Getting life insurance with a criminal record in Canada can be challenging, but it is not impossible. Many insurers assess your criminal record when determining eligibility, premium rates, and coverage limits. While certain offences may impact your ability to secure a policy, options still exist.

In this article, we’ll help you understand how life insurance providers evaluate criminal records, which insurers may be more flexible, and what steps you can take to improve your chances of getting coverage.

Need insurance answers now?

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

Is it possible to get life insurance with a criminal record?

Yes, having a criminal record does not automatically disqualify you from getting life insurance in Canada. However, insurers assess your application based on the specifics of your record, such as the type of offence, when it occurred, and whether you have demonstrated rehabilitation.

Each insurance provider has different rules for applicants with a criminal history. While some may offer coverage at higher premiums, others may deny applications outright. Those considered high-risk may need specialized policies, such as simplified issue or guaranteed issue life insurance.

However, it is crucial to be honest in your application. If you fail to disclose a criminal record, it can result in claim denial or policy cancellation later. Most insurers conduct background checks, so any discrepancies can lead to severe consequences.

What do insurers typically ask on a life insurance application?

Life insurance companies gather details about your family’s health history, your health history, and your lifestyle when applying for a life insurance policy.

Your family’s health history

- Any hereditary conditions such as heart disease, diabetes, or cancer

- History of premature death due to illness

Your health history

- Current medications (names and dosages)

- Diagnosed medical conditions (physical and mental)

- Past surgeries or major medical procedures (last 10 years)

- Your doctor’s name and contact information

- Weight history (fluctuations, major weight gain/loss)

Your lifestyle

- Travel history in the past two years and upcoming plans

- Driving record (reckless driving, license suspension, DUIs)

- Smoking, alcohol, and drug use history

- Criminal record or pending charges

- High-risk hobbies (skydiving, scuba diving, mountain climbing, racing, etc.)

- Aviation history (flying as a pilot or student pilot)

Some insurers will ask specifically about past convictions, including how long ago you were found guilty and whether you’re still on parole.

Sample question from an application:

“In the last 10 years, have you been charged with, convicted of, or pleaded guilty to any criminal offence or financial services regulatory offence (including securities regulators), or are any criminal charges pending?”

If you answer yes, follow-up questions may include:

- Nature of the offence

- Date charged (month and year)

- Details of the sentence (fine, probation, imprisonment, etc.)

- Date of sentence (month and year)

How long do insurance companies consider criminal records?

The time insurers look back at your criminal record depends on the company. Some only ask about offences within the past 12 months, while others may review records going back 5, 10, or even a lifetime.

Many insurance providers that PolicyAdvisor works with will still consider your application if you have a criminal record. Still, approval depends on the severity of the offence and how much time has passed. Just because an insurer asks about your record doesn’t mean they’ll automatically deny you.

Here’s a breakdown of how far back each insurance company looks when assessing traditional life insurance applications.

This list is based on general application questions and does not mean that these insurance companies will accept your application if you were convicted before the period they asked about. Any mention of a criminal record at any time may mean the insurance company will ask for a criminal record check.

What kind of life insurance can you get with a criminal record?

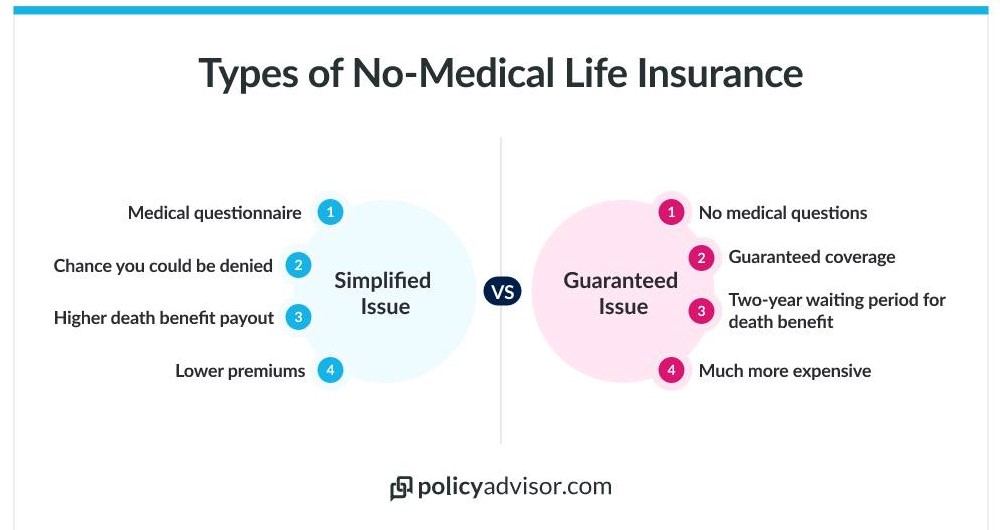

If you have a criminal record, insurers may classify you as a high-risk applicant, making it harder to qualify for traditional life insurance. However, you still have options like simplified issue life insurance and guaranteed issue life insurance.

Depending on your record and the insurer’s criteria, you may be eligible for the following types of coverage:

- Traditional life insurance – Some insurers may approve you for standard term or permanent life insurance, especially if your offence was minor or occurred long ago

- Simplified issue life insurance – No medical exam is required, but you must answer some health and lifestyle questions. This option is more accessible to high-risk applicants

- Guaranteed issue life insurance – No medical exams or health questions. Approval is almost guaranteed, but coverage limits are lower, and premiums are higher

Simplified issue life insurance

Simplified issue life insurance has a faster and easier application process than traditional life insurance. It typically requires no medical exam and asks fewer questions, making it more accessible to high-risk applicants.

