benefits package. Once you have this information, set a budget that reflects what your organization can afford while ensuring financial stability

- Look for flexible options: Consider offering flexible benefits plans, which allow employees to select the benefits that resonate with them, fostering satisfaction and retention. Also, prioritize core benefits like health insurance and retirement plans, as these are often essential to employees

- Explore cost-sharing options: Decide how premiums will be split between the employer and employees

- Wellness and mental health coverage: Look for plans that include wellness programs, counselling, therapy, and Employee Assistance Programs (EAPs) to support both physical and mental well-being

- Analyze claim risks: Consider how claims may impact future premiums, especially in small groups where high usage can lead to noticeable renewal increases

- Consult licensed advisors: At PolicyAdvisor, our insurance experts are here to help you find the best employee benefits plans. They will guide you through coverage options, premiums, and additional benefits you can offer your employees. Trust us to find the best fit for your business! Schedule a call with our team today!

Frequently asked questions

How can small businesses provide employee benefits while managing costs?

Small businesses can manage employee benefits costs by choosing cost-effective health plans, offering a mix of fully insured and self-funded options, and sharing premium costs with employees.

They can also explore wellness programs, which can help reduce long-term health care expenses, and look for group benefit plans that provide comprehensive coverage at competitive rates.

Why should small businesses offer benefits if they only have a few employees?

Even with a small team, offering benefits helps them attract and retain talent, stay competitive, and improve employee satisfaction. Group benefits show employees that you value their well-being, which can boost morale, productivity, and loyalty.

Who is eligible for employee benefits in Canada?

Eligibility for employee benefits typically requires employees to be Canadian residents or temporarily working abroad, provided their Government Pension Plan and Health Insurance remain active. Employers may also set specific criteria, such as length of service or job classification, to determine benefit eligibility within their organizations.

What benefits do employees value most in Canada?

In Canada, employees highly value health and dental coverage, retirement plans, and work-life balance. Additionally, paid time off for new parents is a significant benefit. These offerings enhance overall job satisfaction and contribute to a positive workplace culture, making them essential for attracting and retaining talent.

What are the mandatory benefits for employees in Canada?

In Canada, mandatory benefits for employees include the Canadian Pension Plan (CPP), Employment Insurance (EI), and workers’ compensation. These benefits ensure financial security for workers during retirement, provide support during periods of unemployment, and offer protection in case of workplace injuries, forming a critical safety net for all employees.

Can an employer force you to take benefits in Canada?

In Canada, employers cannot compel employees to accept benefits. However, they can require certain benefits as part of the employment package, particularly if outlined in the employment contract or collective agreements. This ensures clarity and consistency in the benefits offered while allowing employees to make informed choices.