However, some insurers still inquire about criminal records, though they may focus on convictions from further in the past compared to traditional policies. Approval depends on factors like the severity of the charge and the time since conviction.

Since insurers take on more risk by reducing their screening process, premiums are higher than traditional policies. If you have a criminal conviction, here are your best simplified issue life insurance options:

| Company | Application question |

| iA Financial (Deferred) | Within the last 1 year, have you been found guilty of a criminal offence (including DUI) or are awaiting trial? |

| UV Financial (Simplified) | Have you been convicted of or charged with a criminal offence (including impaired driving) in the last three years? |

| Humania (No-Medical) | In the last 5 years, were you incarcerated for more than 48 hours? |

| CPP Insurance (Simplified) | Within the last 10 years, have you been convicted, incarcerated, on probation or parole, or awaiting sentencing for a criminal offence? Within the last 2 years, have you been charged with DUI or impaired driving? |

Guaranteed issue life insurance

Guaranteed issue life insurance is a “no questions asked” policy for those who can’t qualify for traditional or simplified coverage. There are no medical exams and only basic eligibility questions, such as age and residency status.

Some insurers, like CPP, still ask about recent convictions, but if your offence happened long ago, it won’t affect approval. This is the easiest option if you have a criminal record, but premiums are higher due to the lack of underwriting.

| Company | Application question |

| CPP (Guaranteed) | Within the last 5 years, have you been convicted, incarcerated, on probation or parole, or awaiting sentencing for a criminal offence? Within the last 2 years, have you been charged with DUI or impaired driving? |

| Edge Benefits | Questions vary based on your record |

Can you get life insurance if you’re in jail?

Getting life insurance while in jail is extremely difficult and, in most cases, not possible. Most insurers automatically decline incarcerated applicants, awaiting trial, or on probation. Even after you are released, many companies require at least one year to pass before considering your application and approval is not guaranteed.

If you attempt to apply from jail, you must:

- Prove financial stability to pay for coverage

- Demonstrate stable health through medical records

- Provide a full history of drug/alcohol use and other personal details

Even with these documents, traditional life insurance is unlikely to be an option. If you’re incarcerated, your best chance at coverage will be after release, once you’ve met an insurer’s waiting period requirements.

Can you get life insurance if you’re on probation?

Yes, it’s possible to get life insurance while on probation. However, your application’s approval depends on the length, type, and severity of your probation, and your insurer’s risk assessment.

- Length of your probation – Longer probation periods may raise red flags for insurers

- Type and severity of the crime – Felony convictions make approval much harder than misdemeanours

- Insurer’s risk assessment – Some companies may approve coverage but with higher premiums or shorter policy terms due to the added risk

In some cases, insurers may also require a third-party guarantor, such as an employer, to vouch for your good behaviour during probation.

What to do if my life insurance application is rejected?

If your life insurance application has been rejected due to a criminal record, you can still consider other options such as a simplified or guaranteed issue policy, or schedule a call with an experienced advisor to help find an insurer.

- Apply for simplified issue or guaranteed issue life insurance – These policies are designed for individuals who have difficulty obtaining traditional coverage

- Speak with an insurance advisor – Our advisors have access to 30+ Canadian insurers and may be able to help find a provider willing to offer coverage based on individual circumstances

Does life insurance cover criminal death?

If you die while committing a crime, your beneficiary may not receive the payout. Other common exclusions include death due to reckless endangerment, such as racing a car, or pre-existing medical conditions that weren’t disclosed on the application.

Will my criminal record affect the cost of my life insurance?

Yes, having a criminal record will usually affect your life insurance rates. The cost of life insurance will fluctuate based on your health and lifestyle. With traditional life insurance, the company may put a rating, meaning a scaled price increase, depending on how long ago your charge was and the severity of it.

If you’re denied traditional life insurance, you can apply for simplified or guaranteed issue life insurance, but the base costs of these policies are higher than traditional ones.

How to apply for life insurance if you’ve had a criminal conviction?

If you have a criminal conviction, the best approach is to speak with a licensed life insurance expert at PolicyAdvisor. Our team can review your history without judgment and help find the best possible coverage for you and your family.

Everyone deserves financial protection for their loved ones, and we’re here to make that happen—no matter your past. Schedule a call today to explore your options.

Frequently Asked Questions

Can you get life insurance if your charges were dropped?

Yes, if your charges were dropped, you should be able to get life insurance. However, insurers may still ask for details about the charge and the circumstances. The key factor is whether you were convicted—if not, you typically don’t need to declare it on your application.

Do vehicle-related convictions affect life insurance?

Yes, life insurance applications ask about all convictions, including those related to vehicles. If you have DUIs or other serious driving offences, insurers may request a motor vehicle report to assess your risk. This report includes traffic violations (like running a stop sign) and non-moving violations (like seat belt tickets). A history of frequent violations, especially combined with a criminal record, can label you as high risk, which may lead to higher premiums or denial.

Can you lie about your criminal record on a life insurance application?

No, and we strongly advise against it. If an insurer discovers undisclosed convictions, they can deny your application or refuse to pay the death benefit to your family. Most policies also have a two-year contestability period, meaning insurers can review and void coverage if they find false information. After paying premiums, the last thing you want is for your family to receive nothing because of a misrepresentation.